There is a growing danger that network neutrality supporters are going too far in creating analogies to the "treat all apps equally" position.

For starters, the analogy is being applied on a broader basis in ways that probably are not helpful. Network neutrality, over time, as swept up so many concepts that it is in danger of becoming "anti-consumer" in its application, the opposite of what its supporters intended.

For example, the extension of the concept to sponsored apps, where mobile consumers in many developing nations get access to social media apps such as Facebook, without having to buy a data plan, now is cited as a violation of network neutrality. If so, some of us would say, go ahead and violate at will, because people like and benefit from the practice.

Likewise, there now is an argument, advanced in support of net neutrality concepts, that sees danger in managment of the flow of electricity under conditions of high load. That also is a potential overstep.

Electrical utilities already know what they must do when demand exceeds supply. They cut off access to some, as required, to preserve the integrity of the grid as a whole. That is called a brownout, a planned and rolling disruption of power supply under extreme conditions, to preserve the functioining of the electrical grid as a whole.

The point is that denying all access, not just to some apps, sometimes is a step a utility supplier must take, under extreme load. Telcos have done the same. When voice circuits became overloaded because of holiday calling, for example, users were denied admission to the network and got a message instructing them that "all circuits are busy now, please try your call later."

Networks have to be managed under conditions of high load. There is an intellectual trap network neutrality supporters are in danger of falling into, namely overplaying the analogy in too many settings, to the point where the value of the original premise is damaged.

Yes, sometimes the flow of electrons to your house could be throttled or blocked, for entirely understandable reasons. Sometimes that is done with your permission, as when you allow temporary shutdown of your air conditioning, in the summer, to help your energy supplier manage load.

Either way, network managment is valuable and necessary. Allowing the whole network to go down isn't so smart. That's one value of smart grids.

Blocking or throttling sometimes might be necessary, under conditions of high load. That is different from blocking specific competitive and lawful apps. That is an antitrust issue, though.

Monday, August 4, 2014

Overstetched Analogies Now Threaten Net Neutrality Arguments

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, August 3, 2014

Zero Rating: Does Consumer Benefit Outweigh Impact on Supplier Revenue Model?

But many oppose the notion of subsidized use of apps, including zero rating, which allows use of some apps without the purchase of a data plan. That has proven quite popular with consumers in many parts of the developing world.

But some say zero rating is unfair to app providers, as it "turns the Internet into cable TV." It sometimes is hard to know what to make of such arguments.

Every app and service must have a viable revenue model to survive, even assuming there is clear value for end users. Content services, such as cable TV, subscription radio, streaming video services, subscription websites, magazines, newspapers,

And the Internet arguably is chaniging. Many of the new apps are content related. And content businesses have a few reliable revenue models, including subscriptions, advertising and sponsorship.

The argument against zero rating essentially is that any app provider should not have the right to choose a sponsorship model for business reasons of its own, just as it might choose a commerce, advertising or end user fee revenue model.

Some think that is a form of application blocking.

The problem these days is that nearly every dispute between Internet domain providers, content providers and access providers, mobile app store owners and app suppliers is viewed as some form of "application blocking."

How about viewing zero rating as a consumer-friendly choice with direct benefits for consumers who get to use valuable apps at lower cost than otherwide would be possible?

For millions of consumers in the developing world, zero rating is anything but a problem.

But some say zero rating is unfair to app providers, as it "turns the Internet into cable TV." It sometimes is hard to know what to make of such arguments.

Every app and service must have a viable revenue model to survive, even assuming there is clear value for end users. Content services, such as cable TV, subscription radio, streaming video services, subscription websites, magazines, newspapers,

And the Internet arguably is chaniging. Many of the new apps are content related. And content businesses have a few reliable revenue models, including subscriptions, advertising and sponsorship.

The argument against zero rating essentially is that any app provider should not have the right to choose a sponsorship model for business reasons of its own, just as it might choose a commerce, advertising or end user fee revenue model.

Some think that is a form of application blocking.

The problem these days is that nearly every dispute between Internet domain providers, content providers and access providers, mobile app store owners and app suppliers is viewed as some form of "application blocking."

How about viewing zero rating as a consumer-friendly choice with direct benefits for consumers who get to use valuable apps at lower cost than otherwide would be possible?

For millions of consumers in the developing world, zero rating is anything but a problem.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, August 2, 2014

Google Disappers as Part of Microsoft Update

If you own a Windows Phone 8.1 device, once you install the GDR1 update, the new software update removes all search options except for Bing, according to documentation for the update.

For all the attention paid to Internet services providers "not treating all apps equally," how about app providers and operating system providers? Facebook has blocked rival apps, for example.

Nor are the ISPs, necessarily bigger financial actors than app providers, and therefore a bigger threat to use of lawfual apps or exercise of market power.

AT&T’s market capitalization now is about $184.8 billion to Facebook’s $188.9 billion.

There always are gatekeepers in communications, content and information businesses, retailing, transportation and logistics, to name only a few industries. But relative ability to act as a gatekeeper changes over time.

For decades, executives debated whether "content or distribution was king." Depending on the decade, the answers have varied, sometimes favoring distributors and sometimes content providers.

These days, new actors have appeared.

In fact, some would argue, the new gatekeepers are the platform owners — companies like Apple, Google, Twitter, Facebook, Amazon, and even Spotify, the companies that shape information availability and access.

One might note that European Union antitrust officials have been investigating and challenging both Microsoft and Google for years.

One doesn't have to agree with many of these complaints or actions to observe, empirically, that gatekeepers in any market can, and do exist. But the key gatekeepers can change over time.

For all the attention paid to Internet services providers "not treating all apps equally," how about app providers and operating system providers? Facebook has blocked rival apps, for example.

Nor are the ISPs, necessarily bigger financial actors than app providers, and therefore a bigger threat to use of lawfual apps or exercise of market power.

AT&T’s market capitalization now is about $184.8 billion to Facebook’s $188.9 billion.

There always are gatekeepers in communications, content and information businesses, retailing, transportation and logistics, to name only a few industries. But relative ability to act as a gatekeeper changes over time.

For decades, executives debated whether "content or distribution was king." Depending on the decade, the answers have varied, sometimes favoring distributors and sometimes content providers.

These days, new actors have appeared.

In fact, some would argue, the new gatekeepers are the platform owners — companies like Apple, Google, Twitter, Facebook, Amazon, and even Spotify, the companies that shape information availability and access.

One might note that European Union antitrust officials have been investigating and challenging both Microsoft and Google for years.

One doesn't have to agree with many of these complaints or actions to observe, empirically, that gatekeepers in any market can, and do exist. But the key gatekeepers can change over time.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Next in T-Mobile US Effort to Gain Scale?

Deutsche Telekom reportedly does not consider Illiad’s bid to buy a majority stake in T-Mobile US to be a reasonable alternative to a purchase by Sprint. What happens next is key.

Illiad is considered a long shot bidder, even if T-Mobile US parent Deutsche Telekom benefits from a bidding war for T-Mobile US.

If you assume Illiad will have to find some other bid package that does rise to the level of serious competition for T-Mobile US, then a financially strong partner would have to be enticed to bid with Illiad.

It probably would not be Carlos Slim, the Mexican telecom magnate on the lookout for expansion opportunities. Slim has said the U.S. market requires too much capital, and Slim's friendship with AT&T CEO Randall Stephenson likely is an issue as well.

It won’t be Comcast, which is otherwise occupied by its effort to buy Time Warner Cable. Having recently exited the U.S market, Vodafone, which as the cash, likely does not have the interest.

Deutsche Telekom wants to exit the U.S. market as well, and Orange would not likely want to partner with its fiercest rival in the French market.

Some other U.S. firms likely have the resources, but not the immediate appetite. It is easy to toss around the names of firms such as Google, Microsoft or Apple, all of whom have handset and device interests in the U.S market,

The problem is constructing a value proposition that makes sense. All of those firms arleady could buy wholesale access if they wanted to run branded mobile Internet access operations of some sort. They wouldn’t need to own stakes in one of the underlying providers to achieve that goal.

Still, with T-Mobile US in play, some other combination of bidders could emerge. The investment bankers would like that. So would Deutsche Telekom.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, August 1, 2014

Will Microsoft Cloud Revenues Pass Amazon Web Services Revenue?

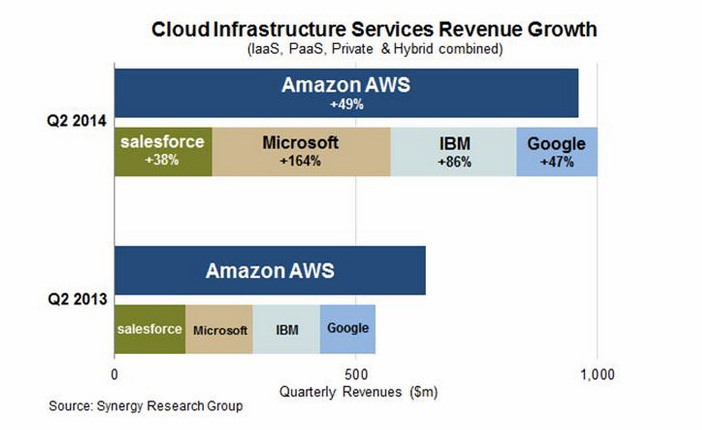

Microsoft and IBM lead revenue growth in cloud infrastructure services, according to Synergy Research Group.

Microsoft and IBM lead revenue growth in cloud infrastructure services, according to Synergy Research Group.

Amazon Web Services was in the second quarter 2014 still the largest single provider, but Microsoft has a blistering 164 percent revenue growth rate.

At such rates, if Microsoft can sustain it, Microsoft inevitably will pass AWS in cloud computing market share, as AWS is growing at perhaps a 49 percent rate.

Synergy Research estimates that quarterly cloud infrastructure service revenues (including infrastructure, platform, private and hybrid cloud) have reached $3.7 billion, with trailing twelve-month revenues comfortably exceeding $13 billion.

That figure excludes the value of software-driven cloud revenues, typically the largest single category of cloud services.

With the total market growing at over 45 percent, Microsoft and IBM have gained market share over the last four quarters while the share of AWS and Google is essentially unchanged from a year ago.

Total Amazon AWS revenues are now well in excess of $1 billion per quarter, with nearly all of that coming from cloud infrastructure services, Synergy Research estimates.

IBM and Microsoft also both claim quarterly cloud revenues of around $1 billion, but in their cases much of the cloud revenue comes from software, cloud-related hardware products or associated professional and technical services.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Financial Implications of 30% Market Share and Triple Play

Municipally-owned U.S. access or telecommunication networks always have been contentious, for obvious reasons: these are instances where tax-supported non-profit institutions compete with private firms.

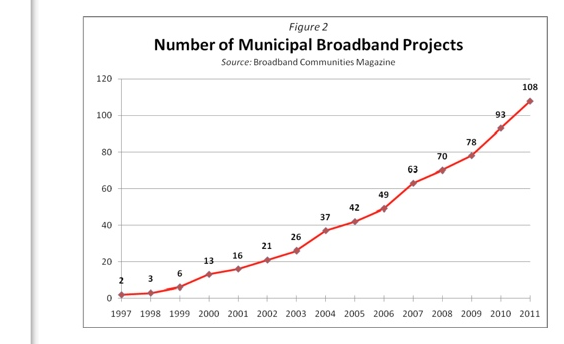

Between 2001 and 2011, the number of such municipal telecommunications initiatives grew from about nine to 108, an order of magnitude expansion in a decade.

Supporters might simply argue that “non-profits” compete with “for-profits” all the time. Museums, hospitals, gas, water and electrical utilities provide examples. Opponents say it is unfair for tax-advantaged entities to compete directly with non-subsidized entities.

The issue is “live” again since Federal Communications Commission Chairman Thomas Wheeler has promised he would stimulate more broadband competition by overriding state laws that presently restrict or ban municipal broadband networks.

The issue remains unsettled, though. Some believe the FCC has no authority to do so, and others think Congress could bar the FCC from taking such action.

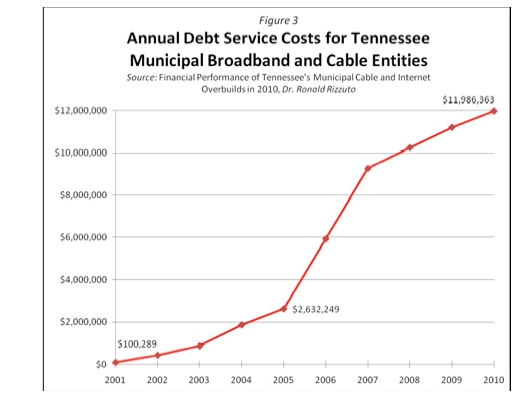

The historical record is mixed: some efforts have succeeded, while others have failed. Even those which have succeeded can leave big debt burdens for taxpayers.

Ignoring the policy issues, the level of risk for gigabit networks has grown, as the risk for fixed networks of all types--private or public--has grown.

There are several reasons. Structurally, markets with multiple competitors inherently mean the cost per customer grows dramatically, increasing risk.

Networks that are built with an expectation of 80 percent to 100 percent customer adoption rates have far lower stranded asset problems than networks where a reasonable assumption is that maximum adoption rates will be in the 30-percent range.

Basically, costs per paying customer are about three times higher in the 30-percent scenario, than in the 100-percent business case. That risk is the same whether the provider is a cable company or telco, a municipal broadband or an upstart ISP, especially if a network must reach all potential customers in a municipality.

Risk is mitigated if suppliers are able to “spot build” only where there is higher demand. That, for example, is why many competitive local exchange carrier operations can survive: they target clusters of business customers, and do not aim for ubiquity.

The triple-play (voice, video entertainment and high speed access) is important for marketing reasons. It also is important for financial reasons. Without the ability to sell three products to a customer, a service provider with 30 percent household adoption would be in grave danger of failure. At 33 percent household adoption, and three products to sell each customer, a service provider mimics the financial results one would expect of a 100-percent take rate for one service.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, July 31, 2014

What Revenue Replacement Options Can Telcos Actually Pursue?

It might go without saying that large access providers have different strategic problems and opportunities than smaller providers. For bigger providers, losing “billion dollar a year markets” means creating new markets of at least similar size, just to maintain current revenue magnitudes.

Growth requires more than that, of course. Smaller service providers face different issues, generally related to scale.

The mobile business, once highly fragmented, has become a scale business. The video subscription business has similar characteristics, meaning it is difficult for small providers to compete effectively.

Likewise, one might argue, many of the promising new markets, including many machine-to-machine or Internet of Things opportunities in the automotive, healthcare, energy, transportation, connected home and retail verticals, require national scale.

The same might be said of mobile wallet, mobile e-commerce or mobile payments opportunities.

In other words, creating new revenue sources to replace lost voice revenues often requires scale, human and capital resources that do not exist.

At the same time, some of the most-important new revenue sources, such as entertainment video, are themselves subject to disruption by online-delivered video.

Important niches do exist. The reason value added resellers and telephone interconnects and resellers in general exist is because it is inefficient for tier one service providers to provide service, or conduct sales operations, in many customer niches, small business being the salient example.

So the strategic issue remains: what can small service providers do to reposition themselves for vastly-different future markets? There are few obvious and easy answers. Small rural telcos, for example, do not have much “overhead” they actually can cut, to improve profit margins.

Few opportunities generally exist to significantly reposition to serve business customers, rather than consumer accounts.

The larger “rural service providers” (including Windstream, CenturyLink and Frontier Communications) already have made big acquisitions to reposition as providers of business customer services to a significant percentage of the U.S. customer base.

That option does not exist for most small telcos or cooperatives.

The latest study by the Telergee Alliance illustrates the issues. Rural and small telco profit margins are dropping, part of a three-year trend that saw an overall five percent drop over the last year. Profit margin on new or non-regulated services were up by about that amount, but margins on voice services dropped more than 15 percent.

Most--if not all--small telco video operations lose money, while mobile operations likewise face declining average revenue per user. Average revenue per user was $35.51 a month, down from $37.12 in 2009 and $40.93 in 2008.

Internet access revenues and margins for out-of-territory business-focused operations rose significantly. The issue is how many small telcos can conduct such operations.

Tier one telcos face different issues.

When big existing markets are shrinking, big new markets are required to replace those lost revenues, it goes without saying. But tier one service providers also have the scale to invest in, and operate, new services that require big service footprints, large numbers of potential customers, and account scale.

Machine-to-machine connections likely feature average revenue per connection of perhaps $4 a month. But those amounts could drop to $1 a month between now and 2020. Only a big firm can achieve enough scale to make that business case work.

There are 4.4 billion machines or devices now connected to each other or to servers, growing 10.3 billion by 2018, a study sponsored by Vodafone predicts. At $48 a year, that implies potential revenue of about $211.2 billion of connection revenue.

Assume average ARPU for an M2M device of about $2 a month, or $24 annually, in 2018. That implies revenue of about $247.2 billion.

That is a market big enough to be interesting to any number of service providers.

Compare that to global subscription TV revenues will grow at a compound annual rate of growth of 3.5 percent over the next few years to $236 billion in 2018.

In other words, M2M connectivity services of the “dumb pipe” sort represent a relatively near term revenue opportunity as big as all linear subscription video services. M2M likely is an opportunity for mobile service providers, while linear video mostly benefits fixed network service providers.

But it is worth considering the type of revenue upside. Linear video is an example of a “value-added application,” the sort of revenue source service providers constantly say they want, as opposed to “dumb pipe” access services.

But the M2M opportunity shows the danger of simple thinking about “dumb pipe,” as opposed to value-added services and applications. Both simple connectivity and apps can represent big opportunities. And the dumb pipe revenue arguably has more scale benefits, as a general purpose or horizontal service, compared to the vertical linear video subscription app.

Within three years, most firms will be embedding M2M into the actual products and services sold to customers, the Vodafone survey suggests.

But the M2M or Internet of Things market consists of “hundreds of micro-markets,” not a single industry, the report also suggests.

That likely has implications for the role of the mobile service provider in the ecosystem. If the application settings are highly fragmented, the easiest role for an access provider to adopt is “horizontal,” not “vertical.”

In other words, mobile service providers supply the communications function, not primarily vertical applications, much as the primarily value provided to business or consumer customers is mobile access (for phones, other personal devices and sensors), with a couple of general purpose applications (text messaging and voice).

In other words, mobile service providers likely can generate more gross revenue, at higher margins, by supplying general purpose “dumb pipe access” for M2M application suppliers, than they will in most vertical markets.

About 22 percent of 600 executives involved in machine-to-machine strategy say they already have at least one active M2M deployment in operation, up about 80 percent in 2014, compared to 2013, according to a new study sponsored by Vodafone and conducted by Circle Research.

The three leading industries, in terms of deployment, are the consumer electronics, energy and utilities, and automotive industries, each with a minimum of 30 percent adoption by respondent firms.

By 2016, the percentage of respondents with at least one M2M deployment will be 74 percent, the study predicts, based at least part on the embedding of M2M features into products such as thermostats and kitchen appliances.

Energy and utility respondents will have boosted M2M deployment to about 62 percent by 2016, based on smart meters and grid monitoring programs.

Use of M2M in the transportation and logistics verticals will be 57 percent in 2016, based largely on fleet logistics applications, and adoption in the healthcare and life sciences industry will be identical, the Vodafone survey found.

Automotive segment adoption will reach 53 percent, while retail deployment reaches 51 percent. M2M deployment in manufacturing will be at least 43 percent, though self reporting might be underestimating the actual state of deployment, given the widespread use of automation in manufacturing. Some respondents might not call what they already are doing an instance of M2M deployment.

Safety and security applications are the leading uses of M2M in automotive settings, partly because in many regions they are being driven by regulation, such as the eCall programme in the European Union.

Consumer electronics is at present the leading adopter of M2M, with the highest adoption

of external-facing strategies, at 71 percent.

Those applications primarily include tracking mobile assets including shipping containers. But

20 percent of all company executives surveyed in the consumer electronics segment already are selling connected devices directly to consumers.

Asset tracking is expected to be important in the energy and utility segment, monitoring in health care, connected car services in the auto industry, monitoring in manufacturing and connected cabinets or asset tracking being lead apps.

Early adopters tend to say productivity and cost savings are the deployment drivers, with projects tending to be in the internal processes areas, rather than external operations visible to customers.

At the moment, adoption of at least one active deployment is highest in the “Africa, Asia, Middle East” region, a rather broad category of limited analytical usefulness, one might argue. But 27 percent of executives surveyed in that region had projects underway.

The study included respondents from Australia, Brazil, China, Germany, India, Italy, Japan, the Netherlands, South Africa, South Korea, Spain, Turkey, the United Kingdom, and the United States.

In Europe, 21 percent of respondents reported they had at least one M2M project in action. In the Americas, 17 percent of executives said they had at least one project in progress.

But Vodafone expects that, by 2016, deployment profiles will be quite similar, with more than half of all respondents supervising actual deployments.

The survey, carried out by Circle Research, captured the views of more than 600 executives involved in setting M2M strategy in seven key industries across 14 countries.

Automotive is the most mature of the sectors where M2M is now seen as an enabler for additional services such as remote maintenance and infotainment. M2M adoption in energy and utilities is also growing rapidly as ‘smart’ home and office services such as intelligent heating and connected security gain popularity.

This uptake is being fuelled by the use of M2M in connected devices such as smart televisions and games consoles. The research shows that nearly three quarters of consumer electronics companies will have adopted some form of M2M by 2016, whether for new products, logistics or production.

Similarly, the report anticipates that 57 percent of healthcare and life sciences companies will have adopted M2M technologies by 2016.

All telcos have revenue issues. All face a loss of key legacy sources. But options for addressing those problems, aside from mergers and acquisitions, are severely limited in the small telco space.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...