Assuming both the Comcast acquisition of Time Warner Cable, and the AT&T bid to buy DirecTV are approved by regulators and antitrust authorities, the U.S. communications market (which now is becoming inseparable from the video entertainment services market) would be transformed.

Comcast would be the largest U.S. service provider, ranked by customer relationships, while AT&T would be only the second largest. Verizon would be a distant third.

Prospects for Sprint and T-Mobile US would still be significant in the mobile segment, but the really big change would be the change in what we might call the triple play services market that now defines the fixed network market.

Before one can analyze a market, one has to define a market. And that is the growing problem for the network services business, including high speed access, voice, video entertainment and mobile services, for both business and consumer segments.

Does one analyze each product segment, or all products sold by all contestants, even if some do not compete in all segments?

Even once those questions are answered, one has to decide whether to rank by subscriber or customer counts (consumer and business accounts included or disaggregated), by country where revenues are earned, or customers are served, or to use revenue (gross revenue or net revenue).

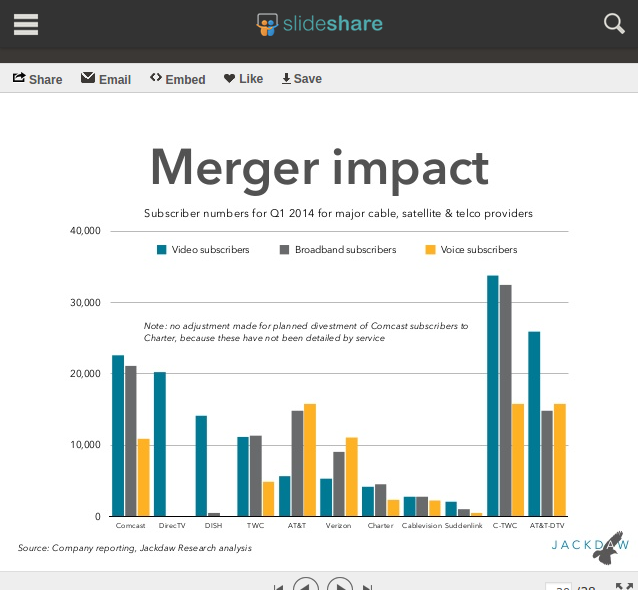

In the U.S. market, for example, measures of size based on mobile subscriber or revenues give different answers about which firm is bigger, AT&T or Verizon. And a mobile services ranking does not include Comcast, the biggest of the cable TV providers.

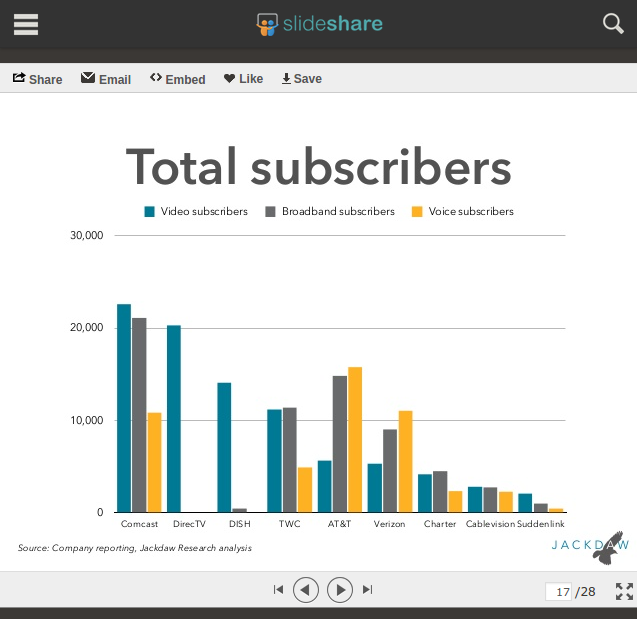

In the high speed services market, ranked by subscribers, Comcast clearly is the leader, while AT&T is number two and Time Warner Cable is number three.

Verizon is number four and CenturyLink is number five.

In video, Comcast in the biggest, ranked by subscribes, followed by DirecTV. Dish Network is number three, while Time Warner Cable is number four. AT&T follows at fifth and Verizon is sixth.

In voice services, AT&T is number one, ranked by customers, with Verizon and Comcast in second and third. Time Warner Cable is fourth. But many could note that Verizon and Comcast have almost the same number of voice customers.

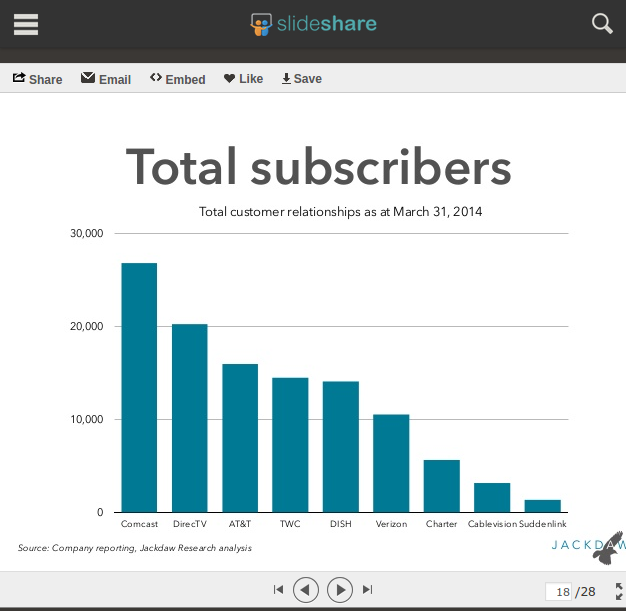

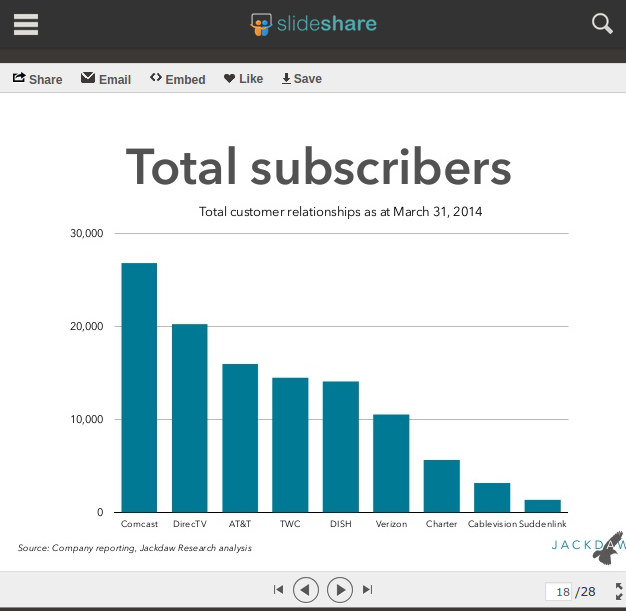

In terms of total customer relationships, across high speed access, video entertainment and voice segments, Comcast is the biggest, followed by DirecTV.

AT&T is third, followed by Time Warner Cable, then Dish Network. Verizon is sixth biggest.

All that would change if both the Comcast acquisition of Time Warner Cable, and the AT&T purchase of DirecTV are approved. In that case, Comcast would be the largest U.S. service provider, with AT&T the number two, with both companies far ahead of all the others.

Video and high speed access would be the key services for both firms.

Video Provider

|

Subscribers at

End of 1Q 2014

|

Net Adds in

1Q 2014

|

Net Adds in

1Q 2013

|

Cable Companies

| |||

Comcast^

|

22,601,000

|

24,000

|

(25,000)

|

Time Warner

|

11,359,000

|

(34,000)

|

(118,000)

|

Charter

|

4,355,000

|

13,000

|

(35,000)

|

Cablevision

|

2,799,000

|

(14,000)

|

(5,000)

|

Suddenlink

|

1,187,500

|

2,400

|

800

|

Mediacom

|

937,000

|

(8,000)

|

(1,000)

|

Cable ONE

|

524,563

|

(14,331)

|

(5,435)

|

Other Major Private Cable Companies*

|

6,655,000

|

(20,000)

|

(40,000)

|

Total Top Cable

|

50,418,063

|

(50,931)

|

(228,635)

|

Satellite TV Companies (DBS)

| |||

DirecTV

|

20,265,000

|

12,000

|

21,000

|

DISH

|

14,097,000

|

40,000

|

36,000

|

Total Top DBS

|

34,362,000

|

52,000

|

57,000

|

Telephone Companies

| |||

AT&T U-verse

|

5,661,000

|

201,000

|

232,000

|

Verizon FiOS

|

5,319,000

|

57,000

|

169,000

|

Total Top Phone

|

10,980,000

|

258,000

|

401,000

|

Total Multi-Channel Video

|

95,760,063

|

259,069

|

229,365

|

Broadband Internet

|

Subscribers at End

of 1Q 2014

|

Net Adds in

1Q 2014

|

Cable Companies

| ||

Comcast*

|

21,068,000

|

383,000

|

Time Warner

|

11,889,000

|

283,000

|

Charter

|

4,788,000

|

148,000

|

Cablevision

|

2,788,000

|

8,000

|

Suddenlink*

|

1,103,100

|

35,100

|

Mediacom

|

984,000

|

19,000

|

WOW (WideOpenWest)

|

756,700

|

16,700

|

Cable ONE

|

484,168

|

11,537

|

Other Major Private Cable Companies**

|

6,450,000

|

65,000

|

Total Top Cable

|

50,310,968

|

969,337

|

Telephone Companies

| ||

AT&T

|

16,503,000

|

78,000

|

Verizon

|

9,031,000

|

16,000

|

CenturyLink

|

6,057,000

|

66,000

|

Frontier^

|

1,873,000

|

37,000

|

Windstream

|

1,170,400

|

(500)

|

FairPoint

|

331,538

|

1,772

|

Cincinnati Bell

|

270,000

|

1,600

|

Total Top Telephone Companies

|

35,235,938

|

199,872

|

Total Broadband

|

85,546,906

|

1,169,209

|