An eight-year robust revenue growth streak has ended abruptly at mobile services supplier Axiata. The issue now is whether the dip is cyclical or structural.

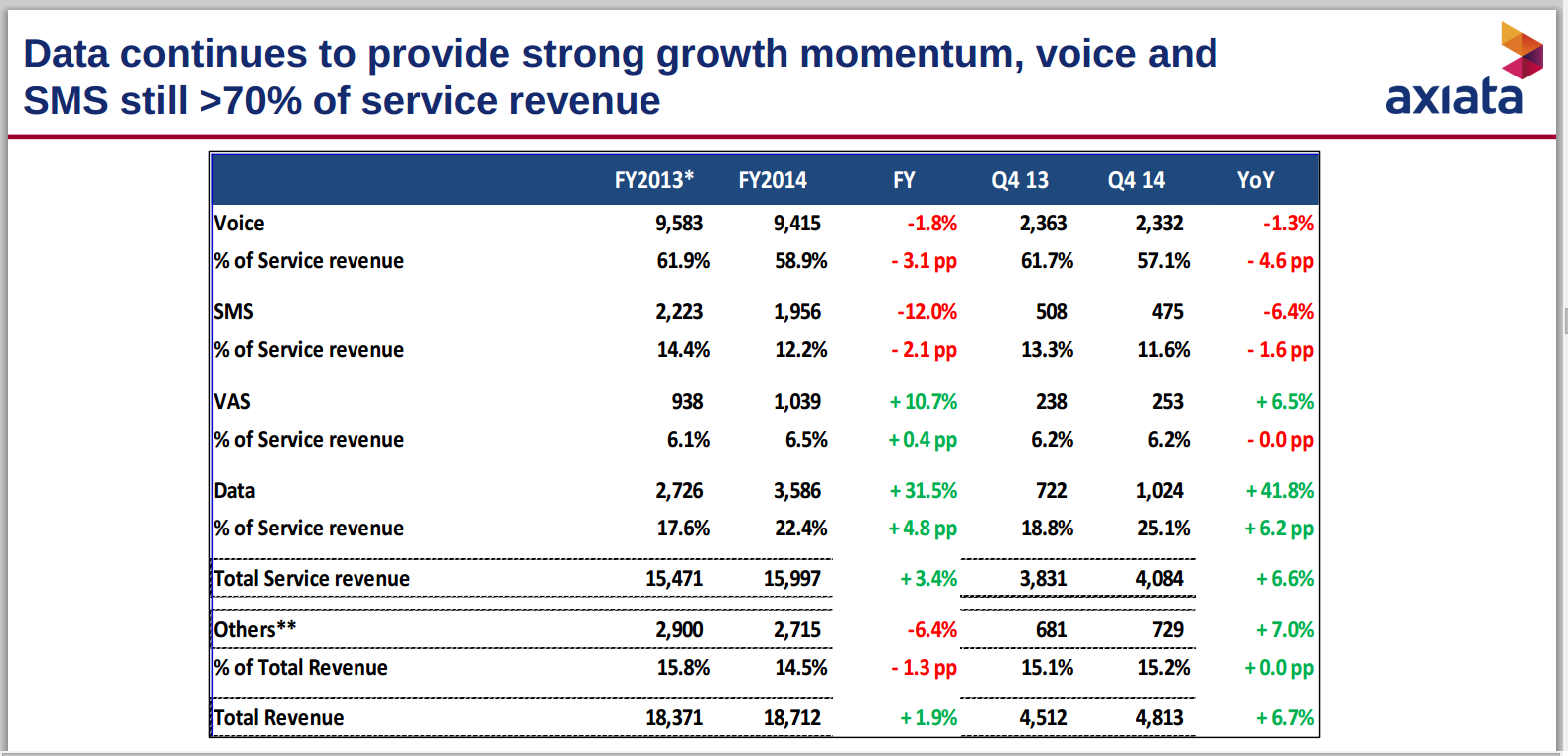

In many key respects, Axiata Group now faces business issues identical to those faced by other mobile service providers, namely robust growth in mobile data revenues, offset by losses of voice and text messaging revenue.

But slower economic growth, foreign exchange issues and investments played a role in Axiata 2014 results as well.

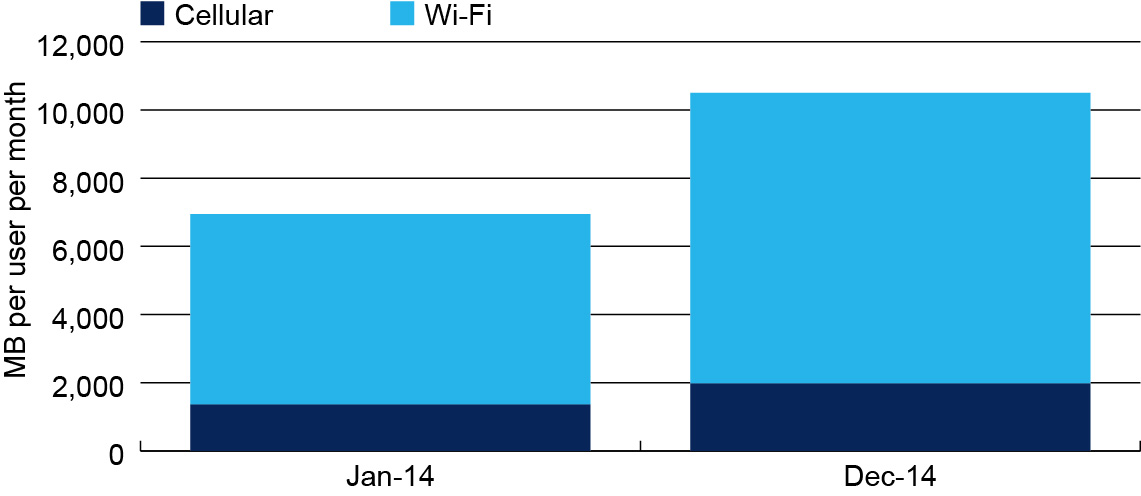

Not even robust mobile data revenue growth of 50 percent was enough to overcome business headwinds faced by Malaysia-based Axiata Group in 2014, which had a full-year 7.9 percent decline in net profit on a 1.9 percent growth in revenue, where the target had been 10 percent.

Axiata has an 84-percent dividend payout ratio, so any dip in revenue has key implications for profits.

Slow economic growth, currency issues and heavy capital investment were noted as reasons for the results, which were a reversal after about eight years of strong revenue growth.

Smart was the best performer with revenue growth of 36 percent and 60.5 percent earnings growth. Though voice revenue grew 19 percent, data grew 135 percent. Performance also was strong at the Robi, Dialog and Idea units, though 44 percent of revenue is earned at Celcom and 35 percent at XL.

Axiata's Malaysian mobile subsidiary Celcom fell 12 percent and revenue declined 3.5 percent.

In Indonesia, XL Axiata increased its revenue by 10 percent to 23.6 trillion rupiah ($1.8 billion).

Axiata also recorded a strong performance at its Sri Lanka, Bangladesh and Cambodian subsidiaries, and solid contributions from its affiliates in India (Idea Cellular) and Singapore (M1).