One of the bigger strategic issues in the traditional telecom business is whether a “mobile only” strategy is sustainable, or whether ownership of both fixed and mobile assets, in the same market, is a better approach, if it can be achieved.

With some exceptions, only the legacy, monopoly-era service providers have an easy choice. Since they already own the fixed network, and want the growth mobile provides, it is an easy choice to embrace both.

Attacking carriers tend, in most markets, to be mobile-only providers, in part because additional spectrum and government policy allows them to enter markets as attackers, and because the cost of building a fixed network is prohibitive.

The exceptions are North America and Western Europe, where attacking carriers sometimes are able to acquire both mobile and fixed assets, allowing them to operate as “full service” providers out of market.

In the U.S. market, for example, half of the top mobile operators are “mobile only,” while two (the legacy providers) own both fixed and mobile assets.

At least some observers might argue that a viable “mobile only” role can be sustained, long term, in the U.S. market. Some of us doubt that.

The reason is that neither of the two mobile-only businesses appears to have the scale to survive as independent entities, for the long term.

While a merger of the number-three and number-four service providers is theoretically possible, U.S. regulators have vetoed two separate efforts to merge assets--AT&T and T-Mobile US; and Sprint-T-Mobile US--within recent years.

Beyond that, other providers have the means and motivation to acquire the mobile-only companies. As both Comcast and Charter Communications, the two behemoths of the U.S. cable TV industry, will be getting into the mobile business, and since the business now is a scale game at the top, both T-Mobile US and Sprint offer ways for those two firms to enter the mobile business in a major way, with national footprints.

Other potential suitors also might exist. Dish Network has to create facilities or sell its licenses. And any number of other firms in the internet ecosystem might have reasons to consider such acquisitions, though such moves do not make as much sense as acquisitions by Comcast and Charter.

So, at least in the U.S. market, the answer to the strategy question might be that a “own both” strategy will apply.

That does not rule out some specialized “mobile-only” business models based on use of unlicensed or affordable shared spectrum. But such approaches are not likely to seek leadership of the traditional mobile market. It will simply be too competitive a market for any such undertakings.

In the near term, the U.S. mobile service provider market is grinding ahead, with subscriber growth extremely difficult in the saturated market.

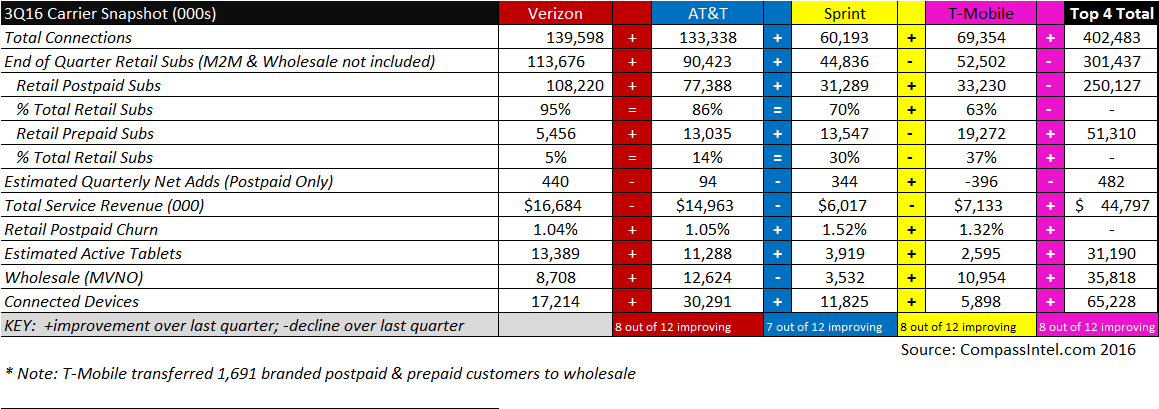

T-Mobile US added the most gross connections in the third quarter of 2016, adding two million gross accounts. AT&T added about 1.5 million gross new accounts.

The U.S. mobile market ended the quarter with about 5.2 million gross new connections gained by the top-four carriers, but a net connection gain of about 482,000 connections.

And many of those connections were lesser-revenue tablet or Internet of Things adds. A total of 1.3 million tablets were activated in the third quarter of 2016, for example.

AT&T and T-Mobile US both increased their overall service revenue, quarter over quarter. Sprint and Verizon experienced service revenue decline, quarter over quarter.

The bigger picture is that the question about grand strategy (mobile-only or mobile-plus-fixed) is likely to be settled in favor of “mobile-plus-fixed,” ultimately, at the top of the traditional mobile business.

What might happen with other specialized “untethered or mobile” business models remains unclear. Those approaches are almost certain to be employed by contestants in the internet ecosystem who have other roles, and see value in adding the access function.