Though--as always--different nations, regions and providers will face different business model changes in the next era of communications, a potentially disastrous possibility exists.

In the voice era, lower unit prices stimulated usage. That did not prevent voice prices--especially international and national long distance--from dropping by a couple orders of magnitude. But vastly-higher volumes sold partly made up for the retail unit price changes.

Some believe tougher problems await in the data era.

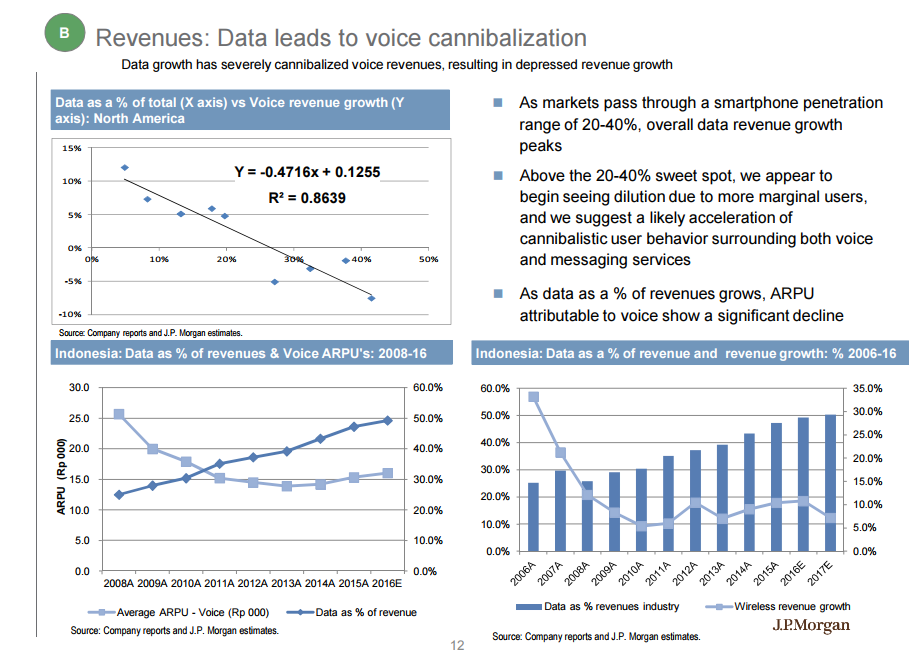

Even after accounting for Wi-Fi and new technologies and alternate business models, there will be still significant global wireless data demand that is not economically possible to serve,” says James Sullivan, J.P. Morgan head of Asia equity research.

In other words, demand will not match supply, in part because data revenue will not scale with capital investment, even if that was roughly the case with voice services. As voice prices dropped, usage exploded, so lower unit prices were somewhat balanced by more volume.

Declining value capture is paired with a significant, and ongoing, increase in capital intensity. In at least some cases, that will mean possible nationalizing of networks. In other cases, competitors might be forced to consider sharing network facilities, to stave off such intervention.

That would overturn nearly a half century of moves to privatize assets and introduce competition.

“Emerging market telcos have no choice but to fundamentally change the structure of industry assets through the unification of networks via nationalization, centralization under a regulated return utility, or more aggressive commercial network sharing,” argues James Sullivan, J.P. Morgan Chase Head of Asia Equity Research.

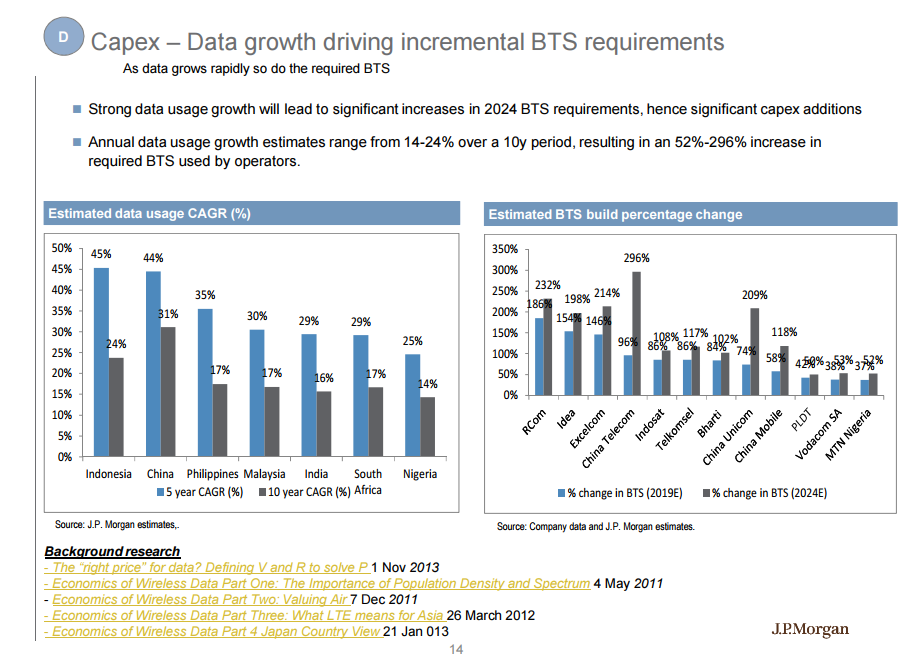

Simply, between now and 2024, telco capital investment and operating expense will climb, while revenue growth lags. But there also is regulatory risk. India, the Philippines, Thailand, Malaysia, Indonesia and Turkey are countries where capex pressures are the big problem.

Regulatory risks exist in Indonesia, Brazil, South Africa and Malaysia, he argues.

Markets with the potential for the most extreme margin compression include the Philippines, India and South Africa; while more defensive margin markets are Nigeria and China, says Sullivan.

Differential margin always has been a characteristic of the business. Universal service funds exist because it often is not possible to support universal communications in rural areas, for example.

Gross revenue and profit margin always has been higher in the business customer segments than in the consumer segments; higher in some geographies than others; higher in denser areas than in lower-density areas.

Gross revenues and profit margin also have varied by product line.

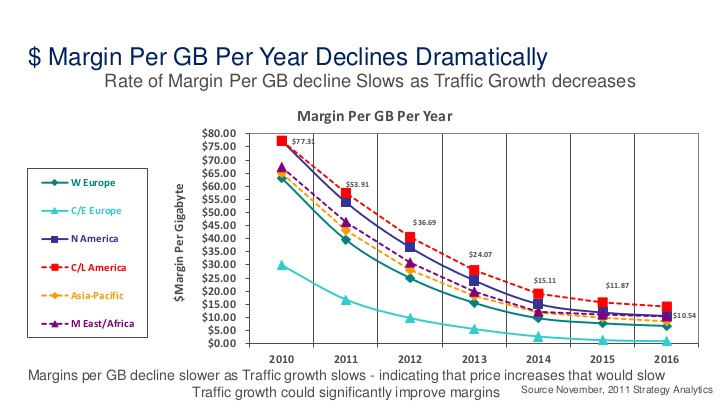

Sullivan’s argument is that there is something profoundly different about supply costs and revenue in the data era. Consider what mobile operators are doing in the U.S. market to accommodate burgeoning video content demand: they are zero rating content.

In other words, customer data plans are not charged when consumers view entertainment video. That is not an unusual practice, historically. It is the way linear video subscriptions, broadcast TV, broadcast radio and most other content businesses have operated.

But consider the capex implications: huge investments in capacity have to be made under conditions where the key drivers of demand (video) do not produce direct incremental revenue.

It is a huge challenge.

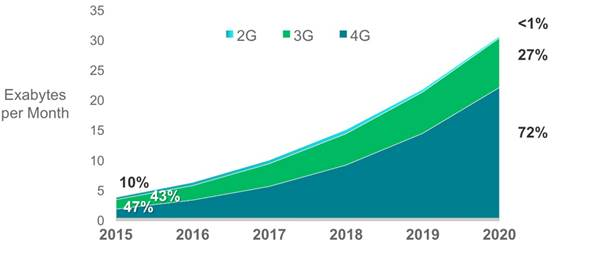

![Figure 2: Revenue per gigabyte of mobile broadband traffic, worldwide, 2011–2016 [Source: Analysys Mason, 2011]](https://lh4.googleusercontent.com/lqWQtnD67pxiXbmGP0nUnk9mLe9QlgiD-1yxOVDvsncYChctSzUST4DtkKA4OxcA_U2CRINrS6wWL-VcPfeEuZDupeNK5j0vd3R283Ig12QPi8qkGM2E9Gptf5Z0NarOu9Af4I6C)