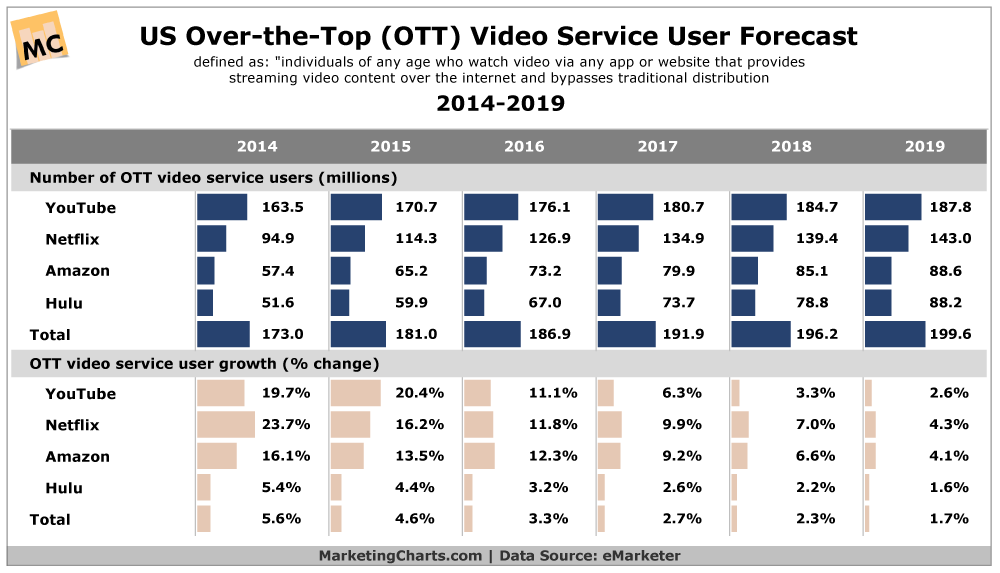

The decline of the U.S. linear subscription TV revenue might happen slower than you think, for a number of reasons. Between 2016 and 2019, for example, though the number of over-the-top subscriptions will grow--boosting the number of active accounts by perhaps 12.7 million units, according to eMarketer--revenue will not change as quickly.

To be sure, OTT account volume already has surpassed linear account volume. U.S. linear subscriptions in 2016 represent about 93.8 million subscriptions. Assuming linear accounts do not grow, or decline too fast, that might mean OTT, already the share leader in terms of total accounts (93.8 million 2016 linear accounts and 187 million OTT accounts), will represent as much as 68 percent of all video entertainment subscriptions.

But average revenue per account is highly disparate. Where a U.S. linear around drives between $80 and $120 a month in revenue, an OTT subscription might drive $7 to $11 per account, per month. In other words, linear accounts can represent as much as an order of magnitude more revenue (10 times) as an OTT subscription.

In 2016, U.S. OTT video revenues might have represented $7 billion. Linear video produced $102 billion.

Were OTT subscription revenues (advertising or transaction revenues also will be generated) to grow 10 times, that would still directly displace a bit less than the current value of linear subscription revenue.

One way of looking at the market is that a customer contemplating purchase of an entertainment video service can buy a single linear subscription, or perhaps 10 OTT accounts, and spend the same amount of money per month.

If one assumes that over-the-air broadcast TV can be gotten using an off-air antenna, for no monthly subscription price, and pre-recorded material from OTT, then the third bucket of content is “live sports” and, for a small number of customers, 24-hour news.

So the issue, long term, is which bundles of purchases allow a potential consumer to replicate all--or enough--of the wanted content using OTT sources only (and assuming over-the-air TV can be gotten at no incremental cost), and what that implies for total monthly spending.

Linear services are adding more features (including OTT or on-demand access), so the issue is not a simple “linear versus on-demand” dynamic.” Also, more linear content is being packaged in OTT form. And few customers want “all” the programming currently offered in big linear bundles. Relatively few want any of the highly-specialized channels, many do not want sports, most do not want news and off-air is an alternative for traditional broadcast network fare.

Logic suggests consumers will evaluate value against price, suggesting a workable set of OTT replacements, for most consumers, will offer “most” of what a linear subscription features, at lower price.

That implies lower revenue per account, and likely lower total monthly spending per user or per household. The reason is what happens in a typical product lifecycle. At some point, every popular product saturates, and revenue per account, as well as industry revenue, falls. Some might argue that OTT is a “new” industry with a “new” growth curve. Others might see OTT as the replacement product for linear delivery.

Both points of view can be correct, simultaneously. One other observation likely is germane. The internet tends to create product replacements that produce less revenue than the legacy business model. The phrase “trading digital dimes for analog dollars” illustrates the notion.

Since most of the primary underlying cost of content is driven directly by content rights access (perhaps 40 percent of total cost in the linear model), and since owners will act to protect those revenue streams, we might surmise that content costs are unlikely to fall much, in the transition from linear to OTT delivery.

source: eMarketer