Is 5G overhyped? Yes. Is the hype unwarranted? In the near term, perhaps. Long term? The global communications business might well prosper or fail based on new revenue streams created by 5G. So, long term, the hype is totally warranted.

Tuesday, April 4, 2017

Is 5G Overhyped?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

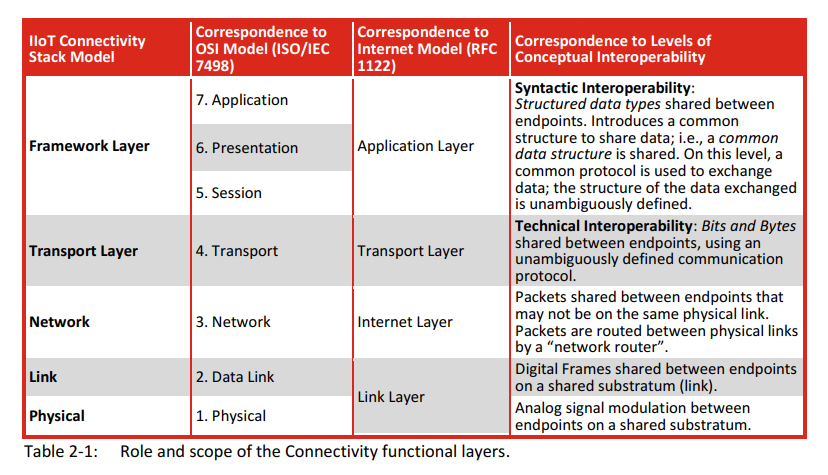

Industrial Internet Consortium Releases IIoT Connectivity Model

The Industrial Internet Consortium has released an extensive white paper on its model for industrial internet of things connectivity. As you might guess, the connectivity model is designed for technology developers, and corresponds, in general, to the Open Systems Interconnect seven-layer model.

As some of us might note, there are business analogies. With the embrace of OSI, applications now are written to be independent of access media and network platforms; as well as independent of devices and operating systems, to a large extent. In such an environment, though there still remain vertical integration opportunities, the basic framework is openness.

But that also means business models are less amenable to “lock in” based on specific protocols, networks or access media. So it is worth noting that, above the the “framework” layer (structured data) is the unnamed “business model” layer, where businesses with revenue models decide to use IIoT.

It is natural that ecosystem participants in the communications segments focus on “how” to achieve ubiquitous communications for IoT. Ultimately, as always is the case, business value will determine whether IoT is embraced, and therefore whether markets for communication services are created.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

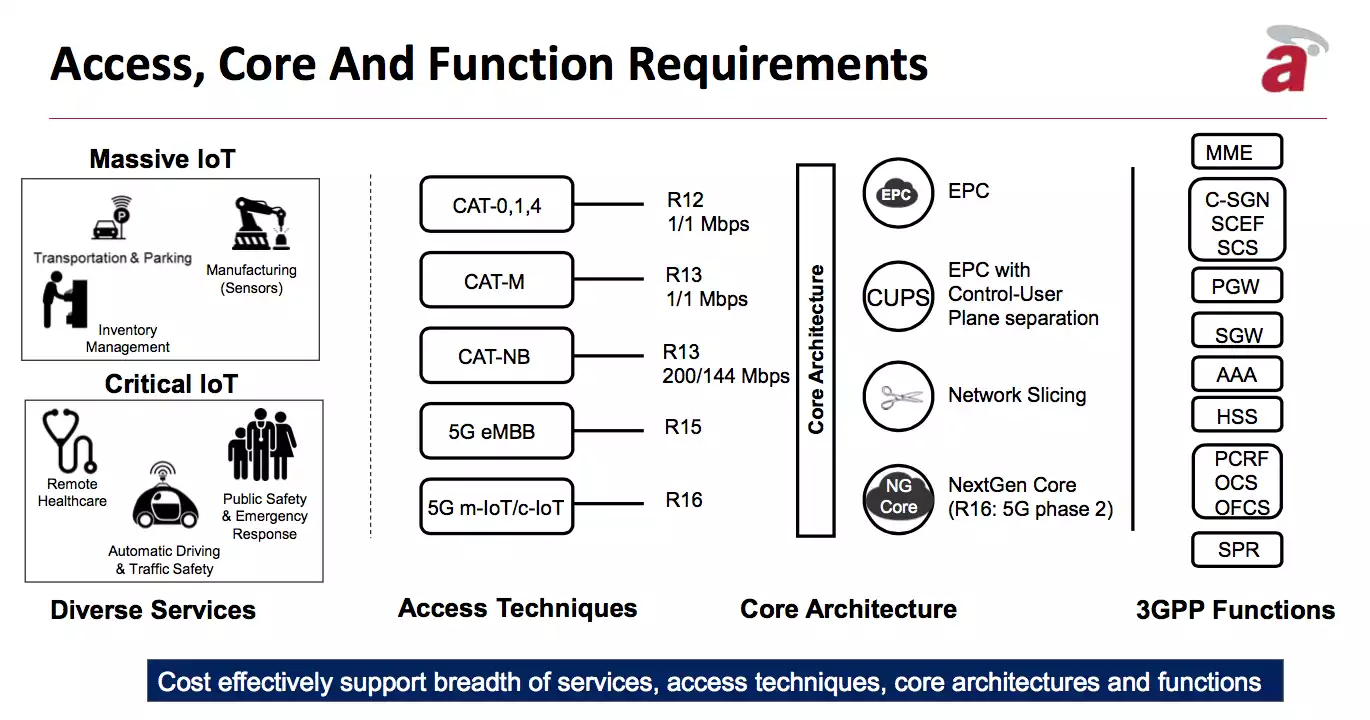

Does NFV Enhance or Replace Evolved Packet Core?

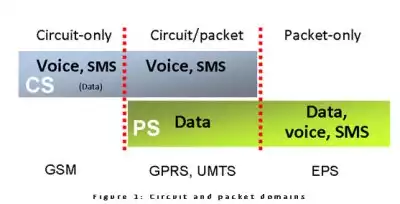

In many ways, network slicing features of coming 5G-compliant core networks builds on evolved packet core (EPC), the current framework for providing converged voice and data on a 4G Long-Term Evolution (LTE) network. The 2G and 3G networks use a different architecture, using

circuit-switched networks for voice and packet-switched networks for data.

Evolved packet core uses Internet Protocol, which is simpler and media independent. Standards for EPC were developed by the Third Generation Partnership Project (3GPP) in early 2009.

As always is the case, networking professionals can disagree about whether NFV either “improves or replaces” the EPC. Perhaps most would argue that NFV extends and builds upon EPC.

It might be somewhat subtle, but CIMI principal Tom Nollte says network slicing (a feature of 5G-compliant core networks) could have an impact in terms of “eliminating the expensive evolved packet core infrastructure that handles mobility in 4G networks.”

Most would probably argue that NFV virtualizes the EPC function. But that is where the nuances are important. If EPC is virtualized, is that a functional replacement of EPC by NFV networks using network slicing? It’s subtle. It might be most accurate to say that virtual replaces physical in the area of EPC functioning.

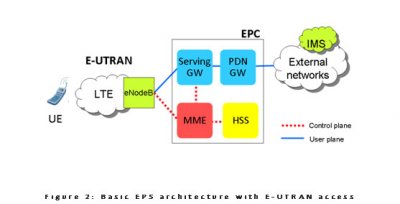

EPC also separates the control plane from the user plane, where control network is separate from the actual payload data, a move intended to reduce costs and network overhead, while improving ability to scale networks more easily (and at less cost) by reducing the amount of active elements.

The next evolution, many would argue, is network functions virtualization (NFV), a network architecture concept that uses “information technology” approaches to virtualize entire classes of network node functions, making them building blocks that can be connected or chained together to create communication services.

One way to look at such an NFV network is that the business case can drive the configuration of network capabilities for each specific application (at least to the extent the network can be customized for latency, security, geography, bandwidth or quality). Historically, the goal of every next-generation network was to create the ability for bandwidth on demand, something NFV builds on, but augments.

So it might be an irrelevant argument (“how many angels can stand on the head of a pin”), but virtualizing networks using network slicing and NFV might either been seen as “improving” existing network functions, or as “replacing” them.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, April 3, 2017

Who Will Develop Shared Spectrum Facilities?

Since 5G networks will build on other developments, such as the latest generations of 4G, core network virtualization, new spectrum access methods (shared spectrum) and millimeter wave frequencies and small cells, business models are likely to be evolutionary, rather than a “flash cut,” compared to prior mobile network generations.

For example, development of new commercial method for spectrum sharing in the 3.5-GHz band are not a formal part of the 5G standards process. But shared spectrum access is expected to be a staple of 5G network access methods.

Likewise, the release of more millimeter wave spectrum partly is, and partly is not, part of the 5G standards process. Similarly, small cell deployments, additional distribution fiber deployments, new radio technology and even open source efforts will eventually contribute to enabling and improving the 5G business model.

Perhaps oddly, the 3.5-GHz Citizens Broadband Radio Service (CBRS) being introduced in the U.S. market might see some unusual demand patterns. CBRS uses a three-tier access priority system, with existing licenses having interference protection rights from commercial users, while a a second tier offers priority access, while a third tier operates much as does Wi-Fi (best effort access).

The Priority Access Licenses (PAL), expected to be made available at auction, and with interference rights over the “best effort if capacity is available” General Authorized Access (GAA) tier of service, might be considered the preferred choice of mobile service providers, who have tended in the past to require quality-of-service protections.

The GAA spectrum would allow licensees the right to use 10 MHz channels for two three-year periods (3550–3650 MHz). And that is the issue: the six-year license duration limits the attractiveness of PAL for mobile operators who, in the U.S. market, are used to perpetual license terms, argues Senza Fili principal Monica Paolini.

As a result, she argues, the strongest interest might lie in use of the license-exempt GAA tier, which will effectively represent a new capacity option that is similar to Wi-Fi. That might have other repercussions as well.

If GAA spectrum can be used by any entity without a license, then CBRS can be built out by property owners in the same way they use Wi-Fi. That might effectively limit use of CBRS capacity by mobile operators

Also, CBRS access using GAA will allow venues to block use of other temporary Wi-Fi access points (consumers using their own devices, for example).

That also increases the likelihood that neutral host approaches could develop on a fairly widespread basis, eventually. The advantage there is that each service provider could use CBRS facilities without building in-building infrastructure. The disadvantage is that mobile service providers and others using a neutral host network would not be able to control the facilities to the same extent as if each provider supplied their own radio infrastructure.

So much remains to be discovered, in terms of the ultimate pattern of CBRS license preferences by commercial users (such as mobile or cable operators), venue owners (building owners and managers) or third-party developers of CBRS indoor access facilities.

If the present Wi-Fi pattern develops, then venue owners will develop CBRS access services that resemble today’s Wi-Fi. In principle, new neutral host facilities could develop, with a property owner or third party operating the radio infrastructure, and offering access to all who wish to partake. Unclear is the amount of demand for priority access approaches that resemble today’s mobile licenses.

Potential regulatory changes that would extend PAL licenses for longer durations also could have an impact. If that were to happen, then CBRS using PAL would more closely resemble traditional mobile licensing.

If one had to make a guess today, it might be that most smaller locations eventually will have CBRS operating just as Wi-Fi does today, with a property owner or tenant making the decision to create a small cell running a CBRS network using the GAA access method, just like they would operate a Wi-Fi network.

Neutral host is going to make more sense at large venues, though it remains unclear how scale will become a factor, favoring larger service providers rather than individual venue owners.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Charter Does Not Have to Overbuild, FCC Says

Charter Communications will not be required to overbuild (compete with an existing cable operator) as part of its acquisition of Time Warner Cable, the U.S. Federal Communications Commission has ruled.

That preserves the collegial structure of the U.S. cable TV industry, which historically has held to a practice of not competing with other cable operators, even if such competition is lawful. Basically, as industry execs have privately said, that “no competition” behavior has meant cable had the “best of all possible worlds, able to operate an an unregulated monopoly.”

That remains only partly true now that U.S. telcos and cable operators compete head to head, with the same key product lines, virtually everywhere. But the historic restraint (no competing with another cable company) remains largely intact.

The big changes will come as Comcast and Charter Communications enter the mobile and OTT streaming businesses, which require national scale. In such areas, Comcast and Charter will “compete” with other cable operators at least in the OTT video area. In that sense, the “competition” will be indirect, similar to the notion of a cable operator competing with Netflix.

Even so, the competition will more theoretical than practical, as smaller cable operators will not have the scale to compete in the OTT streaming services market. It is virtually certain neither Comcast nor Charter would directly challenge other cable operators in the core fixed networks business.

In the mobile business, it is possible local cable partners might, in many cases, also act as marketing and infrastructure partners with either Comcast or Charter or both. Despite that, Comcast and Charter will be trying to market services to customers served by other cable operators. No doubt both firms will do everything possible to minimize the perceived degree of competition and revenue threat.

As a condition of FCC approval of the acquisition, the FCC under the Obama administration had required that Charter build internet access facilities to about a million households that currently have service from other cable operators.

As you would expect, the smaller rural cable operators that would have faced new competition from Charter opposed the provision.

As a condition of approval for its acquisition of two cable companies, Charter in May 2016 agreed to extend high-speed internet access to two million potential customers within five years, with one million served by an existing cable competitor. That would have created new cable operator competition in those overbuilt areas for the first time.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

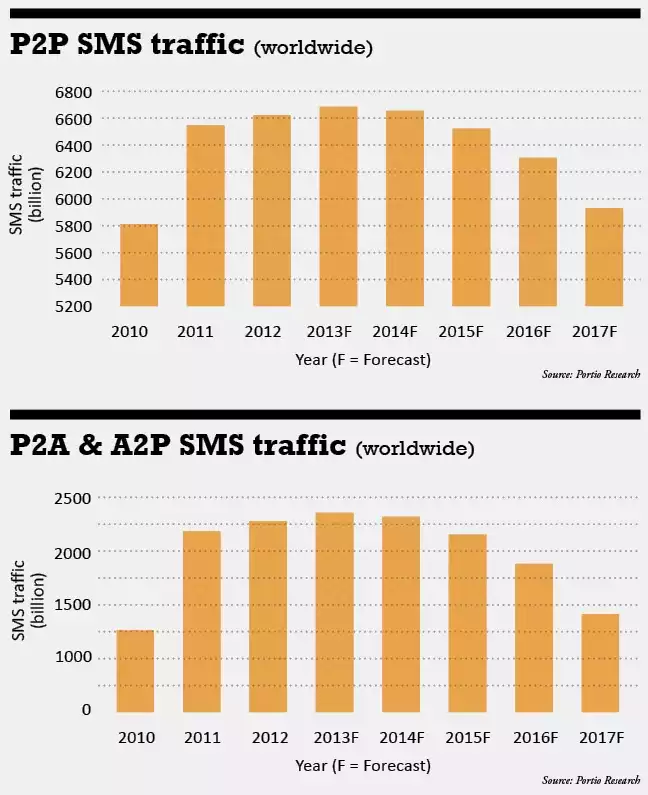

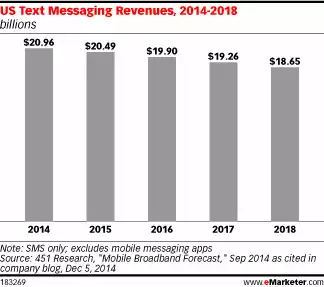

Text Messaging Revenue Opportunities Shift to Marketing, Customer Service, Other Business Revenue Models

New findings from Juniper Research forecast that OTT messaging applications, such as WhatsApp and Snapchat, will see adoption grow from 2.3 billion unique users in 2016 to 4.2 billion by 2021 representing a growth of over 12 percent CAGR (compound annual growth rate).

It anticipates that players will begin focusing their strategies around the development and provision of artificial intelligence (AI) chatbot tools. In other words, the revenue upside now is seen as marketing, not consumer direct revenue.

That is one example of a broader trend, namely the decline of voice and messaging revenues and the shift of such apps to “features” rather than revenue drivers. To be sure, some revenue still is made from voice and text messaging, and no mobile service provider would dare market a mobile service that did not support voice and messaging.

From time to time, a supplier might ponder offering services that use over the top voice and messaging, with no carrier voice and messaging capability. So far, that business model does not appear to be appealing.

To be sure, traffic or usage is different from “revenue earned from providing such usage,” but consumers globally simply are talking and texting less using carrier services, and substituting OTT voice and messaging, or using social media as a substitute in many cases.

That explains the new emphasis on use of text messaging as an advertising or business-to-business tool.

Juniper Research predicts that OTT players will reposition their messaging platforms as customer relationship management tools, for example.

By leveraging AI technology, these OTT apps--it is hoped--will create a service that drvies revenue because it offers a new level of consumer engagement and customer service.

The other interesting implication is that these new customer service and marketing tools will be built on use of artificial intelligence tools.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

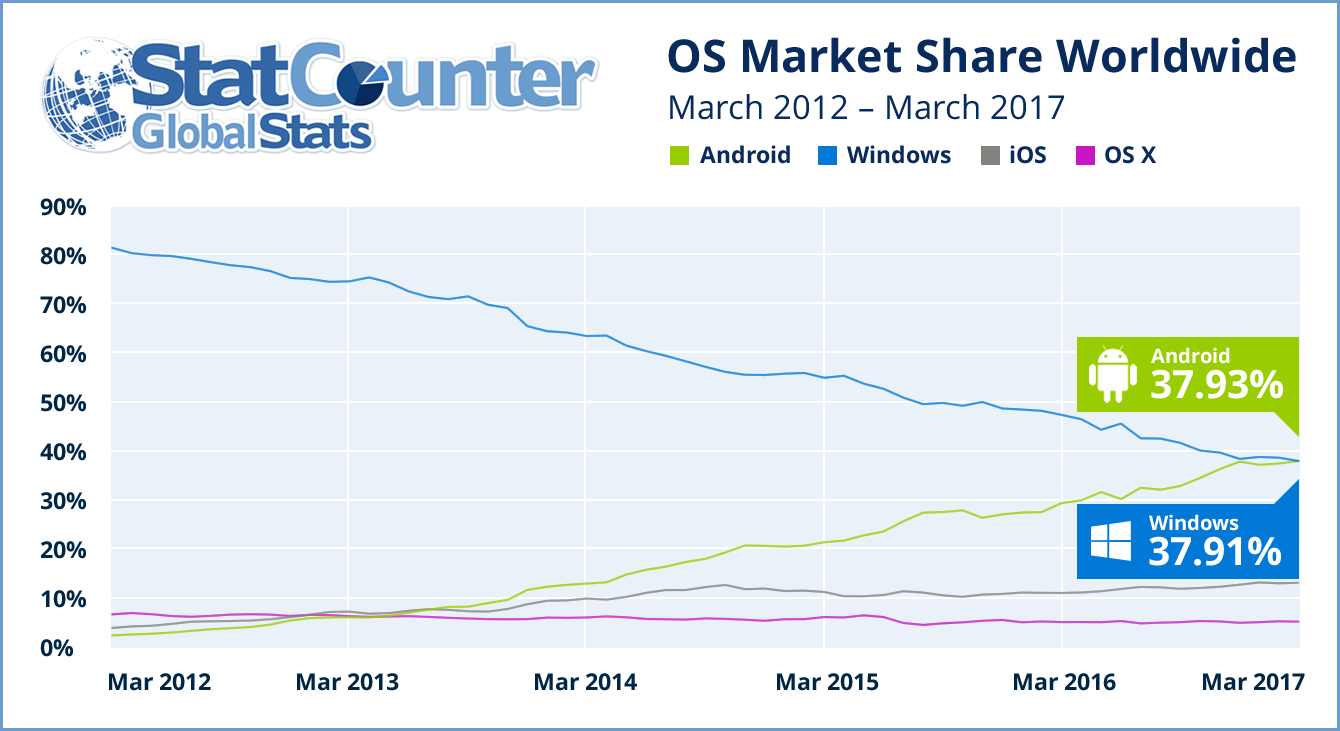

End of An Era: Android Passes Microsoft Globally as Top OS

Some milestones are turning points. Some turning points illustrate that an era has passed. Even if the fact will surprise virtually nobody, it is worth noting that, in March 2017, for the first time ever, Android passed the Microsoft operating system as the world’s most popular operating system (OS) in terms of total internet usage across desktop, laptop, tablet and mobile devices combined, according to StatCounter.

Granted, you might argue the OS share was a tie. In March of 2017, Android topped the worldwide OS internet usage market share with 37.93 percent usage, compared to Windows, with 37.91 percent share. Five years ago, Android had market share of about 2.4 percent, notes

Aodhan Cullen, CEO, StatCounter.

That noted, Microsoft Windows still dominates the worldwide operating system desktop market (PC and laptop) with a 84 percent internet usage share in March.

“Windows won the desktop war but the battlefield moved on,” said Cullen.

In substantial part, you can credit use of smartphones In Asia for Android’s global growth. In Asia, Android represents 52.2 percent of internet-using device operating systems, compared to 29.2 percent share for Windows.

In other regions, Windows retains its lead. In North America Windows had 39.5 percent share in March, followed by iOS at 25.7 percent and Android at 21.2 percent.

In Europe, Windows had 51.7 percent, with Android at 23.6 percent.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...