Concern about the "end of Moore's Law" has been expressed for decades. And there are clear constraints on current platforms. It remains to be seen what can happen with new platforms. But many believe there are a range of options to support continued progress, by tweaking both software and hardware.

Wednesday, June 7, 2017

No End to Moore's Law Rates of Improvement?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Why AI Investment is Going to (Initially) Disappoint

Despite the promise of big data, industrial enterprises are struggling to maximize its value. A survey conducted by IDG showed that “extracting business value from that data is the biggest challenge the Industrial IoT presents.”

Why? Abundant data by itself solves nothing, says Jeremiah Stone, GM of Asset Performance Management at GE Digital.

Its unstructured nature, sheer volume, and variety exceed human capacity and traditional tools to organize it efficiently and at a cost which supports return on investment requirements, he argues.

At least so far, firms "rarely" have had clear success with big data or artificial intelligence projects. "Only 15 per cent of surveyed businesses report deploying big data projects to production,” says IDC analyst Merv Adrian.

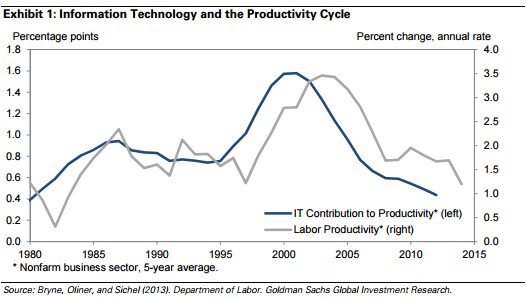

We should not be surprised. Big waves of information technology investment have in the past taken quite some time to show up in the form of measurable productivity increases.

In fact, there was a clear productivity paradox when enterprises began to spend heavily on information technology in the 1980s.

“From 1978 through 1982 U.S. manufacturing productivity was essentially flat,” said Wickham Skinner, writing in the Harvard Business Review.

In fact, researchers have created a hypothesis about the application of IT for productivity: the Solow computer paradox. Yes, paradox.

Here’s the problem: the rule suggests that as more investment is made in information technology, worker productivity may go down instead of up.

Empirical evidence from the 1970s to the early 1990s fits the hypothesis.

Before investment in IT became widespread, the expected return on investment in terms of productivity was three percent to four percent, in line with what was seen in mechanization and automation of the farm and factory sectors.

When IT was applied over two decades from 1970 to 1990, the normal return on investment was only one percent.

This productivity paradox is not new. Information technology investments did not measurably help improve white collar job productivity for decades. In fact, it can be argued that researchers have failed to measure any improvement in productivity. So some might argue nearly all the investment has been wasted.

Some now argue there is a lag between the massive introduction of new information technology and measurable productivity results, and that this lag might conceivably take a decade or two decades to emerge.

The problem is that this is far outside the window for meaningful payback metrics conducted by virtually any private sector organization. That might suggest we inevitably will see disillusionment with the results of artificial intelligence investment.

One also can predict that many promising firms with good technology will fail to reach sustainability before they are acquired by bigger firms about to sustain the long wait to a payoff.

So it would be premature to say too much about when we will see the actual impact of widespread artificial intelligence application to business processes. It is possible to predict that, as was the case for earlier waves of IT investment, it does not help to automate existing processes.

Organizations have to recraft and create brand new business processes before the IT investment actually yields results.

One possibly mistaken idea is that productivity advances actually hinge on “human” processes.

Skinner argues that there is a “40 40 20” rule where it comes to measurable benefits. Roughly 40 percent of any manufacturing-based competitive advantage derives from long-term changes in manufacturing structure (decisions about the number, size, location, and capacity of facilities) and basic approaches in materials and workforce management.

Another 40 percent of improvement comes from major changes in equipment and process technology.

The final 20 percent of gain is produced by conventional approaches to productivity improvement (substitute capital for labor).

In other words, and colloquially, firms cannot “cut their way to success.” Quality, reliable delivery, short lead times, customer service, rapid product introduction, flexible capacity, and efficient capital deployment arguably were sources of business advantage in earlier waves of IT investment.

But the search for those values, not cost reduction, were the primary sources of advantage. The next wave will be the production of insights from huge amounts of unstructured data that allow accurate predictions to be made about when to conduct maintenance on machines, how to direct flows of people, vehicles, materials and goods, when medical attention is needed, what goods to stock, market and promote, and when.

Of course, there is another thesis about the productivity paradox. Perhaps we do not know how to quantify quality improvements wrought by application of the technology. The classic example is computers that cost about the same as they used to, but are orders of magnitude more powerful.

It is not so helpful, even if true, that we cannot measure quality improvements in some agreed-upon way that produce far better products sold at lower or same cost. Economies based on services have an even worse problem, since services productivity is both difficult and hard to quantify.

The bad news is that disappointment over the value of AI investments will inevitably result in disillusionment. And that condition might exist for quite some time, until most larger organizations have been able to recraft their processes in a way that builds directly on AI.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, June 6, 2017

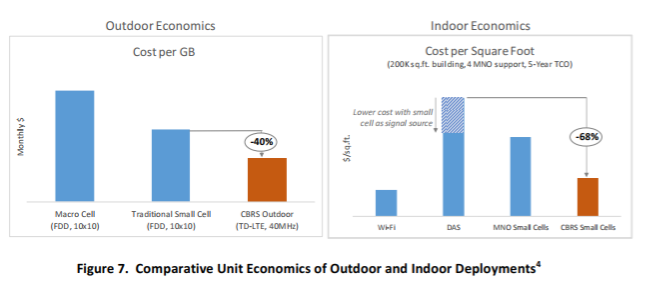

CBRS Neutral Host Precedent: Enterprise Wi-Fi

There is a model for neutral host deployments using the Citizens Broadband Radio Service "shared spectrum" approach: enterprise Wi-Fi.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

5G for Enterprise

The thing about 5G is the wide range of potential use cases, from consumer mobile internet access to enterprise private networks, new forms of indoor "neutral host" facilities and many new "narrowband" applications where bandwidths under 1.5 Mbps are the goal.

Since 5G will support virtualized networks very much like virtual private networks, ideally as a native feature, there should be lots of room to create optimized enterprise networks.

Since 5G will support virtualized networks very much like virtual private networks, ideally as a native feature, there should be lots of room to create optimized enterprise networks.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"All of the Above" Tells Us Very Little About Future Revenue Sources

When a new market is developing, and the answer to the question “where will the growth happen?” is “all the above,” we know we essentially have no idea what will happen. And that seems to be the case for the Citizens Broadband Radio Service, which will support about 150 MHz of new spectrum in the 3.5 GHz range that can be used for mobile internet access, enterprise networks or other purposes we have not yet explored fully.

To a large extent, we might say they same about prospects for 5G, where “everyone” expects applications in the consumer smartphone internet access area, but also in the fixed internet access area, internet of things and low-latency applications areas.

Still, nobody can be too sure which of those use cases will be dominant, and when, though given the size of existing mobile internet access markets, 5G might well see the greater part of revenues in the “enhanced mobile broadband” area.

On the other hand, the most-significant new development could be huge new markets for pervasive computing (internet of things), representing billions of new connections.

It remains unclear how use cases and revenue models will develop for shared spectrum platforms such as the Citizens Broadband Radio Service. At the moment, the conventional wisdom is that there will be opportunities in consumer and business markets, as primary or secondary access mechanisms, as indoor or outdoor networks.

CBRS obviously could be used to support consumer or business internet access, mobile or fixed wireless, enterprise apps, neutral host facilities that support indoor mobile access by all major mobile providers, or play other roles, such as allowing in-building access specialists (think Boingo) to support new indoor communications services.

In other words, more so than has been the case for general purpose mobile platforms, CBRS could enable industrial or vertical market applications for manufacturing, energy or healthcare, the Federal Communications Commission says.

The Citizens Broadband Radio Service uses a three-tiered access framework, dynamically managed in much the same way Television White Spaces networks work

CBRS uses three tiers: Incumbent Access, Priority Access, and General Authorized Access.

Incumbent Access users include authorized federal and grandfathered Fixed Satellite Service users currently operating in the 3.5 GHz Band. These users will be protected from harmful interference from Priority Access and General Authorized Access users.

The Priority Access tier consists of Priority Access Licenses (PALs) that will be assigned using competitive bidding within the 3550-3650 MHz portion of the band.

Each PAL is defined as a non-renewable authorization to use a 10 megahertz channel in a single census tract for three-years.

Up to seven total PALs may be assigned in any given census tract with up to four PALs going to any single applicant. Applicants may acquire up to two-consecutive PAL terms in any given license area during the first auction.

The General Authorized Access tier is licensed-by-rule to permit open, flexible access to the band for the widest possible group of potential users, on the Wi-Fi model.

General Authorized Access users are permitted to use any portion of the 3550-3700 MHz band not assigned to a higher tier user and may also operate opportunistically on unused Priority Access channels.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

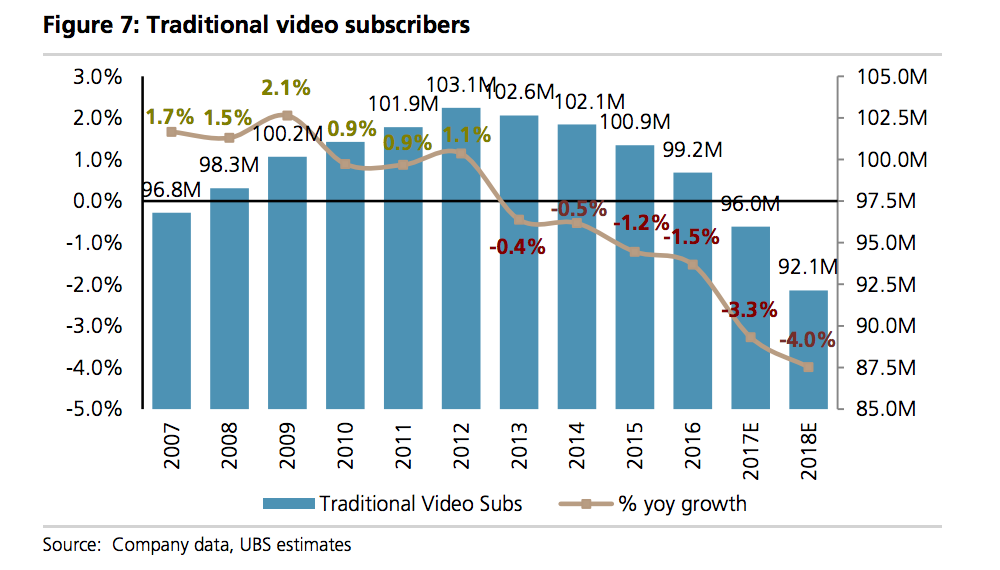

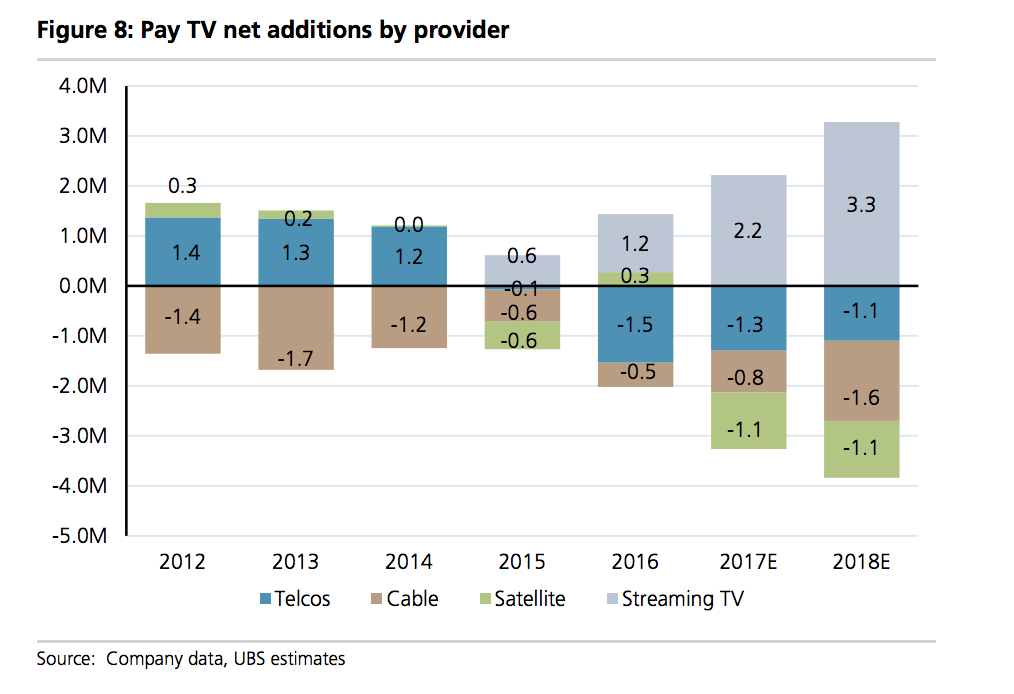

Inflection Point for Linear Video?

Nobody knows yet whether an inflection point has been reached in the linear video subscription business, but it arguably has happened. If so, that means the rate of change will increase significantly, and result in faster rates of account decline.

It is not a new problem, at least in developed markets, where every legacy service has faced maturity and then decline.

“Everyone” expects streaming services to be the replacement product, with a couple significant potential implications. Average revenue per account or per user will tend to fall, as streaming services cost far less than linear video subscriptions.

The move to “skinny bundles” (smaller packages of channels that cost less) also is driving the lower ARPU.

Eventually, though, as linear subscriber numbers really start to fall, there will be a bifurcation of revenue. Today, linear video is a two-sided market, with distributors earning revenue both from advertisers and subscribers.

What already is developing in the streaming market are revenue models that rely only on subscription fees (Netflix) or advertising (Facebook, YouTube) or transactions (Amazon Prime).

What obviously happens is that the linear services will suffer on several fronts, losing subscription revenue; losing advertising revenue and losing profit margins.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

NFV and AI: the How and the Why

With the ability to quickly analyze massive amount of consumer behavior and data, mobile devices with artificial intelligence applications might ultimately make it possible for the network itself to adapt to the needs of the end users, reconfiguring for bandwidth and speed dynamically as the end user population moves around.

In that sense, AI might create new value from virtualized networks. Network functions virtualization always has been about increasing network agility and reducing friction, allowing services and bandwidth to be immediately turned up, reconfigured or torn down.

But AI will create the business rationale for doing so.

In that sense, NFV is "how" networks can be made more liquid, and efficient enough to support many new business cases that require lower cost. AI will create the insights that drive "why" network features need to be enabled and changed.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

Uh Oh: Big AI Circular Deals

So now we have a new wrinkle to add to the “potential AI bubble” thesis: circular deals between AI infra suppliers (chips and compute platfo...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...