It is terribly difficult to imagine your own business operating under conditions of absolute abundance, when the key inputs are relatively scarce, and therefore, costly.

Unthinkably large and important businesses have been built on apparently crazy assumptions, the most important of which turns out to be the assumption that key enabling inputs, though hugely expensive and highly limited in performance, eventually, because of Moore's Law, be rendered very cheap.

So cheap that the phrase "computing wants to be free" or "bandwidth wants to be free" actually make sense, in terms of performance-cost relationships.

It can be argued that Microsoft’s business model, and that of Netflix, were based on astounding assumptions, namely that, as Moore’s Law continued to operate, Microsoft could assume the cost of computing would be very low, to free.

Likewise, Netflix assumed that Moore’s Law, applied to bandwidth, meant that, eventually, bandwidth sufficient to support a video streaming service would be possible, and virtually free.

But if one understands the arguments that “computing will be nearly free,” or that “bandwidth will be nearly free,” then you will understand the argument that “cars will be nearly free.”

Yes, assume your business (even as a auto manufacturer) model has to assume that vehicles themselves will be “nearly free” in terms of cost. That might sound crazy, but Microsoft and Netflix both based their business models on “near zero pricing” of a key input and enabler.

Will automobiles of the future become “mobile real estate, a data pipe, equivalent to telecom spectrum,” asks Morgan Stanley auto and mobility analyst Adam Jonas. To be clear, Jonas does not mean “pipe” as in “access pipe.”

He means a platform for data harvesting, machine learning and content delivery. In other words, autos as data repositories that can be mined, using artificial intelligence, to glean insights useful to third parties that will pay for access to those data stores.

“In the Auto 2.0 business model, we see 100 percent of the revenue and profit eventually coming from the operation of vehicles in a network,” said Jonas.

That might sound crazy, but it is the sort of analysis that underpinned the business models adopted by Microsoft, Netflix and arguably most other “digital” businesses such as Uber, Amazon, Facebook or Airbnb.

It is easy to understand the phrase “connected car,” and try to envision what that means, in terms of increased computing content.

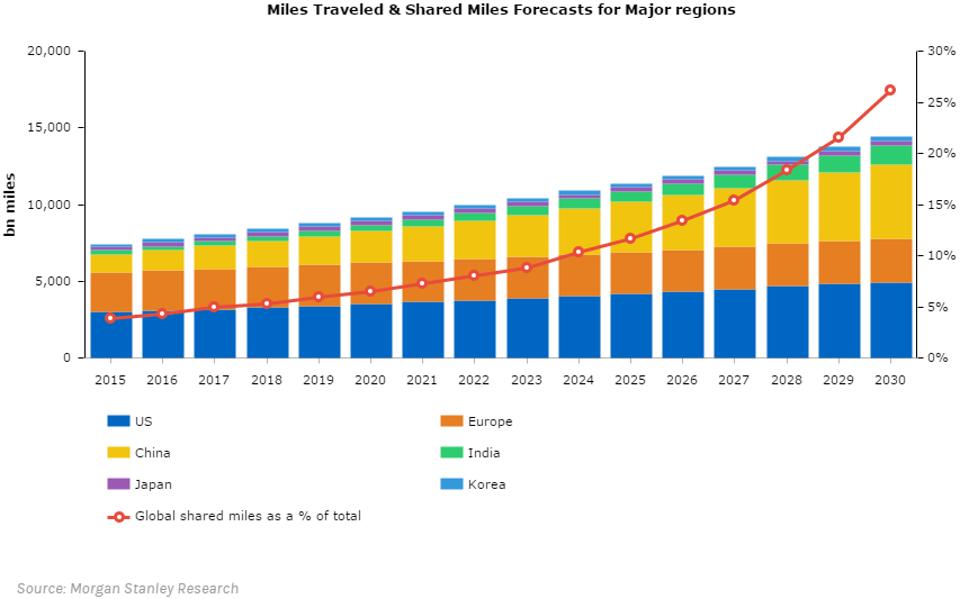

It is quite a bit harder to understand the implications of Moore’s Law for many physical products, or services based on physical products, when there is so much surplus capacity built into the use models. Some estimate that the typical vehicle sits unused 95 percent of the time. That is the inefficiency Uber exploited.

Ability to monetize assets that formerly could not be monetized (spare rooms, spare cottages, spare apartment capacity) was what made Airbnb possible.

Assuming “autos” eventually will cost nearly nothing might make sense if one also assumes “individuals” will not be owning those vehicles. It is a huge leap. It might be wrong. It might not be possible to apply Moore’s Law in such a way to a “physical product” such as an auto.

Traditionally, Moore’s Law has been disruptive mostly to businesses whose “product” is virtual, or can be made virtual (content, transactions). Not to the same extent, but significantly, Moore’s Law has lead to major cost reduction for computing products (all machines that are computational intense).

But the line of reasoning at least suggests ways to think about what one’s business might look like if you make the “wild” assumption (as did Bill Gates and Reed Hastings) that a key input to your business--though prohibitively expensive and underpowered at the moment--eventually will become so affordable that they are not constraints to your planned business.

It might seem crazy to assume that a large physical product such as an automobile could actually become "free." There are lots of caveats, most importantly that the manufacturing of the product will not become "costless."

But the business model? That is where some big leaps could happen.