How much should any tier-one service provider invest in its internet access capabilities?

Much depends on the market dynamics: whether that firm’s role is wholesale-only; wholesale and retail; or retail only or mostly.

But in every case, the fundamentally-sound position is to invest only to the point that an adequate return on capital can be made. The level of return might be dictated wholly, or in part, by a government entity that caps the rate of return. In other markets the rate of return is limited by the amount of competition and risk of stranded assets.

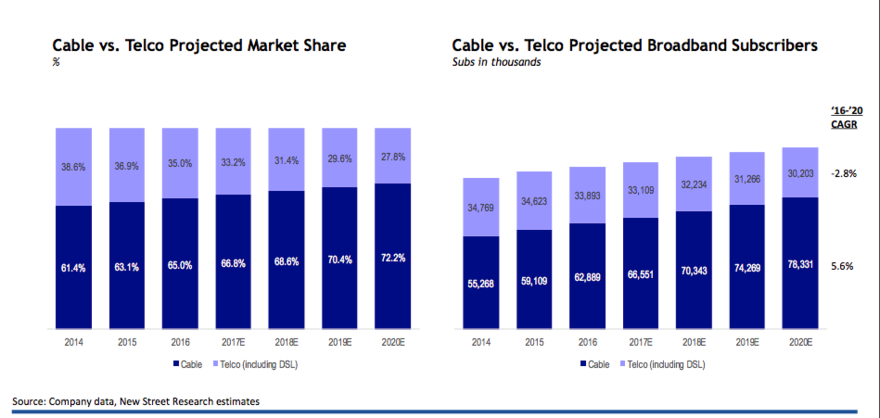

In the U.S. market, some are not optimistic. Jonathan Chaplin, New Street Research equity analyst, believes cable companies could have 72 percent market share in 2020, with as much as 78 percent share of the internet access market.

Some might argue, given such trends, that telcos should simply harvest their internet access customer base. Of course, such forecasts likely include an assumption that telcos must either upgrade to fiber to home or stay with copper access of some sort, and also assume that, for capital availability reasons, the upgrades will occur relatively slowly.

The other assumption is that “telcos” are not the same as “AT&T and Verizon,” which actually are seeing very-modest declines in internet access share, with most of the losses coming from other telcos, especially the large former-rural-carrier ranks (CenturyLink, Windstream, Frontier).

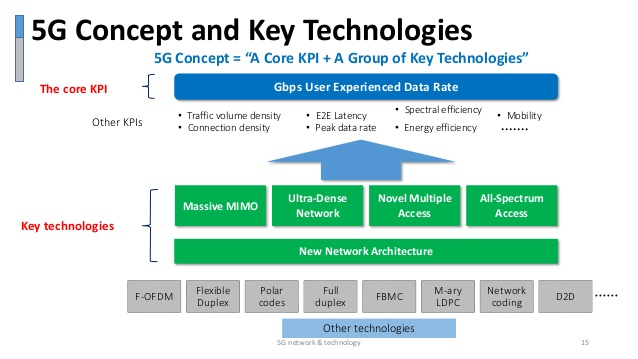

AT&T and Verizon have other options, including both fiber to home, mobile substitution and fixed wireless access options that will improve dramatically with 5G. In fact, in most cases, AT&T and Verizon are likely to find the business case for mobile or fixed wireless much more compelling.

The point is that a service provider has to invest enough in its internet access capabilities to remain competitive in the market, but not more than that level. There are, in some markets, good reasons why the upside is limited.

Consider the U.S. market, where a cable operator is the market share leader, approaching 60 percent share in most instances. That leaves a bit less than 40 percent share for the local telco.

Ignore for the moment the growing cable share, a situation many would argue exists since some key telco providers rely mostly on less-capable digital subscriber line platforms. In the second quarter of 2017, for example, internet access account losses by AT&T and Verizon were infinitesimal (on the level of hundredths of a percent of their installed base).

The logical investment criteria should then be, at a minimum, what is necessary to hold 40 percent market share.

The “maximum” position is a bit less clear, namely the level of investment that could allow either firm to take market share away from competitors. It is not so clear that taking share is possible, no matter what the level of investment, some might argue. Others might argue that this is possible, if mobile and fixed wireless offers can be used to create a superior value proposition, compared to cable.

Ironically, that might be especially true if cable companies start to raise prices as much as double current rates. That would create a higher pricing umbrella underneath which telco offers could operate.

The “take share” position is complicated, as the value proposition includes a range of value (types and quality of services, plus price, plus bundling effects, plus threat of new entrants). The “hold share” position is easier, as it mostly involves offering packages that are roughly competitive with what cable offers, in terms of speed, price, value and role in bundles.

The point is that some telcos might not be able to do much to prevent lost market share. AT&T and Verizon have other options, based on their coming 5G profiles. Even in its FiOS areas, Verizon tends to get only about 40 percent share. Perhaps that is as good as it gets.