Some have argued that 5G fixed wireless is an existential threat to cable TV and some telco fixed network service providers. That might turn out to be mistaken.

But more firms in the internet ecosystem might face similar existential problems in the future, for reasons either of business strategy or government intervention.

By definition, an existential problem is one that threatens the survival of the entity. And that is where strategic decisions matter, as a common rule of thumb is that a firm or entity facing an existential crisis might well have to consider fundamental changes and adaptations. “More of the same,” in other words, does not typically work.

But “more of the same” might be exactly the broad choice most service providers ultimately will make, simply because rival paths are unfeasible.

Some applaud Verizon’s apparent continued focus on the quality of its network and connectivity services, as opposed to other strategies that might reduce reliance on connectivity revenues.

Others think that is risky. Tier-one app, device or platform providers seem to be evaluating, testing entry into the connectivity business on a bigger retail level, or might well do so in the future. The simple reality is that bigger firms acquire smaller firms, and many tier-one platform, app or device firms have market values far in excess of even the largest tier-one telcos, mobile operators and cable operators.

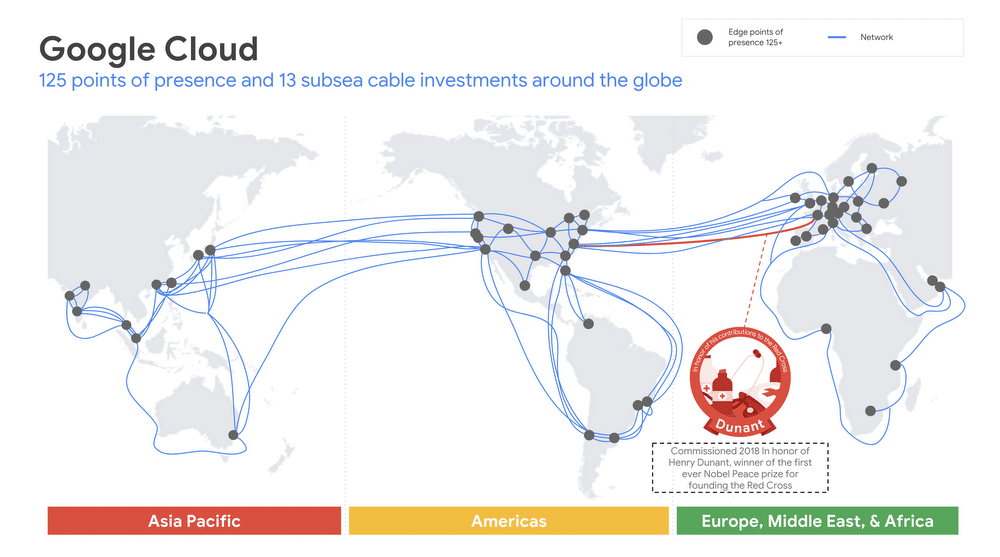

Apple, for example, is the latest to be moving into a potential connectivity role. Google and Facebook already have developed technologies for communications, and Google Fiber of course already is a connectivity services provider.

So the big question is whether most communications service providers should “stick to their knitting” and be the best communications providers possible, or whether sustainability requires moves elsewhere in the ecosystem (“up the stack”).

Both strategies ultimately are likely to be chosen, by different providers with varying abilities to execute on a diversification strategy.

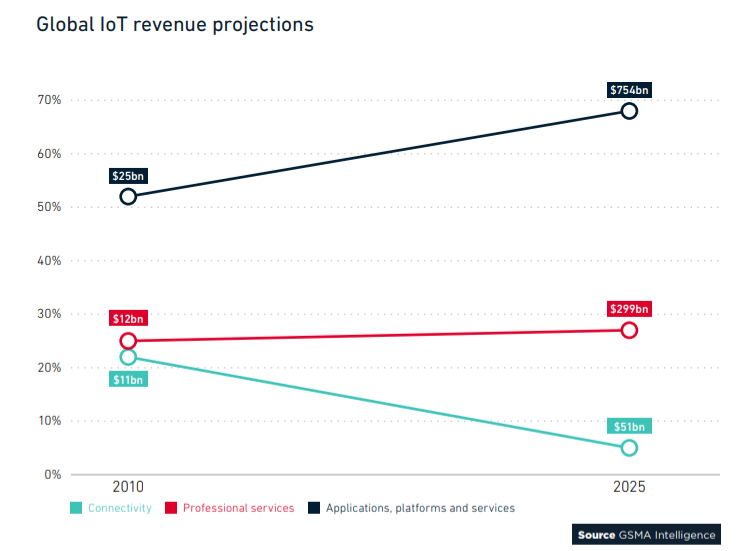

To be sure, in a developing area such as internet of things, connectivity revenue will grow, perhaps substantially. But upside is almost certain to be higher in the applications and platform areas.

Most service providers ultimately are going to choose to focus on connectivity services, even if that eventually means huge consolidation in the service provider space, as surviving firms seek to bulk up, gain scale, boost gross revenues and prop up profit margins.

A relative few will have the resources to diversify revenue sources beyond connectivity (Comcast, AT&T, NTT, SingTel, Orange, DT already are trying). Verizon’s strategy seems to be “focus on connectivity,” after a period where it tried without huge success to create a bigger role in content services.

And we might be premature in suggesting Verizon really believes it can sustain revenue and growth on the strength of connectivity services.

Of course, Verizon and other service providers are not alone in facing what might be existential business problems. Even if it is easier to see that virtually every legacy telecom revenue stream has past its peak, it now looks as though many leading internet app platforms and app provider face their own huge problems, namely of the antitrust sort.