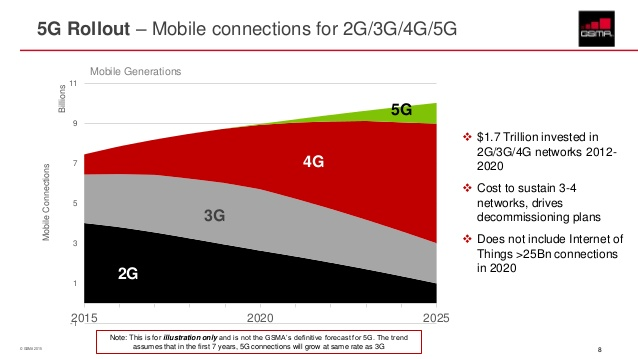

Service provider revenues from 5G connections will approach $300 billion by 2025, rising from $894 million in 2019, a new study from Juniper Research predicts. That also implies a growth rate of about 163 percent over the first six years.

If correct, then 5G service revenues would reach 38 percent of total operator billed revenues by 2025.

It always is difficult, though, to make sense of such forecasts, in large part because revenue earned by the next generation platform tends to displace revenue earned from existing platform. In other words, most 5G revenues will cannibalize 4G accounts.

There should be some incremental revenue upside, if 4G provides a template. In other words, it is likely that new 5G services will be sold at some price premium to 4G. In some cases that will be driven by higher prices for mobile 5G. In other cases, higher revenue will come from fixed 5G, which will be prices comparably with fixed internet access services. That could mean per-account revenue that is higher than mobile accounts generally produce.

In 2025, the 1.5 billion 5G connections will be 14 percent of total cellular connections in the same year, Juniper Research suggests.

Some of us would argue that incremental revenue will be driven by fixed wireless and then internet of things applications. Aggregate 5G revenue figures do not matter as much as the revenue produced by the new services.

For most consumer users, the primary benefit of 5G deployment is going to be that 4G gets more attractive. Very few consumer users will benefit from the ultra-low-latency features of standards-based 5G, and while the headline speeds for mobile 5G will have the same marketing value as gigabit fixed network internet access, virtually no consumer apps require that much speed.

We might find that most consumers are mostly content to rely on advanced 4G for quite some time. If today’s “typical” LTE access speed ranges between 11 Mbps to 14 Mbps, then typical LTE-A might range between 30 Mbps and 40 Mbps.

For any single phone, that is likely to be enough to handle any application a typical person wants to use. So much might depend on what percentage of 5G revenues are driven by new use cases, rather than consumer mobile broadband.