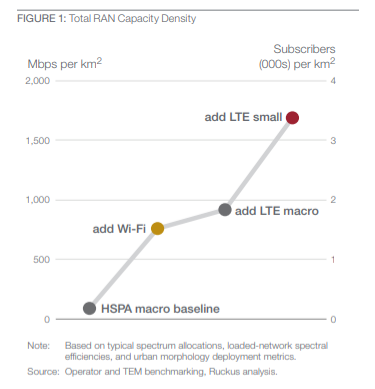

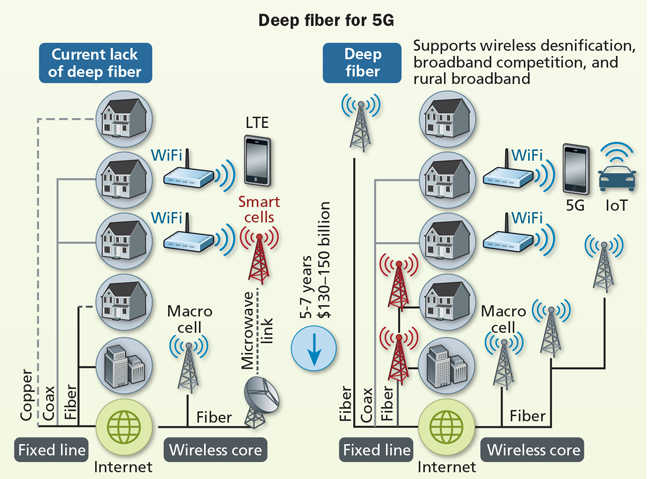

Do industry executives increasingly believe 5G will change the economics of the fixed networks business? This diagram suggests they increasingly believe that is possible. As 5G networks are built, today’s fixed network access (copper, fiber to home or hybrid fiber coax) will be faced with new competition from fixed wireless and mobile wireless alternatives.

That will happen as deep fiber architectures enable use of lower-power microcells and small cells with access to an order of magnitude more spectrum, in addition to better radios and using the frequency reuse principle (cell site division) to historically-dense levels.

By some estimates, 4G has lead to cell tower density of perhaps 2 kilometer (1.25 miles) spacing. Some believe the 5G network using millimeter wave spectrum will require small cells placed about every one-third of a mile. In other words, 5G using millimeter wave spectrum might require about eight times the number of transmitting sites, compared to 4G using towers spaced at about 2 km (1.25 mile distances).

That is probably a high-end forecast, assuming an equally-dense network in all deployment scenarios in dense urban and suburban settings. Virtual nobody believes that is possible in rural areas.

Some might note that such densities, while perhaps common in more-dense urban areas, are not so common in suburban settings, and nonexistent in rural areas, for the most part. Also, the simple assumption here is that optical backhaul to one macrocell in point to point fashion also applies to more-dense networks.

In other words, if one site requires a single point to point connection, then 25 small cell sites require 25 total point-to-point connections. But density itself changes the topology, leading to “more tree and branch off a ring” topology that does require lots more fiber, but not as much as point-to-point links would require.

Still, the business model impact on fixed line network operators will possibly be significant. Think of 5G as a new overbuild operation. Where today a cable operator and telco compete for the consumer internet access customer, tomorrow it could well be the case that those two competitors face a third or maybe even fourth competitor for a market that is very close to saturated.

That means market share losses will happen. The degree of business model disruption then turns on the amount of share the new competitors can take, and from which current suppliers.