Wednesday, April 10, 2019

TVision Home by T-Mobile

T-Mobile US is getting into the linear TV subscription business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

T-Mobile US Launches TVision Home

T-Mobile US has introduced “TVision Home,” its over the top linear video service for fixed network customers, in eight U.S. markets, apparently where its Layer 3 networks already had been available.

T-Mobile US also announced it will launch nationwide streaming services later in 2019, presumably based on use of T-Mobile’s own 5G network as well as an OTT app.

TVision Home 275-plus available channels and over 35,000 on-demand movies and shows. On-screen social content, a personalized home screen and DVR for each user, smart speaker voice control with Amazon Alexa or Google Assistant, and access to security cameras are part of the service.

TVision Home launches with apps for Pandora, iHeartRadio, XUMO, CuriosityStream, Toon Goggles and HSN.

There also is a bit of regulatory arbitrage. Fixed network service providers are required to pay local fees and taxes that TVision Home is not liable for. That allows it to sell a service costing less than cable or telco suppliers.

The implications are clear enough. T-Mobile US is getting into the linear video business, to compete with cable TV operators and telcos. At the same time, it is getting into the live TV streaming business (linear, rather than on-demand), with on-demand video services such as Netflix also accessible as part of the app.

The bigger question is whether 5G mobile TV, in this form, also will begin to show consumer appetite for linear video consumed on mobile devices. Mobile service providers have offered the ability to listen to broadcast radio and TV for decades, but with no real traction. The shift to the full palette of managed video channels is new, though.

Among the questions is how some consumers might start to use the service, casting to TVs, for example.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, April 9, 2019

ISPs are Not the Big Internet Problem

Among the disingenuous arguments raised about network neutrality is that it somehow “saves internet freedom.” It does not. The heart of the network neutrality argument is that internet service providers should be barred from offering any quality of service features for consumer internet access services, on the theory that any other policy would allow ISPs to degrade service on their networks, while creating “value added” services that run faster.

Ignore for the moment that fixed network speeds increased about 38 percent in 2018 alone; that with 5G delivering an order of magnitude faster speeds; with new low earth orbit satellite constellations launching; with new ways to deploy fast fixed wireless access networks; with the number of ISPs actually growing; and that you would be extremely hard pressed to find any actual instances of ISPs deliberately building “crappy” networks that run slow, just so they can try and upsell.

Ignore the coming era of edge computing that will make network responsiveness even higher. Ignore Amazon’s entry into the ISP business; Google’s existing operations and Facebook’s satellite and other ISP operations.

Every public policy has private interest implications. Net neutrality essentially protects Google, Facebook and others from potential underlying cost pressures, even as all major app providers themselves pay to “speed up” their own services, using content delivery networks.

All those firms win when “everybody” has internet access, of good quality and low price. Net neutrality rules are viewed as ways to promote such outcomes. U.S. regulators never have allowed ISPs to block or degrade consumer internet access to all lawful applications, period.

So net neutrality cannot be about preserving consumer access to lawful applications, despite the breathless rhetoric. A fair assessment would be that the danger to consumer welfare comes from the content and application sphere these days: privacy violations; excessive sales of user data; biased filtering policies; selective censorship and so forth. None of those ailments are caused by ISPs.

Internet access keeps getting better, and rapidly. The era of 5G is going to provide extraordinary low latency and quality bandwidth at prices that are low, and dropping, in terms of price per bit and even often in real terms (adjusted both for inflation and different consumer choices).

Internet access keeps getting better, and rapidly. The era of 5G is going to provide extraordinary low latency and quality bandwidth at prices that are low, and dropping, in terms of price per bit and even often in real terms (adjusted both for inflation and different consumer choices).

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, April 8, 2019

IoT Markets are Hard to Quanify with Any Precision

Quantifying the size of edge computing or internet of things markets is difficult, if in fact both have both horizontal capability (general purpose use cases) as well as vertical (within specific industry vertical) implications.

Most firms--even those focusing on IoT--will not likely derive most of their revenue from specific edge or IoT sales. When “everybody” can claim to be, and in fact might be, a participant in the broad ecosystem, it also is nearly impossible to specify the specific value or revenue upside. Virtually all the major cloud suppliers, mobile and fixed connectivity providers, end user appliance and general-purpose computing firms can claim to have some role.

That means virtually every large enterprise software or solution provider, every large ISP, every large computing solutions suppliers, many device and component suppliers and system integrators can claim to have a role.

Security, robotics, connectivity services, chipsets, databases, devices, enterprise software, consulting and implementation services, vertical industry software suppliers, server suppliers, analytics, embedded computing suppliers all would have plausible roles.

Consider just industrial IoT, which might include firms such as DHL, Hitachi, Huawei, SAP, GE, Rolls Royce, Dell, ARM, Bosch, Cisco, AWS, AT&T, Fujitsu, Deutsche Telecom, Telefonica, Google, HPE, IBM, Intel, Microsoft, Oracle, Qualcomm, Salesforce, Samsung, Sierra Wireless and PC-Tel, as well as any firm that competes with these firms.

Siemens, ABB, Honeywell, Schneider Electric, ON Semiconductors, Micron, Broadcom, Analog Devices, NXP, Texas Instruments, Gemalto, RSA, Symantec, Kaspersky, Palo Alto Networks, ThingWorx, Sigfox, Ingenu, Accenture, Fujitsu, Tata, Infosys, Tech Mahindra, Fanuc, Kuka, Boston Dynamics, Zebra and ProGlove also are among firms with possible roles to play.

Verizon, Fortinet, Samsara, Eaton, SonicWall, Johnson Controls, Vertiv and Honeywell are some of the other names any industrial IoT potential participants list would tend to include.

PTC, IGEL, Red Hat, Senet, Cambium, Lenovo, National Instruments, Particle, Rigado, Roambee, Armis, Claroty, Cradlepoint, ForeScout, Trend Micro, VDOO, Xage Security, Zingbox, Falkonry, Foghorn Systems, IoTium, KMC Controls and Seeq might also be names with industrial IoT credibility.

Verizon, Fortinet, Samsara, Eaton, SonicWall, Johnson Controls, Vertiv and Honeywell are some of the other names any industrial IoT potential participants list would tend to include.

PTC, IGEL, Red Hat, Senet, Cambium, Lenovo, National Instruments, Particle, Rigado, Roambee, Armis, Claroty, Cradlepoint, ForeScout, Trend Micro, VDOO, Xage Security, Zingbox, Falkonry, Foghorn Systems, IoTium, KMC Controls and Seeq might also be names with industrial IoT credibility.

But few of those firms will be able to generate specific industrial IoT revenue that moves the needle much on overall firm revenues.

And much the same can be said for potential suppliers in any other vertical market IoT realm. As a general theme, IoT is going to be significant. But specific forecasts will be difficult.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Can 5G Providers Sell QoS?

Can 5G service providers charge a premium for low-latency performance guarantees, when the stated latency parameters--best effort--are already so low? That is a question that also might be asked in other ways.

Will 5G best effort service be good enough, latency-wise and bandwidth, to obviate the need for any additional quality of service features to preserve low latency and bandwidth?

Is there a market for quality of service when delivered bandwidth rates are so high, and latency performance so much better than 4G? In a broader sense, as network performance keeps getting better on both latency and bandwidth dimensions, can connectivity providers actually sell customers on QoS-assured services?

Also, some would argue, it becomes problematic to try and maintain QoS packets are encrypted at the edge. A service provider cannot prioritize what it cannot see. And that is the growing trend as most traffic gets encrypted.

By about 2020, estimates Openwave Mobility, fully 80 percent of all internet traffic will be encrypted. In 2017, more than 70 percent of all traffic is encrypted.

The other change is the emergence of edge computing for latency-sensitive applications. We can assume that the whole point of edge computing is to provide a level of quality assurance that cannot otherwise be obtained.

As content delivery networks provide such assurances to enterprises and content suppliers for a fee, so it is likely that edge computing networks or other networks relying on network slicing to maintain low-latency performance will be sold as a service to enterprises who want that latency protection.

Such deals do not violate network neutrality rules, which do not apply to business services such as content delivery networks. So, ultimately, between encryption, network slicing, edge computing and CDNS, there might actually not be much of a market for consumer services featuring QoS.

Best-effort-only never has been part of the vision for next-generation networks, whatever might have been proposed for the public internet. According to the International Telecommunications Union, “a Next Generation Network (NGN) is a packet-based network able to provide services including Telecommunication Services and able to make use of multiple broadband, QoS-enabled transport technologies and in which service-related functions are independent from underlying transport-related technologies.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

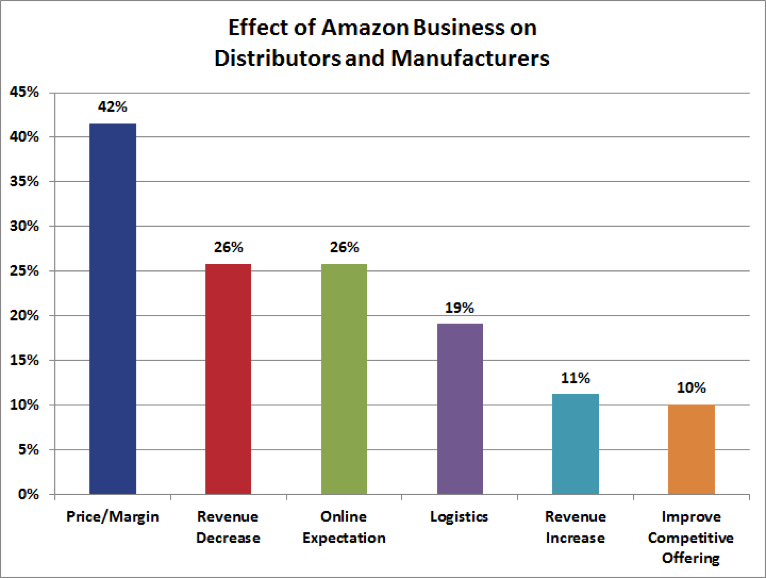

Telecom Industry About to be Amazoned

Question: What happens to any market Amazon enters? Answer: public market valuations drop; market share shifts (or at least people expect that to happen with time).

Rhetorical question: What happens when Amazon enters the telecom business? And it will. Amazon is moving to commercialize its own fleet of nearly 4,000 low earth orbit satellites, to provide internet access to literally every square inch of the earth’s surface.

Amazon wants to be an ISP for the same reason Google and Facebook do, with one major difference: the revenue model. As any ad-supported app provider’s success hinges on the total number of people able to use the apps, so any commerce supplier’s fortunes rest on the number of consumers it can establish direct or indirect relationships with.

And Amazon believes it will do better when more connections can be made directly, without relying on the goodwill of governments or other private firms.

“Four billion new customers” is a big enough carrot to justify launching a constellation of nearly 4,000 low earth orbit satellites, making Amazon one of the world’s potentially biggest internet service provider firms.

It is easy to predict what the implications are for others in the connectivity services ecosystem.

The "Amazon effect" refers to the impact created by the online, e-commerce or digital marketplace on the traditional brick and mortar business model due to the change in shopping patterns, customer expectations and a new competitive landscape. https://www.investopedia.com/terms/a/amazon-effect.asp

Some note that Amazon’s business activities prevent inflation. That’s another way of saying prices cannot rise much.

Surveys tend to show that contestants in any business believe entry by Amazon into their own markets affects gross revenue, profit margins and distribution channels.

To be sure, margin pressure already is a huge issue in the global telecom business for other reasons (competition, changes in end user demand). Amason’s entry into one or more parts of the connectivity value chain will only worsen those pressures.

The big observation is that the telecom industry is about to be “Amazoned.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, April 6, 2019

Will ITU Refarm All C-Band Spectrum for 5G?

Later in 2019, at the World Radio Conference later this year (WRC-19), it is perhaps likely that the entire C-band spectrum presently used by satellite operators will be reallocated for IMT-2000 (5G) purposes.

That is some of the backdrop to current discussions by the satellite, cable TV and other interests, including the Federal Communications Commission, about reallocating up to 500-MHz of spectrum presently allocated for C-band satellite, to 5G, itself a component of the overall 5G FAST plan.

“I believe the best option would be to pursue a proposal put forth by a large, ad hoc coalition of equipment manufacturers, wireless providers, and unlicensed users,” said FCC Commissioner Michael O'Rielly. “They recommend that the FCC allocate spectrum now used for satellite C-Band downlinks (3.7 to 4.2 GHz) for licensed mobile communications and designate 6 GHz spectrum (5.925 to 7.125), which includes the C-Band uplink, for unlicensed use.”

If approved, this approach would free up 1700 megahertz of spectrum, 500 megahertz for licensed and up to 1.2 gigahertz for unlicensed purposes.

Satellite and mobile interests seem always at odds about spectrum allocation, so positions on the latest efforts in C-band will not be foreign.

A report by an advisory committee to the U.S. Secretary of Defense, co-written by vice president of wireless at Google, Milo Medin and tech venture capitalist Gilman Louie makes the point that such a development hinges on use of spectrum sharing, as has been pioneered by Citizens Broadband Radio Service.

The report recommends the “NTIA, FCC and Department of State should advocate the reallocation of the C-band satellite spectrum to IMT-2000 5G use at the World Radio Conference later this year (WRC-19), and take measures to adopt sharing in all 500 MHz of the band in the United States on an accelerated basis for fixed operations.”

A shift of former C-band satellite spectrum in the 4-GHz region might also be more important than some believe, if global 5G supply chains and service providers build product volume in the 3-GHz to 4-GHz frequency ranges.

“In the near term, 3 and 4 GHz spectrum will likely serve as the dominant global bands that drive volume in infrastructure and device deployments,” the authors argue.

And that provides some idea of the importance of how the Federal Communications Commission sets policy for refarming as much as 500 MHz of C-band spectrum in the United States, which is in the crucial band the authors say will be an area of robust supply chain focus.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...