For most consumer mobility apps, 5G represents not so much an experience changer as an experience-maintaining development. While some new use cases will probably depend on both 5G and edge computing, the value of 5G for most consumer smartphone apps is that it allows the network to support ever-increasing data consumption.

For most use cases, 4G latency performance and speeds are likely not a problem. What is a problem is the cost of usage. Consumers are price resistant for all products, but likely especially so for data usage charges. No matter how much data they consume, customers tend to budget only so much for that product.

spending as a percentage of total disposal income does not change much, from year to year. To the extent that increases in purchases have happened, those boosts have been accompanied by decreases in purchase of some other product. To spend more on mobility, consumers have chosen to spend less on fixed network services, for example.

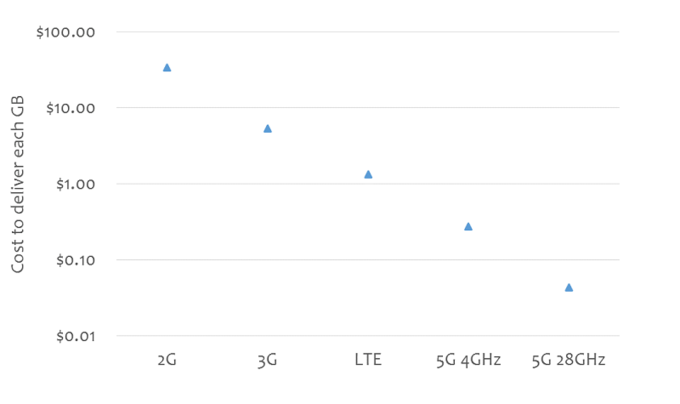

So a linear increase in cost-per-gigabyte consumed is not possible. But that is why 5G is essential: it is a way to keep supplying bandwidth at lower costs per bit, to maintain supplier profit margins.

In some cases, cheaper cost per bit also enables new use cases. That especially is true for fixed wireless use cases, where cost per bit for mobile solutions has to drop by an order of magnitude, compared to fixed alternatives.

Not so long ago, mobile data prices were so high, compared to fixed costs, that full substitution was mostly unthinkable.

That said, the trend is clear: since the 2G era, mobile bandwidth costs have fallen by more than 90 percent. In some markets, while the gap with fixed alternatives remains about an order of magnitude, that could change in the 5G era, especially where fixed wireless is possible.

That is far less true for 5G appeal in the area of enterprise use cases, where very-low-latency, edge computing and ultra-high bandwidth might enable new use cases.

This forecast developed by ABI Research for Interdigital shows as well as anything the potential revenues to be generated by 5G. Note the importance of industrial revenue, compared to consumer revenue.

In this context, “industrial” revenue includes smart cities use cases. “New types of services, especially in cities and smart cities, will likely come faster when 5G becomes a consistent connectivity and processing platform,” say ABI researchers.

“The proliferation of connected cameras and sensors around a city, in combination with 5G connectivity and edge computing, will allow for a much more comprehensive security solution deployed throughout cities,” ABI Research says. “It is almost certain that edge computing will be deployed first in cities, and coupled with 5G, it can allow for smart transport applications.”

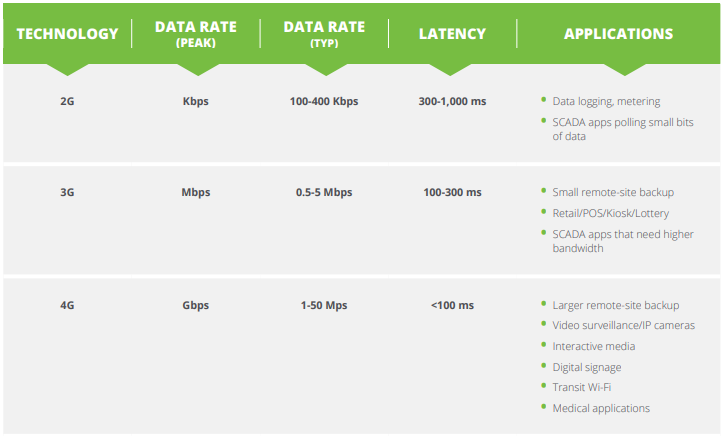

Every mobile generation since the first analog network has enabled new use cases and applications. In business markets, for example, 2G enabled what we now tend to call “internet of things” apps for monitoring industrial processed. During the 3G era use cases expanded to remote site data backups and kiosks. In the 4G era video surveillance became practical.

So the 5G focus on new use cases in the internet of things space are not misplaced. Of course, it is not simply the characteristics of the network but also cost per bit and other terms and conditions of use that help create new use cases.

In the 3G era I would not have considered using the mobile network full time as my primary internet access connection for work. Speed was too low and cost per bit too high. That changed in the 4G era, when I actually did replace a fixed connection with 4G.

To be sure, the use case was not “connect all the users in the home.” That remains to this day a fixed network solution, in large part because the main driver of demand is streaming video. But to support my own work needs, especially given the amount of mobility, 4G was a good choice.

Still, more important shifts tend to take time, at least in part because full deployment and advanced versions of the network will take some time.

But one of the nuances of 5G is that, for most consumer applications, the 4G network is going to be satisfactory, while Advanced 4G (LTE-A) is going to to support nearly every consumer 5G smartphone-based experience requirement.

So advanced 4G is going to be important as a way of maintaining continuity of experience as users bounce between 5G and 4G networks. Nobody wants to experience what used to happen in dropping from an area of 3G to an area of 2G, for example. For some of us, that same experience happened when dropping from 4G back to 3G.

There is reason to hope the switch from 5G to 4G will not be as abrupt, simply because consumer mobile app experience might not be noticeable when speed drops from 100 Mbps to 30 Mbps.

Still, gaming, virtual reality and augmented realitt seem to be the areas where some consumers might find 5G does actually provide improved experience.

For most of us, the transition to 5G will come more slowly, as the need to replace handsets results in acquisition of devices that can use 5G. In other words, for many, the new handset pulls with it the incentive and means to use 5G.

What remains to be seen is how soon that transition occurs, and when new use cases start to emerge. As a consumer smartphone user, the advantage seems less than was the case for migrating from 3G to 4G. Both 4G and advanced 4G seem more than adequate for my needs, at the moment.