“Slow is smooth; smooth is fast,” special operations personnel always say. And that is not a new thought. The Latin phrase festina lente might be translatd as "hurry slowly" or "hasten slowly."

Festina lente suggests that trying to do things too fast often means people and organizations waste time because they go back to correct mistakes. "Haste makes waste," in other words.

In other words, the fastest way of accomplishing something is to work carefully and methodically. It still works. Consider the ways 5G is being built.

You might assume, given all the hype about 5G, and the rival marketing claims, that mobile operators are throwing money at network construction in a mad rush to build out full networks as quickly as possible.

Actually, operators seem to be proceeding rationally, deliberately and at a measured pace, with significant results.

Just a few years ago, projections of 5G infrastructure cost were so high that many argued the networks could not be built. In fact, some speculated that 5G networks would cost 10 times that of 4G. Others only expected 5G costs to double or triple.

Capital investment levels, though, seem not to be skyrocketing, even as 5G is built. In fact, there is growing evidence that 5G can be built within existing capex budgets.

There are several reasons. First, mobile operators are being deliberate in their spending and build rates. Also, capital expense is shifted from 4G to 5G, as always happens when a next-generation network is under construction.

Also, network architects, working with better radios, have found that 5G mid-band signal coverage is almost identical to that of 4G, meaning less physical infrastructure actually turns out to be necessary. Also, low-band spectrum is being used for 5G rollouts, limiting capacity growth, but also requiring fewer new tower or radio sites and backhaul construction.

Better technology, allowing lower cost builds, also is at work.

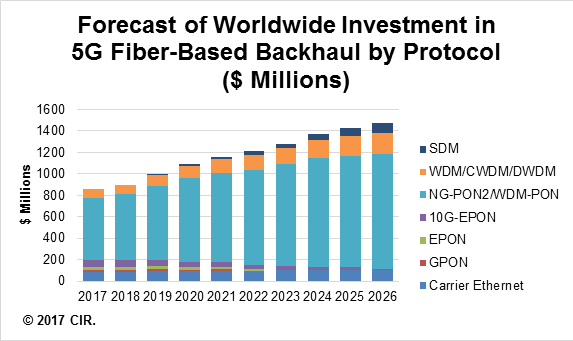

But even at the height of concern, some forecasts suggested reasonable levels of spending on 5G optical fiber backhaul.

So the worst fears about 5G infrastructure cost have not been realized. In substantial part, that is because mobile executives are rational about 5G revenue gains, which will be slight, initially. The business model therefore requires a deliberate approach to investment, all hype aside.

Some might say the early alarm was based to a too-literal extrapolation from past experience with macrocell infrastructure. Analysts basically took the legacy costs and inflated by the expected number of new cell sites. That has proven to be incorrect.

A higher degree of infrastructure reuse has proven possible. Deployment is being carefully phased. Better technology means capex demands are less than expected. Perhaps most important, operators are evaluating investment in light of expected financial returns, and behaving accordingly. -