Some argue U.S. consumers suffer from high prices for internet access. It is a highly-nuanced matter, though. Some issues are methodological. To make a valid price comparison, any researcher has to choose a method--picking plans that are widespread enough to be comparable across many or most nations.

Then one has to adjust prices using some measure of currency conversion that accounts for relative price differences for all manner of goods and services in any particular country. The reason is that general price levels for the same products are higher or lower in different countries, across the board.

Add to that cases where half of all purchases occur in bundles that obscure the “price” of service.

Then there is the matter of value. Price is one thing, while typical speeds and service quality or(outage performance) are different. There is no convenient way to adjust prices to incorporate quality differences (cost per Mbps, for example).

Also, customers in different countries buy different plans. As always, the method of determining “average” matters. Median (half higher, half lower) prices can be quite different from “mean” prices (average of all plans) when plans cover a high range (high to low).

It matters greatly which plans are most-often purchased, in other words. In the U.S. market, 60 percent to 75 percent of internet access plans are bought in a bundle, so there is no way to directly state the internet access price. Price has to be inferred.

To my knowledge, nobody actually uses bundle prices to compare internet access prices across nations. So comparisons are made on the basis of published retail prices for stand-alone internet access. By definition, up to 75 percent of U.S. consumers do not buy internet access that way.

So the price comparisons are made on the basis of retail tariffs alone, without considering the frequency of plan purchase. Under such conditions, all one can say is that published retail tariffs are at certain levels. That tells us nothing about which products customers actually buy, at what volume, and therefore the effective or actual purchase price.

The further nuance is that posted retail prices often are not “final prices” paid by consumers, since taxes, fees, equipment charges and so forth are included. No comparison of retail prices captures the final price.

In the U.S. market, where 60 percent to 75 percent of all purchases are on bundle plans where price cannot be determined, prices are inferred based on allocations. The easy method is to take the total price of the bundle and then divide by the number of services in the bundle to derive an “average” price.

There are obvious methodological issues. Video service tends to be twice as expensive as internet access. And internet access tends to be twice as expensive as voice service. So some method of weighting is required. So the cost pattern is 4:2:1.

Consider a bundle costing $175 a month. The simple “divide total cost by number of services” method gives you a mean cost of $58 a month for each service.

That ignores the retail price differential for each service, however. Retail prices might have a pattern something like $90 for video, $50 for internet access and $30 for voice (after including taxes, fees, customer equipment rentals). So the $175-per-month bundle has video at 53 percent of total cost, internet access at about 29 percent of total cost, and voice at about 18 percent of total cost.

So in a $175 a month package, internet access might cost about $50 a month (including taxes, fees, CPE). That is just an allocation, though. One could argue for a higher or lower price, making different assumptions about the cost of the other components. Video often represents a higher cost, voice arguably a lower cost, in many packages.

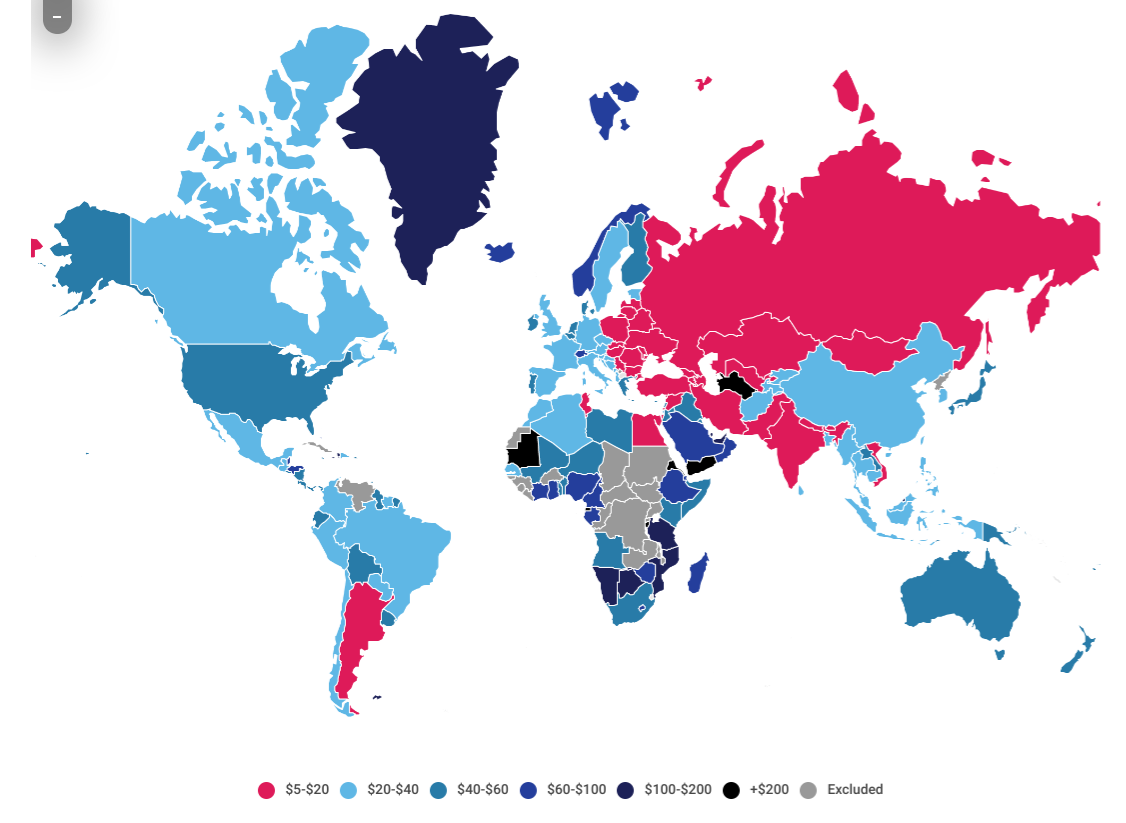

And then one has to adjust for internet access price tiers, since faster service costs more than slower service. This deconstruction of bundle prices actually agrees with the cable.co.uk estimates.

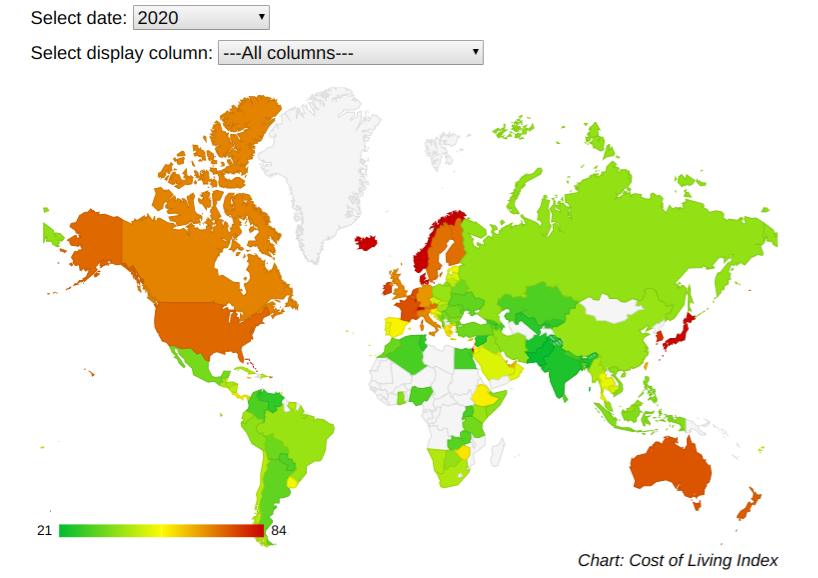

Those prices are not adjusted for price levels in each country, however. So comparisons often adjust for purchasing power parity, normalizing for general price level differences across countries. This look at country cost of living indexes, for example, shows areas in red that have higher living costs generally. So all prices would normally be expected to be higher in those areas. Note that these comparisons are not adjusted for purchasing power parity, though.

One analysis of the costs of fixed network internet access, using the purchasing power parity method, shows that by 2016, internet access prices--adjusted for differences in local prices--actually were quite consistent across nations.

In all countries, prices hovered around a $50 a month level, after PPP adjustments.

The point is that, even if nominal retail posted prices in the U.S. market seem higher than in Western Europe, Japan, South Korea or China, PPP prices in all countries are about the same.