Nvidia CEO Jensen Huang on AI, data science, high performance computing, graphics, edge computing, networking, and autonomous machines.

Tuesday, March 22, 2022

Jensen Huang on AI, Edge, Graphics, High-Performance Computing

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

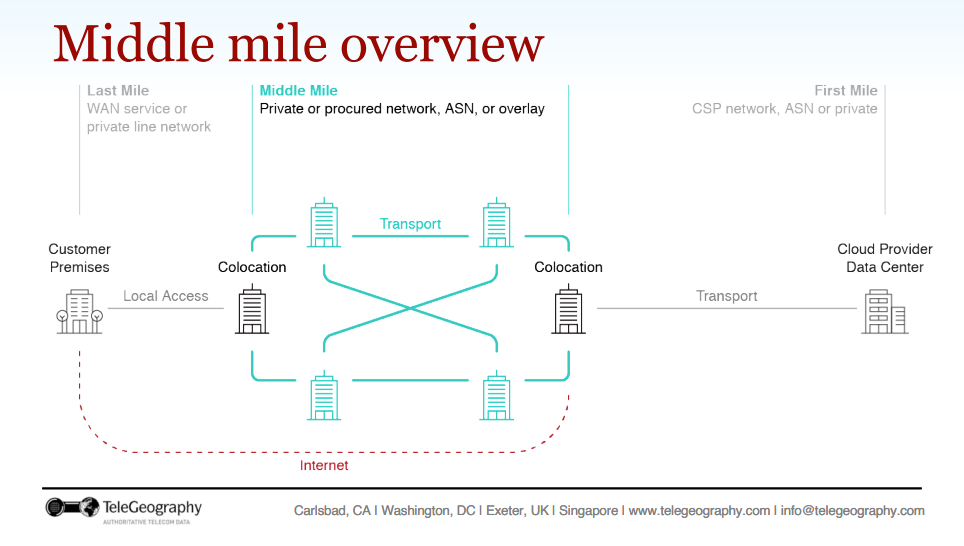

In the Cloud Era, the WAN is Abstracted

If you have been in the connectivity business long enough, you know that terminology changes over time. Our definitions of “broadband” are a moving target. Functions are virtualized, so appliances no longer dictate operations. And networks are evaluated differently by infrastructure suppliers and customers of those networks.

Consider the term middle mile. In traditional parlance, we did not use the term. Traditionally, the portion of the network between Class 4 switches was the wide area network. The part of the network connecting a Class 5 switch with customers was the local access network (local loop). That meant the network connecting Class 5 switches with Class 4 switches was the “distribution” network, which might have been viewed as the “middle mile” between the access and wide area networks.

For internet access providers, “middle mile” means something altogether different, and has less to do with transport function or distance. For an internet service provider, the middle mile is that function moving traffic from an ISP’s own signal processing location (headend, central office, data center) to the nearest internet point of presence.

It is a functional requirement and a cost element that assumes the cloud and wide area networks exist, but abstracts them.

For an ISP or enterprise, “WAN” is an abstraction. Actual costs are determined by the cost of interconnecting at an internet point of presence. Transport is simply a function that is provided by the interconnection cost.

In a retail commerce setting, looking at logistics, “middle mile” means the movement of goods from a supplier warehouse to a retailer location. And that is a fairly good analogy.

From an ISP or enterprise perspective, WAN no longer is a direct cost element, as once was the case for T-1 or DS3 wide area connections. What matters is the cost of connecting the ISP access traffic to the nearest internet point of presence.

As with “cloud” architecture, the WAN is abstracted. What matters is the cost of connecting at an internet point of presence.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, March 21, 2022

When the Data is Wrong, So is the Analysis

Very few issues seemingly are more contentious than the issue of whether internet access prices are high or not; rising or not. Internet service providers do not wish to be accused of price gouging; policymakers do not wish to be accused of not doing enough; some policy advocates must argue there is a problem to be solved, or there is no issue to debate.

Nor is this an easy matter to quantify. If one points out that price inflation has occurred for most of modern history, then of course “prices” will be higher, not lower, over time.

U.S. consumer prices in 2022 are 11.77 times higher than average prices since 1950, according to the Bureau of Labor Statistics consumer price index.

source: U.S. Bureau of Labor Statistics

General U.S. price levels since 1996, when many people started buying internet access, have increased almost fifty percent. So arguing that prices--any prices--have increased over the last decade, several decades or longer does not mean much.

All prices have increased.

The only meaningful issue is whether prices for some products, such as home broadband, have increased more, the same or less than the average for all consumer prices. Nor is that an easy exercise.

Methodology also matters.

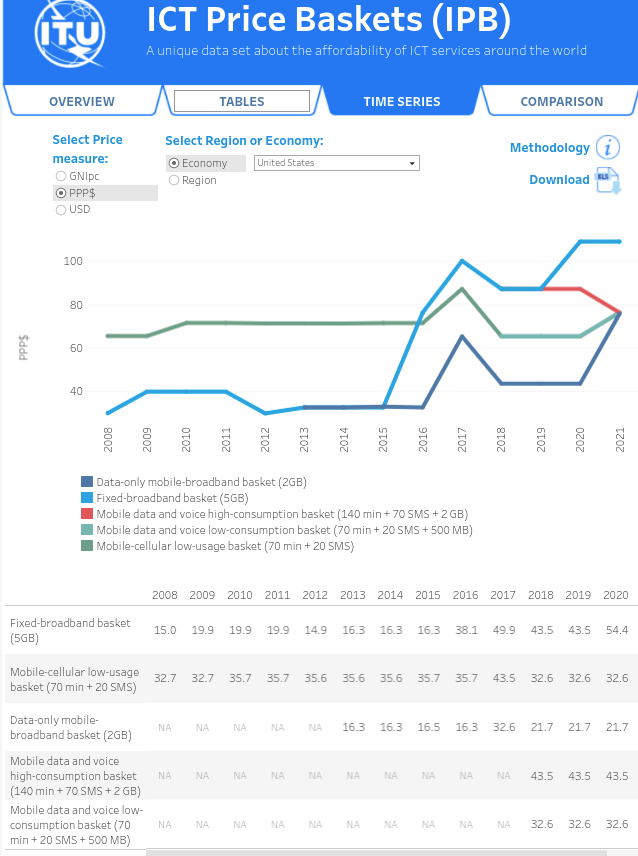

The International Telecommunications Union says that, in the U.S. market, the prices for the lowest-priced plans offering at least 5 Gbytes of usage have increased from less than $40 per month in 2008 to more than $100 a month in 2020.

That seems wildly incorrect. That might be the case for gigabit services--which can approach $100 a month--but cannot be correct for the budget plans that are in the $30 a month level. The methodology is off, as Comcast, the largest U.S. ISP, only charges $30 a month for services operating at 100 Mbps. To be sure, Comcast also says those prices are good only for one year, with sharp price increases after 12 months.

Comcast says its 100-Mbps plan will grow to $81 a month after 12 months. The issue is that it would be hard to find anybody who actually pays that amount for a 100-Mbps service, even after a 12-month period.

The average U.S. home broadband service costs about $64 a month. If the cost of the lowest-priced plan really were more than $100 a month, as the ITU analysis suggests, the “average” U.S. price could not be as low as $64. By definition, the average would have to be much higher.

According to Openvault, only about 20 percent of U.S. households purchased services operating at 100 Mbps or less in the second quarter of 2021 and only 18 percent in the third quarter of 2021 and 17 percent by the fourth quarter of 2021.

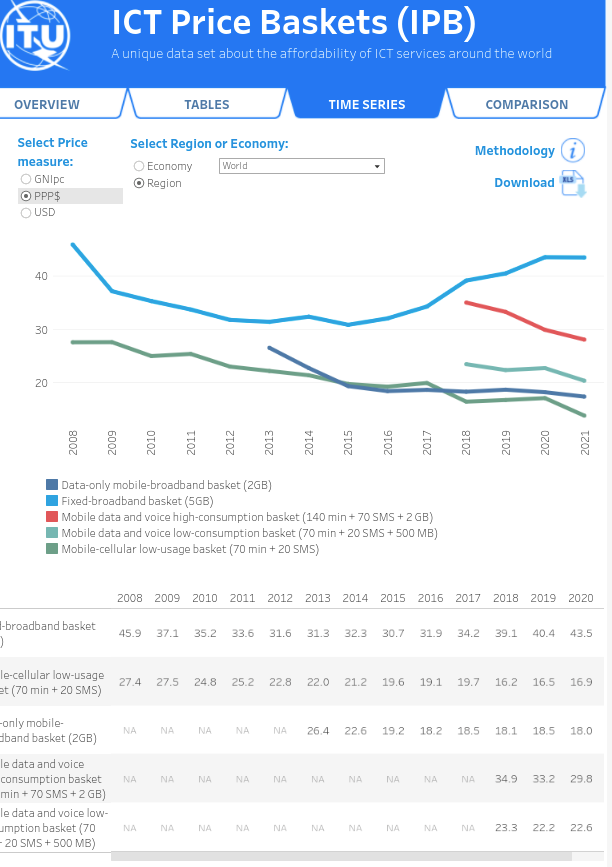

Other issues must be confronted when comparing prices across countries. Adjusting for currency and living cost effects, the International Telecommunications Union, for example, says mobile prices (not adjusted for inflation) have dropped, while fixed network prices for the lowest tier of service have climbed a bit since 2015, but only after having dropped since 2008.

Still, prices are lower than in 2008, all that noted.

Keep in mind that this analysis is only of the cheapest plans in each country offering at least 5 Gbytes of usage and a minimum speed of 256 kbps, supplied by the largest internet service provider in each market.

The analysis is not of the service plans “most consumers buy.” The plans are based only on posted retail tariffs and do not include any discounts customers may have based on promotions or other criteria. Nor does the data take into account whether plans offered by all providers that are not the “biggest” in each market. Nor does the analysis include the prices paid by consumers on the most-popular plans, using any discounts or promotions.

There are other important drivers at work, as well. Since 2008, ISPs in developed countries have been rapidly increasing “typical” speeds, while consumers have been gradually changing the service plans they buy, shifting from lower-speed plans to higher-speed plans that cost more.

Beyond all that, the latest ITU data on U.S. home broadband plans seems wildly incorrect.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Early Metaverse

Metaverse 35,600 years ago!

source: Pinterest

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Ecosystem Adjacencies are Valuable But Debt-Inducing for Telcos

Verizon’s collaboration to develop a 5G, smartphone-based immerse game Helios, and Microsoft’s acquisition of Activision Blizzard illustrate the issues connectivity providers face in creating new value and revenue.

In part, Verizon believes 5G and a robust edge computing platform will encourage partners, users and customers to prefer its network. Microsoft, for its part, becomes the owner of the third-largest gaming planet globally.

Verizon will spend a bit to demonstrate the value of its network, though the financial upside will be nearly impossible to measure. Microsoft spent $69 billion to own an asset producing nearly $9 billion in annual revenues.

The financial upside for Verizon is more likely to be measured in net account additions, churn reduction or average revenue per account than emergence as an equity owner of gaming assets.

In fact, Verizon is likely to earn measurable revenue from fixed wireless than it will from advanced gaming. Fixed wireless revenue already is measurable, in fact.

On the other hand, “metaverse,” now touted by Verizon as a growth opportunity, seems likely to produce revenue value--in consumer or business segments--mostly indirectly.

Verizon is unlikely to be a major asset owner of metaverse properties. Verizon is more likely to create value as a connectivity or edge computing partner for firms that do own metaverse apps and services, with some direct but mostly indirect revenue upside.

In other words, metaverse is important mostly as it affects account acquisition, account retention or average revenue per account in its consumer mobility business, or as a supplier of edge computing real estate services for companies that offer metaverse platforms, gaming services and apps.

All of that, in turn, illustrates the difficulty of adding new roles, beyond connectivity, to grow revenue. Both Verizon and AT&T have had recent experience amassing content assets, for example, at the cost of high debt burdens. And both have unwound those strategies in large part to reduce leverage.

Domain expertise is an issue, but probably not as great an issue as the sheer amount of debt a telco has to incur in order to acquire a significant position in any adjacent ecosystem role.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will Telco Revenue Mix Really Change Substantially Because of 5G or IoT?

Historically, business customers have generated somewhere between 20 percent and 40 percent of total connectivity provider revenues. In most markets, the percentage is likely to be closer to 20 percent than 40 percent.

When one hears observers speculating about 5G revenue growth, business or enterprise revenues always loom large. What is less clear is the meaning of that observation.

It might mean that new use cases develop mostly in the enterprise segment, but that total revenue remains generated by the consumer segment. It could mean the historic mix of revenues changes, and that business revenue becomes a larger percentage of total.

Globally, revenue amounts and growth are led by mobility services, and most of that is earned from consumers rather than businesses. But one constantly hears the argument that 5G is going to be different, because of the internet of things, edge computing or private networks.

Just how different is the issue.

It never is completely clear whether 5G produces, or can produce, enterprise revenues fast enough to change the historic share of revenue in fixed or mobile segments of the business.

It is easy enough to find projections of total mobile connections that suggest sensors will outnumber phone users by quite a wide margin. But connections are not directly related to revenue on a one-for-one basis, as IoT connections generate revenue an order of magnitude or sometimes two orders of magnitude less than phone accounts.

Also, many IoT connections will not directly use new wide area networks for access. Instead, local area connections of various types might actually predominate. Ericsson, for example, has estimated that about 15 percent of IoT devices will use mobile networks for connectivity.

In fact, that seems relatively unlikely, Rather, the emphasis on enterprise revenues typically refers to incremental growth. Some estimate business revenues represent only about 25 percent of total revenues. In some markets business revenue might reach close to 40 percent.

For a decade or so, service providers also have been urged to consider a range of changes in their operations, from separating retail and network functions to simplifying retail offers. Rarely is specific strategic advice given to emphasize business customer connectivity revenue over consumer revenue sources.

Service providers are, of course, encouraged to explore new roles and revenues in internet of things, private networks or edge computing, all of which might fall under the “explore market adjacencies” objective.

It seems unlikely to me that new business segment revenues are going to be substantial enough to fundamentally change revenue dynamics that have most of the total revenue being generated by consumers using phones.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, March 20, 2022

Home Broadband Payback Model Changes Radically When One Subsidizes 75% of the Cost

This is one example of how the business case for fiber to the home and other advanced home broadband networks is changing. Delaware has allocated $110 million to improve home broadband access in unserved and underserved areas, using federal government funds.

The cost of construction will be reduced by about 75 percent for 11,000 locations said to have no fixed networks providing home broadband access. Those locations likely map close to the 11,800 unserved Delaware locations previously identified.

Comcast won a grant of more than $30 million; Verizon received $11.8 million and Mediacom got $11.1 million.

For Verizon, the grants mean 940 Mbps home broadband will be made available to 3,000 unserved locations” in Delaware. That implies a subsidy of about $3933 per new line, with Verizon contributing $1311 per line.

That implies a total cost per new Verizon line of about $5244.

The awards also imply that 75 percent of the cost per line for the cable companies is about $2275. Assuming Comcast and Mediacom contribute 25 percent of the construction cost, the total cable cost per line is about $3033.

Network cost is one key element of the payback model; consumer willingness to buy is the other key variable. Consumer willingness to pay is highest at $50 per month and drops off steadily at higher levels.

One might infer that at about $100 a month, half the market will not buy. Many studies suggest the U.S. home broadband median monthly price paid is about $60 to $65 or $68 a month.

Some studies show cable connections are the most affordable, satellite connections the most expensive. Inflation-adjusted prices are lower than $60 per month, some suggest. Analyses can vary based on whether they include additional charges or whether the monthly recurring price reported by a consumer includes those charges.

Estimates also can vary based on how the analysis is conducted. Comparing posted retail prices is one way; estimating actual prices, including all discount mechanisms, is another way. And some studies weight the results by considering the plans consumers actually buy.

The key takeaway is that subsidizing 75 percent of the cost of facilities radically changes the payback model for home broadband.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

Uh Oh: Big AI Circular Deals

So now we have a new wrinkle to add to the “potential AI bubble” thesis: circular deals between AI infra suppliers (chips and compute platfo...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...