One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infrastructure investments than customer demand. Beyond that, MEC almost necessarily involves some sharing of revenue among ecosystem participants.

To determine whether the connectivity provider business model for MEC actually works, one has to delineate cost (capital investment as well as operating costs) as well as revenue. And some of us still do not clearly see how the business plan works out, at least where it comes to retail revenue.

It is a bit easier to envision how edge computing works as a necessary part of the network infrastructure to support advanced mobile networks, which are, by definition these days, distributed. In other words, MEC might be just as important as telco operating infrastructure as a possible source of retail revenue from customers.

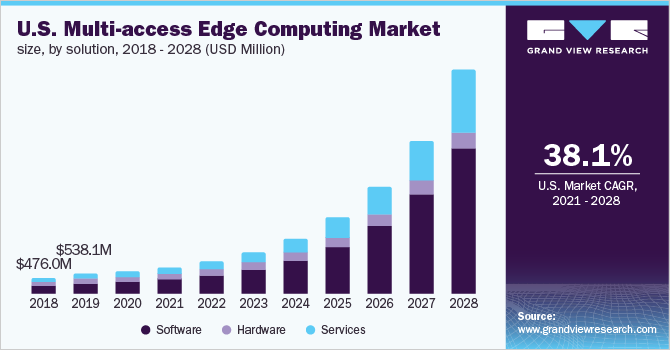

Research and Markets has forecast 2028 MEC revenue at about $23 billion. That mostly includes infrastructure sold by hardware and software suppliers to create MEC capabilities.

Service revenue from actual “edge computing” is included, but one still must make assumptions about the receipt of such revenue by ecosystem partners, such as a hyperscale computing as a service supplier and its access network partners.

But one matter is clear enough: most “MEC” revenue is generated by the sale of hardware and software to create the capability, not revenues earned by the supplier of the actual “computing” service.

It matters greatly “who” is supplying the edge computing “as a service” and who is providing other necessary infrastructure. It also matters “what” is defined as “edge computing revenue and services.” In addition to the “as a service” revenue, there are recurring revenue contributions from real estate (colocation) and connectivity.

Right now, it is nearly impossible to accurately predict the magnitude of “edge computing” revenues. How does Amazon Web Services state revenue for a customer account that uses both cloud and edge resources, for example?

Does a mobile operator report additional connectivity revenue supporting internet of things use cases as “connectivity” revenue in its business customer segment, or as “edge computing” revenues?

Looking only at private networks, there are similar issues. How do we separate “edge” from other “computing infrastructure” spending? As always, attributions matter. What is “private edge;”what is use of “public edge?”

It is far easier--if not “easy”--to estimate what it might cost to create MEC capabilities.

Private network multi-access edge computing investments will amount to about $6 billion by 2030, ABI Research now estimates.

Juniper Research predicts that annual investments by telecommunications operators on multi-access edge computing infrastructure will reach $11.6 billion in 2027, up from $5.4 billion in 2022; a CAGR of 16.7 percent.

Total “spending” on MEC facilities will be higher. Juniper Research estimates investment of nearly $9 billion in 2022 growing to nearly $23 billion in 2027.

By 2027 mobile operators will have built out more than 3.4 million MEC nodes, up from less than one million by the end of 2022.

Juniper forecasts that over 1.6 billion mobile users will have access to services underpinned by MEC nodes by 2027, up from only 390 million in 2022.

Of course, that is a prediction about capital investment, not revenue. And revenue also is a complicated matter where it comes to edge computing. Edge computing spending can represent purchases of user or network devices; software capabilities or computing as a service or 5G access to support edge computing.

So revenue can accrue to a number of participants in the edge computing ecosystem: device retailers, network infrastructure providers, software suppliers or connectivity service providers. So when researchers talk about MEC revenue or investments, one has to separate shares within the ecosystem.

Some estimates have total MEC revenues exceeding $25 billion by perhaps 2027 and close to $70 billion by 2032. Other estimates suggest annual revenue of close to $17 billion by 2027.

But those forecasts virtually always lump together revenues earned by hardware, software and services suppliers: infrastructure and platform plus computing as a service revenues. And computing as a service revenues will likely be dominated by hyperscalers, not mobile operators.

Connectivity providers will profit from real estate support and some increase in connectivity revenues, but relatively rarely from the actual “edge computing as a service” revenues.

For example, assume 2021 MEC revenues of $1.6 billion globally; a cumulative average growth rate of 33 percent per year; services share of 30 percent; telco share of service revenue at 10 percent.

The actual MEC revenue from MEC is quite small by 2028. In fact, too small to measure. Of course, all forecasts are about assumptions.

One can assume higher or lower growth rates; different amounts of connectivity provider participation in the services business; different telco shares of the actual “computing as a service” revenue stream; greater or lesser contributions from mobile connectivity revenue from MEC.

The point is that actual MEC revenues earned by mobile operators or other connectivity providers might actually be quite low. So value earned from all those infrastructure investments would have to come in other ways.

Higher subscription rates; higher profit margins; lower churn; higher average revenue per account are some of the ways MEC could provide a return on invested capital. Some service providers might actually provide the “computing as a service” function as well, in which case MEC revenues could be two to three times higher.

But many observers are likely to be disappointed by the actual direct revenue MEC creates for a connectivity provider.

So revenue can accrue to a number of participants in the edge computing ecosystem: device retailers, network infrastructure providers, software suppliers or connectivity service providers. So when researchers talk about MEC revenue or investments, one has to separate shares within the ecosystem.