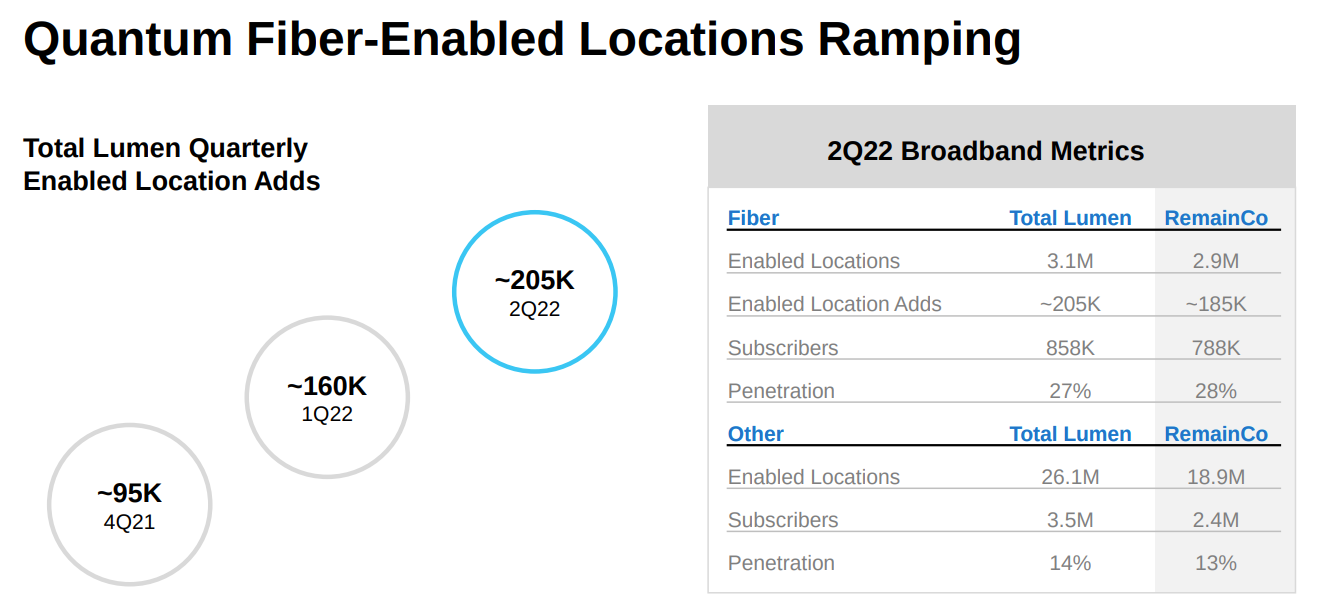

Lumen Technologies is expanding its fiber to home expansion activity, expecting to boost the availability of fiber-to-premises beyond the 27 percent of homes it already supports. With the caveat that Lumen’s future success rests more with its enterprise portfolio than its consumer broadband business (all mass markets revenue is about 25 percent of total), the fiber upgrades should boost subscription rates.

Where the fiber access network gets about 27 percent adoption, the copper access network gets about 14 percent take rates. In other words, FTTH gets almost double the adoption of the copper access product, with FTTH average revenue per account of about $59 a month.

In principle, Lumen should be able to gain a price advantage over its key cable TV competitors, at least if most customers on all the networks buy the advertised products at the advertised prices (ignoring promotional or bundle pricing). Whether that is the case in practice is far from clear.

Nor is it always completely clear that 5G and 4G mobile networks are outclassed to the point that they cannot gain significant market share. The early evidence suggests that a significant portion of the consumer market is content with lower-speed service (up to 200 Mbps), and will buy a fixed wireless service. That value segment could represent about 33 percent of the present market.

As always, that value segment will be offered higher speeds over time, for about the same price (less than $50 a month).

Some of us would argue that the real advantage over cable will lie in symmetrical broadband features, not price per bit or downstream speed.

The issue is how fast cable companies will move to boost upstream speeds; how fast Lumen can upgrade its home broadband access facilities and how fast both Lumen and the cable firms can boost downstream speeds.

Of these three, the first two are likely going to be crucial, as the salient performance advantage Lumen will be able to claim, once facilities are upgraded to fiber, is upstream speed. Lumen believes it will be able to build the network for $1,000 per passing or less, with incremental capital required to activate each customer location.

The issue then will become the penetration rate (customer adoption rate): can Lumen relatively quickly boost its customer share from 27 percent up closer to 40 percent? Possibly equally important, can Lumen get a higher share of the performance-oriented segment of the market, willing to pay more?

Much could hinge on whether Lumen can hit its own goal of upgrading to a total of about 12 million FTTH locations over the next six years, at the expected capital investment cost, at the expected take rate.