Startups have advantages and disadvantages that well-established legacy firms do not face. No internet service provider, mobile operator, cable TV provider or video streaming firm has to convince buyers there is a problem that firms in the category can solve.

Hilton, Marriot and Hyatt do not have to explain to buyers what they do. Airbnb had to convince people. So did Uber. So did Google (with search). That is called category creation.

Category creation often is a task that firms in emerging new markets must cultivate, to raise money, create valuation expectations, attract business partners and customers.

The concept is that some big new class of problem is solved by a new category of solution providers. Solving a different problem, with a different solution is foundational.

Think about HubSpot, IKEA, Pixar, Netflix, Google, Airbnb or Uber.

That often also means solving a problem buyers did not know they have.

“It's difficult to create a category without inspiring others and getting them to realize they had a problem they didn't know existed or that fundamentally changes how they interact with the world,” argues Michelle Snyder, digital investor, has said.

In that regard, a category of one creates buyer risk. It actually is helpful, when creating a new category, to have competitors in the same category.

“From the start, you must base your efforts on some broader market, consumer, or societal change that you believe will fundamentally change how we should look at the world,” says Sapphire Ventures. “Providing that macro context elevates the conversation beyond a product pitch from your company, and helps create a sense of inevitability for your vision.”

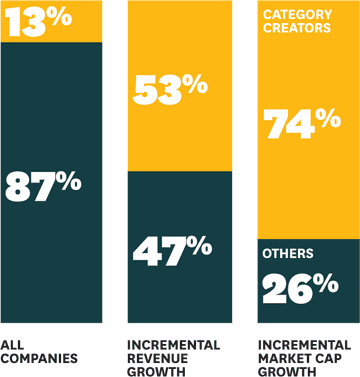

Firms in new categories often are valued at richer multiples than firms in legacy categories. They also can grow revenues faster than firms in related older categories and definitely reap rewards in terms of equity valuation.

“Category creators are a small part of the Fortune 100 list of fastest-growing companies—but they account for much of the group’s growth,” say Eddie Yoon, principal of the advisory firm of Eddie Would Grow, and Linda Deeken, founder of Deeken Strategies.

source: Harvard Busienss Review

In many cases, startups are virtually required to create a new category. “In Silicon Valley, creating a new exciting category is the holy grail of what most companies are trying to achieve,” says Al Campa, Rocket Scale CEO.

Building a business when customers and ecosystem par;ticipants already understand the problem to be solved is one matter. But building a category is different. By definition, the new category falls outside existing understanding. That understanding has to be created.

Clearly-understood new categories also reduce buyer risk. “There are always a few consumers who want to be the first among their friends to try a new product, but this is a surprisingly rare behavior,” says Peter Thomson, a digital strategist.

Most buyers, though, are very risk averse.

As a practical matter, that often requires bringing together thought leaders, practitioners and competitors together. In part, the reason is simple: market participants must be convinced there is a big new problem the category solves. Think of the aphorism “a rising tide lifts all boats.”

Think of the practical marketplace value of any industry consortia, forum or association that works to promote the value of any particular industry segment. By framing a big problem in an innovative way, the whole category is boosted.

That is particularly true when markets must be convinced a big new problem exists that has an important new solution.

“Category creation becomes a self-fulfilling prophecy,” Sapphire Ventures notes. “When you’re able to both identify the disease and deliver the cure, it creates a defensible moat around your business.”

“The intermediate goal for creating a new category is starting a conversation in the market that includes you,” Sapphire says.

How many firms in the data center, Wi-Fi, wide area or local access connectivity or mobile businesses can you think of that ever created a new category, in the same sense as Uber, Airbnb, Google (search), Amazon (retailing) or Meta (social networking).