Lower prices are a policy feature, not a bug. Government policy promoting competiton is designed to create lower retail prices. So it should not be surprising that pressure on average prices per user or customer or account now are a major service provider concern.

What else would you have expected? Lower prices are the intended outcome of competition policy.

To what extent is it correct to characterize legacy service provider revenue trends as “down and to the right?” Obviously legacy services such as fixed network voice, mobile messaging and voice and linear entertainment video generally show that pattern.

What we often forget is that the very objective of introducing competition for connectivity services, and the government policies to support that objective, are intentionally designed to create lower prices. The objective of policy is a “down and to the right” pattern.

In other words, “down and to the right” is not a bug, it is a feature. It represents the outcome policy intends, and is not a defect of policy.

The other angle is that a proven way of increasing ARPU is to increase speed, despite another clear trend: over time, speeds grow but prices remain relatively flat, or even decline. In other words, the cost of a 300-Mbps connection is the same, or less, than a 512-kbps connection three decades ago.

Over the short period of 2007 to 2017, for example, U.S. typical speeds grew by two orders of magnitude, while prices dropped.

At the moment, up to 80 percent of U.S. locations can buy internet access operating at least the gigabit per second level.

The global pattern is not always transparent. If one looks only at total service provider revenue, that tends to grow each year, in large part because new customers are added in growing regions (Asia, primarily, but also eventually in Africa).

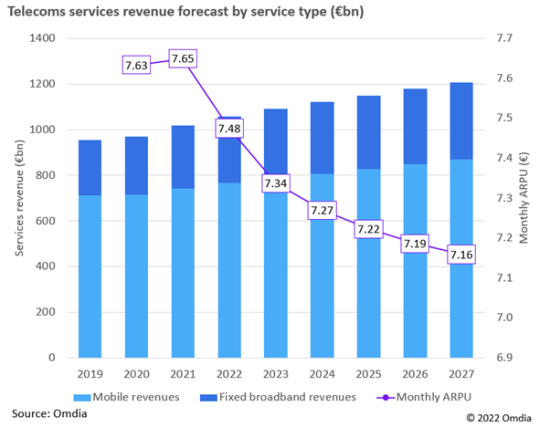

So global service provider revenues will grow 14 percent between 2022 and 2027, according to researchers at Omdia. Monthly average revenue per user will fall by four percent. So the pattern is more customers, each paying less than the “typical customer” used to pay. Revenue might ber “up and to the right” but ARPU clearly is “down and to the right.”

Every management team seems to emphasize that value can be enhanced, preventing further commoditization. You can make your own assessment of how effective such efforts have been, or could be.

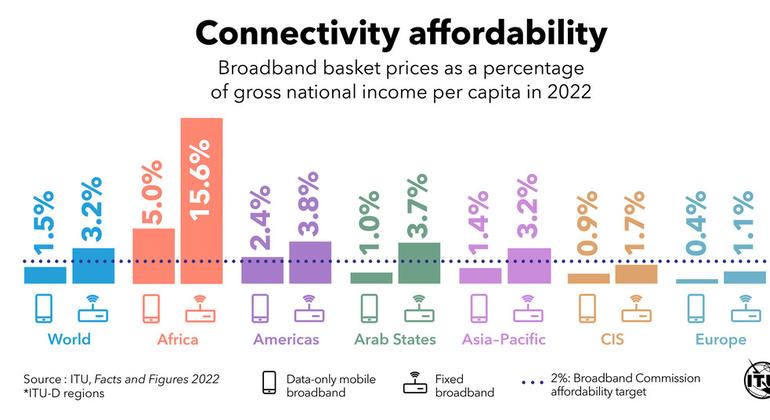

Disposable income is among the other limitations. It will be hard to boost ARPU very much in lower-income countries. If policymakers succeed in reducing the cost of connectivity to perhaps two percent of gross national income per capita, that further limits ARPU upside.

source: S&P Global Market Intelligence

In other words, the goal of policy in developing countries is to actively reduce ARPU. The objective is precisely “down and to the right” pricing.

Until recently, home broadband was the major product line producing “up and the right” results, but growth now has slowed in mature markets. That pattern looks more like “flat and to the right.”

When service provider executives talk about a transition from “telco to techco” they essentially are saying such moves will change the revenue picture to “up and to the right.”

Service providers in emerging or younger markets have advantages, in that regard. They can still hope to rely on mobile subscription growth and uptake of mobile internet access to fuel their continued “up and to the right” growth prospects.

Mature market executives who own infrastructure assets have no such luxury, and strategic options often hinge on whether mobility revenues exist. Contestants in mobile or fixed businesses who operate using wholesale access, rather than owning infra, have other options.

Competitors with Infra-based business models complain about higher capital investment requirements and limited abilities to monetize those investments, not without basis in fact.

Still, we often forget that the whole point of introducing competition in access markets is to drive average costs “down and to the right.” It is a policy feature, not a bug.