As much as connectivity providers envy the valuation multiples earned by app providers, so long as data access and transport remains a distinct part of the value chain and ecosystem, it is going to command a valuation set by the market.

For example, mobile operators have an EV/EBITDA multiple of about 8.7, according to an analysis by NYU’s Stern School of ratios in January 2023. That is close to the cable TV multiple of about seven. Telecom ratios are a bit below six. Internet software earns a multiple close to 15.

As always, firms are evaluated differently even within the same industry. A recent analysis suggests that small ISPs that also are cable operators get a higher multiple than the largest and larger service providers.

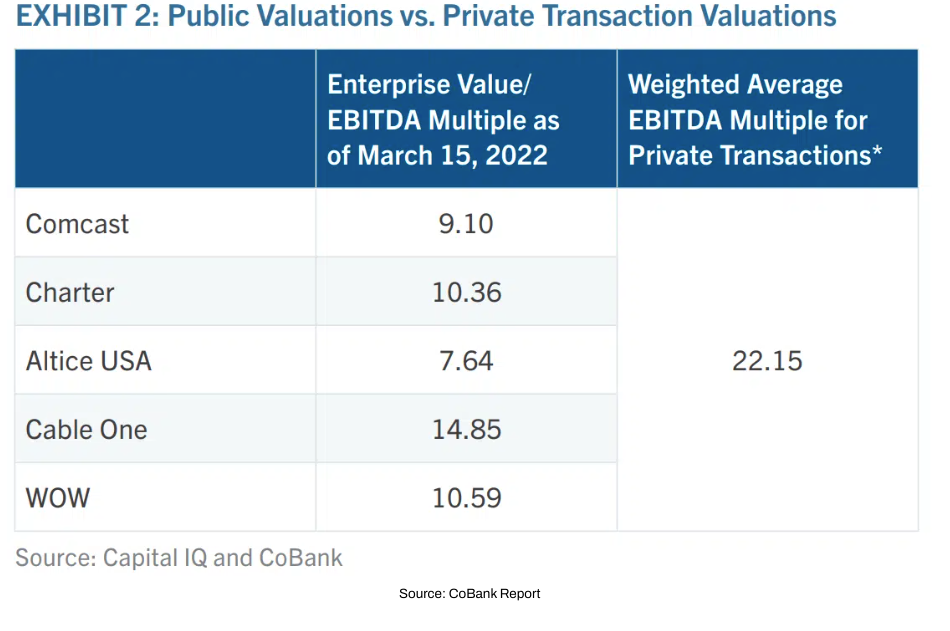

source: Cobank, CapitalIQ, Telecompetitor

According to Equidam, telecom services and mobile service have EV/EBITDA ratios of nearly seven. Online services have a multiple of nearly 16. In other words, online services are valued at more than twice that of integrated telecom providers.

Likewise, Equidam estimates telecom EV/EBITA at a multiple of 6.4, while information technology carries a 16 multiple. Other analyses by McKinsey suggest a telecom service provider EV/EBITDA median ratio around 10 and a median information technology radio a bit over 15.

Since “telecom” often is lumped in with “telecom, technology and media” as a category, the aggregate indices often obscure more than they reveal. “Worldwide, the average value of enterprise value to earnings before interest, tax, depreciation and amortization (EV/EBITDA) in the technology and telecommunications sector as of 2022 was a multiple of approximately 20.8 times,” says Statista. But the “software (internet) industry saw the highest valuation multiples with 44.9 times.” So the “telecommunications” ratios were far lower.

According to Siblis Research, the EV/EBITDA ratio for “communications” firms in the large capitalization category was about 8.6, while the ratio for “information technology” was about 16.

To be sure, valuation metrics change over time, and specific valuations of any particular firm, at any particular time, geography, revenue magnitude and strategic value, can vary.

But you get the point: different industries are evaluated differently in financial markets.

The complication comes when firms in different industries start to “converge,” offering services and products historically offered by other industries. When revenue magnitudes are low, it is likely that a unit of revenue earned by a firm in a high EV/EBITDA industry is valued at that industry’s norms.

The same unit of revenue earned by a firm in lower EV/EBITDA industry then is valued at that industry’s norms. At low revenue magnitudes, that makes sense. But when revenue contribution grows in significance, creating a business model that is similar to a conglomerate, then a “sum of the parts”. analysis might be helpful.

Looking at products rather than industries. If a certain product has a valuation multiple of X, that product should nearly always be valued at the X multiple, no matter what firm in which industry segment earns that unit of revenue.

source: Corporate Finance Institute

That sort of process is highly useful for evaluating firms such as Amazon, which is a mixture of e-commerce and computing-as-a-service segments, each with distinct growth profiles and valuation metrics. Sum of the parts historically also has been useful when evaluating conglomerates that operate in multiple lines of business.

Increasingly, with virtualization, that is going to apply to firms in the cloud computing, data center and connectivity businesses as each segment begins to earn revenue in different “industries.”