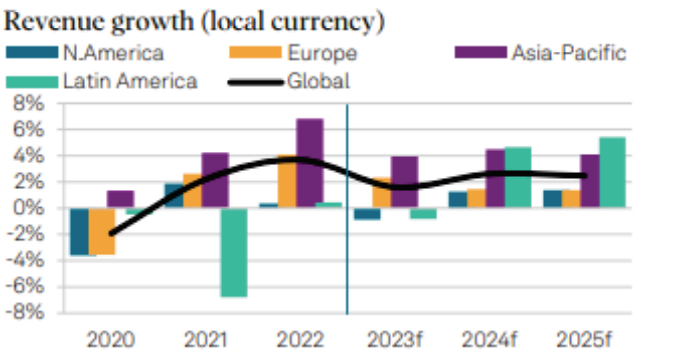

Connectivity provider revenue growth between 2024 and 2025 should be about as most would expect, with a global average of about three percent per year, with slower growth possibly in the one-percent range in North America and Europe, with higher growth in the four percent to 4.5 percent range in Asia-Pacific and Latin America, according to S&P Global Ratings.

To be sure, executives might wish for faster growth rates, but growth rates in mature markets, especially in industries with “utility-type” characteristics, often are slow.

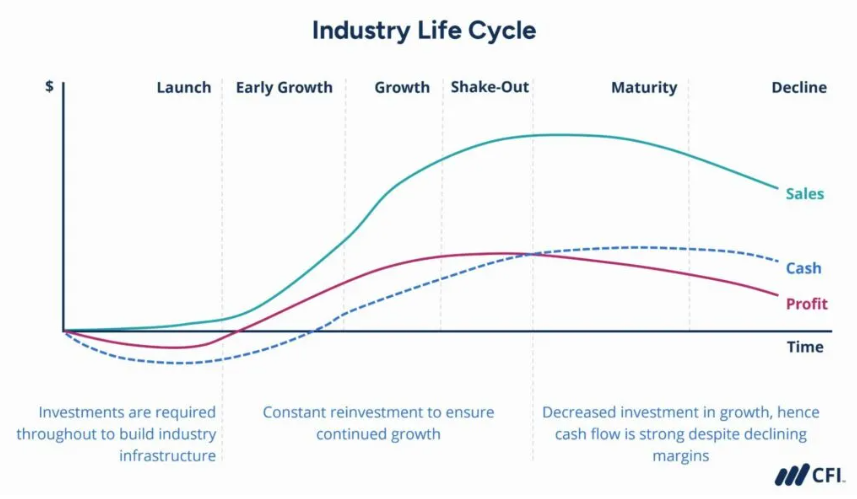

Though growth rates in various utility-style industries vary over time, none of these industries are early in their adoption curves, when growth is much faster.

source: Corporate Finance Institute

As the ILC applies to the connectivity service provider industry, while generally mature, segments within the industry that might be likened to “products” can be at different phases of their life cycles.

The fixed network voice portion of the industry clearly is declining; the home broadband segment growing. The mobile industry routinely introduced a new generation of mobile services every decade, while sunsetting the older legacy generations as that happens.

Within the mobile industry, growth is fastest in Asia-Pacific and Latin America; slowest in Europe.

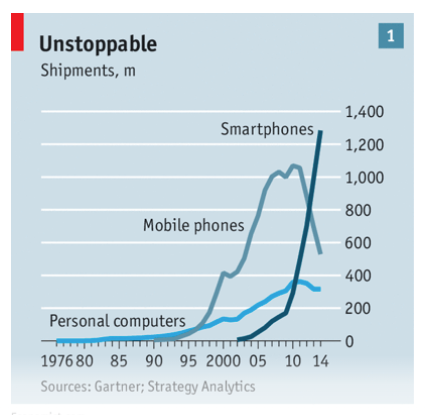

If one looks at computing devices, “personal computing” clearly has moved through a personal computer stage to a mobile phone stage to a smartphone stage.

At a high level, only fixed network voice is clearly in its “decline” phase. Mobile service is expected to continue replacing its lead platform every decade.