One common assumption about using mobile devices in a "wave and pay" application is that such alternate ways of paying for retail and other transactions necessarily will "cost retailers less" than existing methods such as paying by credit card or debit card, providing a business model for retailer adoption.

Specifically, there is some hope or expectation that retailers might be charged less money for each transaction than they now pay for supporting credit card payments. The transaction fee of about 3.5 percent is the typical target.

So far, these hopes have proven difficult. In fact, though many observers would note problems, debit card fees recently have been slashed by the Durbin Amendment to the Dodd-Frank financial services reform law, and not by any change in technological method. Debit card issuers have lost revenue, retailers have gotten lower transaction fees, but issuers still will have to make up the lost revenue some way, by raising other fees, cutting costs, or both.

Beyond that, in many cases, alternative methods, including putting charges on cell phone monthly statements, or alternative methods such as Square, actually do not save money, or even cost more than using credit card payments. Mobile money and transaction fees

Common expectations about value for end users likewise have proven elusive, to date. One advantage of "wave and pay" is the time savings. At some point, with volume deployment and consumer experience, that will be true. Right now, it is arguably the case that consumer inexperience means more friction at the point of sale. So even the hoped-for transaction time savings might not be seen, in practice. That will change over time, with greater experience.

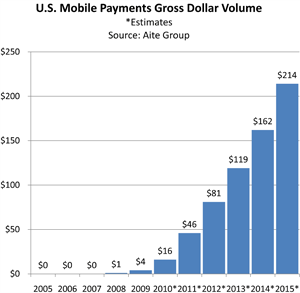

Still, the point is that mobile payments, which largely are in early deployment or testing stages, have not yet created an obvious and significant value proposition either for retailers or end users, with the notable exception of the Starbucks mobile payment system. So 2011 was not the "year of mobile payments," nor will 2012 be that year. There will be significant progress, though.

![[CABLEDEAL]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_v5t5qOpSv6daijERobcPsvqxpa9FsAI-0W-nnoIJlPrKMn1WLU-3z6zFxm8C_oiNVy0RSopwqdV7duT0IU8SLQSIpDdlMh9H27_oRT0VcbDUiPWg7GZjd2hWsnQ93qoGZ6SsyqOVHma1HSgiOICIiewP4=s0-d)