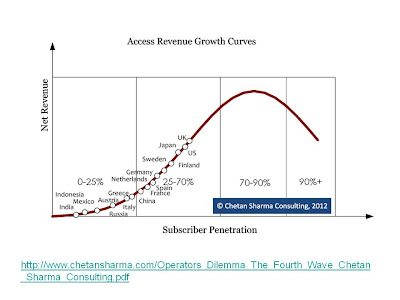

A replacement of voice revenues by data revenues at that level would be a key milestone for an industry that has for some time been grappling with the issue of how to replace lost voice revenue and profit margin.

Growing adoption of smart phones, with the new and significant data plan revenue, will play a key role, of course. Almost by definition, a smart phone activation will come with a boost in monthly revenue, from data access, of $20 to $40 a month.

But different retail packaging likely will play a key role. New shared data plans offered by AT&T and Verizon Wireless are intended to lift overall revenues while creating a usage-based data revenue model, while encouraging users to add tablets to their accounts for mobile broadband access.

What remains unclear is the extent of demand for such plans. Some think the entire industry eventually will move in that direction, as was the case with some earlier packaging innovations, including the mobile industry's abolition of domestic long distance with AT&T's Digital One Rate, or the adoption of family plans for domestic voice and texting.

But that is far from a universal view. T-Mobile USA, for example, has argued that the plans are not advantageous for consumers. And there are many subtleties. Most believe that the new plans primarily will encourage smart phone adoption, and secondarily tablet mobile connections.

Some of us might argue it is possible that the big secondary effect will be to lift personal mobile hotspot service sales, not the additional mobile network connections for tablets. The reason is that a personal mobile hotspot capability solves the same problem as a paid mobile connection for a tablet, and also has additional value.

When the personal hotspot capability is provided by the smart phone, there is no need to carry another device, such as a dongle or discrete hotspot device. Also, the personal hotspot conveniently can connect multiple devices, where a dongle connects only one device.

But that isn’t the only potential way data revenues might grow. As the number of devices with mobile network modems increases, so will the number of instances where it makes sense to have mobile network broadband.

The issue is whether that also will lead to demand for multi-device data rate plans, as Gartner believes.

The disagreement about adoption probably will not be decided, one way or the other, for some time. The reason is that the current structure of the shared data plans does not offer significantly better economics for users, compared to what they already can buy.

There are some marginal advantages and inducements to add tablet devices, for example, but the price advantage might not be so obvious to most users, or valuable.

But Gartner believes multi-device rate plans will be a key driving factor in the expansion of U.S. data revenue from $81.4 billion in 2011 to $151.9 billion in 2016.

Voice represents something on the order of 72 percent percent of total mobile service provider revenue, according to ABI Research estimates.

Messaging represents about 21 percent of total revenue, so declining messaging revenue is less a problem than lost voice revenue.

Mobile Internet revenue still is growing, in every market, so there is more time to react to the eventual maturation of that market, which at the moment only represents about six percent of total mobile service provider revenue globally, by ABI Research estimates.

The rate of mobile data revenue growth is important because voice revenues are declining. ABI Research also forecasts annual mobile voice revenues to reach $580 billion in 2010.

From 2011 on, rising subscriber saturation will increasingly erode mobile voice revenues, not just in developed markets but also in a number of emerging markets. By 2014, mobile voice revenues will have contracted by 9.6 percent.

While mobile operators have received a substantial boost from value-added services such as messaging and mobile Internet, competition is squeezing margins for a variety of services and carriers. Total mobile data services should generate $169 million in 2009 and will grow at a compound annual growth rate of nine percent until 2014.

By the end of 2009 the declines in annual average revenue per user (ARPU) will have been felt most severely in Asia-Pacific (-8.7% to $105) and Africa (-7.8% to $134). ARPU in 2009 in North America will have contracted, but only by -0.6% to $526).

All that means mobile service providers will have to work to resist voice revenue erosion while simultaneously growing data revenues.