Withim a single day on Aug. 21, 2012, MetroPCS and T-Mobile USA did what underdog firms often do, namely shake up retail pricing in an attempt to reverse flagging sales or market share.

Withim a single day on Aug. 21, 2012, MetroPCS and T-Mobile USA did what underdog firms often do, namely shake up retail pricing in an attempt to reverse flagging sales or market share. In this case, both firms announced “unlimited” data plans for smart phones.Those moves come against an industry backdrop of movement away from unlimited, flat rate data plans that threaten to erode profit margins as well as limit gross revenue opportunities.

There are a few fundamental questions one might ask. First, are such plans sustainable, by these two contestants (which is a different question than whether unlimited plans are sustainable by other competitors).

Also, related to that question, is the issue of whether the new offers will change the cost structure of T-Mobile USA and MetroPCS in some qualitative way, for better or worse.

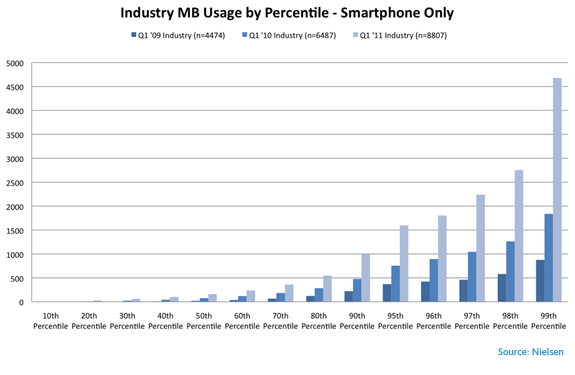

Granted, usage tends to grow, over time. But a June 2011 Nielsen monthly analysis of cell phone bills for 65,000 lines, though showing smart phone owners, especially those with iPhones and Android devices, are consuming more data than ever before on a per-user basis, the amounts are not so huge.

The amount of data the average smart phone user consumes per month has grown by 89 percent from 230 megabytes in the first quartrer of 2010 to 435 MBytes in the first quarter of 2011.

Separately, T-Mobile USA executives have noted 2012 consumption of 1.3 Mbytes a month by 4G network users. More typical users, not the “power” users, consume something on the order of 760 Mbytes a month.

In the United Kingdom, U.K. service provider Three has reported that its users have more than doubled how much mobile data they consume every month in less than a year.

The “average user” now consumes 1.1 Gbytes,, compared to 450 Mbytes in the summer of 2011.

As always “average” in the sense of “arithmetic mean” is misleading. According to U.K. service provider O2, though average consumption is 200 Mbytes a month, 0.1 percent of users consume more than 800 Mbytes a month, while 97 percent of users consume less than 500 Mbytes a month.

The point is that, for most consumers, the difference between an “unlimited” plan and a plan offering 2 Mbytes to 5 Mbytes is virtually zero, in terms of potential value. Most people just won’t use all that much data, no matter what plan they are on.

The point is that, for most consumers, the difference between an “unlimited” plan and a plan offering 2 Mbytes to 5 Mbytes is virtually zero, in terms of potential value. Most people just won’t use all that much data, no matter what plan they are on.