Thursday, April 25, 2013

1/3 of Planet Now Online

About a third of human beings now use the Internet. And most of the growth these days now comes from people in the developing regions. Mobile now represents about 10 percent of total usage, and will grow.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

New Rumor About Verizon Buying Rest of Verizon Wireless

Verizon Communications has hired advisers to prepare a possible $100 billion bid to take full control of Verizon Wireless from its partner Vodafone, according to Reuters. The latest rumor is but the latest rumor about Verizon buying the Vodafone stake.

Among the recent rumors AT&T and Verizon bid for all of Vodafone. Given slower growth in most mobile markets globally and very low interest rates, the merger activity in the U.S. and other markets is logical.

When firms cannot grow organically, they typically acquire growth.

Among the recent rumors AT&T and Verizon bid for all of Vodafone. Given slower growth in most mobile markets globally and very low interest rates, the merger activity in the U.S. and other markets is logical.

When firms cannot grow organically, they typically acquire growth.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, April 24, 2013

Does LTE Create New Revenue, or Only Displace 3G?

With every recent "next generation" of mobile networks, the hope and expectation has been that new revenue-generating services and applications would be created. That was true for 3G and now is said to be an expectation for 4G networks as well.

It's a reasonable enough hope, even if it sometimes takes quite a long time for those new revenue-generating apps to be discovered and embraced. In fact, one might argue, it was until the advent of either mobile email and mobile Internet access that "new revenue generating services" became significant.

That might logically be expected to happen for 4G Long Term Evolution networks as well. The issue is whether the "new revenue" is generated mostly by new retail policies, totally new apps, higher data consumption and therefore bigger data plans, or some combination of all of those possible trends.

Also, though it will be hard to quantify, users will simply shift from use of 3G to 4G, so LTE revenue cannibalizes 3G.

Many executives say the "new revenue" will come in large part from an end to "all you can eat" data plans that are instituted with 4G. In that case, the "new revenue" does not come from "compelling new apps" but only from changes in charging policies. That is helpful for a mobile ISP, but perhaps not the same thing as arguing LTE will create brand new apps.

So forecasts of "LTE revenue" have to be viewed with some circumspection. LTE might represent a third of revenue by 2017, Juniper Research forecasts, representing more than $340 billion worth of revenue. Other older estimates suggested faster revenue growth, but that isn't unusual early in the development of any new market.

But the magnitude of the revenue stream is not the only, or most important, new fact. Aside from cannibalizing 3G revenue, aside from representing higher data consumption, and therefore higher access fee plans, will LTE actually enable the creation of brand new applications that generate revenue? That's the big question.

It's a reasonable enough hope, even if it sometimes takes quite a long time for those new revenue-generating apps to be discovered and embraced. In fact, one might argue, it was until the advent of either mobile email and mobile Internet access that "new revenue generating services" became significant.

That might logically be expected to happen for 4G Long Term Evolution networks as well. The issue is whether the "new revenue" is generated mostly by new retail policies, totally new apps, higher data consumption and therefore bigger data plans, or some combination of all of those possible trends.

Also, though it will be hard to quantify, users will simply shift from use of 3G to 4G, so LTE revenue cannibalizes 3G.

Many executives say the "new revenue" will come in large part from an end to "all you can eat" data plans that are instituted with 4G. In that case, the "new revenue" does not come from "compelling new apps" but only from changes in charging policies. That is helpful for a mobile ISP, but perhaps not the same thing as arguing LTE will create brand new apps.

So forecasts of "LTE revenue" have to be viewed with some circumspection. LTE might represent a third of revenue by 2017, Juniper Research forecasts, representing more than $340 billion worth of revenue. Other older estimates suggested faster revenue growth, but that isn't unusual early in the development of any new market.

But the magnitude of the revenue stream is not the only, or most important, new fact. Aside from cannibalizing 3G revenue, aside from representing higher data consumption, and therefore higher access fee plans, will LTE actually enable the creation of brand new applications that generate revenue? That's the big question.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Legacy Decline is Slow, at First, in Video Entertainment, Computing or Communications

In three different legacy businesses--video entertainment, communications and computing--we see examples of how robust markets eventually mature and then decay.

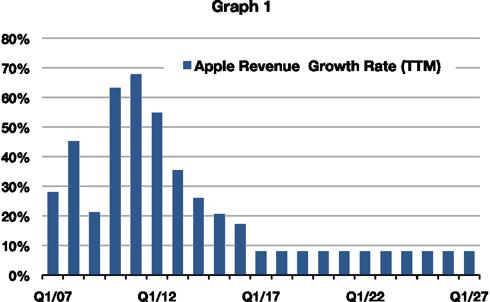

Apple. for example, might be on the cusp of transitioning from a fast-growing technology company to a slower-growing dividend-paying company, as many would argue already has happened to Microsoft.

Canada has one of the highest pay TV penetrations in the world, estimated to reach nearly 90 per cent at year-end 2012, but like the US, IHS Screen Digest expects that pay TV penetration will be on a relentless yet shallow decline decline through 2017, as many newly formed households are less likely to take a traditional TV service.

And AT&T seems to hitting something of a wall as well, as its recent earnings report show revenue is flat. If Long Term Evolution is doing anything other than compensating for declining revenues in other areas (parts of the consumer fixed network business or enterprise), it isn't immediately clear.

But it also is important to note that even if firms such as AT&T, Apple and cable companies are at a point where the growth curve flattens, there is nothing to suggest inevitable rapid decline after a peak has been reached, or passed.

In other words, transitions often build for long periods of time, with only apparently marginal and incremental changes in buyer behavior. But every big change eventually reaches an inflection point, where change is quite rapid.

The big challenge is avoiding too much optimism about what can change in the near term, and too little optimism about the magnitude of ultimate change after the inflection point is reached.

For suppliers, what happens, ideally, is a gradual decline, occurring over a relatively long time, allowing a firm time to reignite growth some other way.

On the other hand, the technology business, especially the computing business, offers a rather bracing lesson for computing suppliers.

Leaders in one era rarely survive as leaders of the next era. Some would argue the same process has been at work in the entertainment business, as it evolved from stage to radio to movies to television.

The big question is how communications might change. Some would note that we are only now at the first big change in industry dynamics, as voice services cease to be the revenue driver.

And though there is much logic to suggest the Internet access business largely will replace voice as the underpinning of the business, it is not axiomatic that today's suppliers of such access inevitably are so dominant in the future. We just cannot tell.

Though Internet access will remain a capital intensive undertaking, precisely how much capital it will take, and who can do it, will be a somewhat open question in the future.

And though one might argue that access providers these days are in a multi-product business (mobile voice, fixed voice, video entertainment, Internet access), there also are examples of "disappearance."

AT&T, for example, never was able to evolve beyond its "long distance" revenue dependence. Nor did MCI. As crazy as it sounds, we cannot say for certain, today, how Internet access will be supplied in the future, and by whom.

Apple. for example, might be on the cusp of transitioning from a fast-growing technology company to a slower-growing dividend-paying company, as many would argue already has happened to Microsoft.

Canada has one of the highest pay TV penetrations in the world, estimated to reach nearly 90 per cent at year-end 2012, but like the US, IHS Screen Digest expects that pay TV penetration will be on a relentless yet shallow decline decline through 2017, as many newly formed households are less likely to take a traditional TV service.

And AT&T seems to hitting something of a wall as well, as its recent earnings report show revenue is flat. If Long Term Evolution is doing anything other than compensating for declining revenues in other areas (parts of the consumer fixed network business or enterprise), it isn't immediately clear.

But it also is important to note that even if firms such as AT&T, Apple and cable companies are at a point where the growth curve flattens, there is nothing to suggest inevitable rapid decline after a peak has been reached, or passed.

In other words, transitions often build for long periods of time, with only apparently marginal and incremental changes in buyer behavior. But every big change eventually reaches an inflection point, where change is quite rapid.

The big challenge is avoiding too much optimism about what can change in the near term, and too little optimism about the magnitude of ultimate change after the inflection point is reached.

For suppliers, what happens, ideally, is a gradual decline, occurring over a relatively long time, allowing a firm time to reignite growth some other way.

On the other hand, the technology business, especially the computing business, offers a rather bracing lesson for computing suppliers.

Leaders in one era rarely survive as leaders of the next era. Some would argue the same process has been at work in the entertainment business, as it evolved from stage to radio to movies to television.

The big question is how communications might change. Some would note that we are only now at the first big change in industry dynamics, as voice services cease to be the revenue driver.

And though there is much logic to suggest the Internet access business largely will replace voice as the underpinning of the business, it is not axiomatic that today's suppliers of such access inevitably are so dominant in the future. We just cannot tell.

Though Internet access will remain a capital intensive undertaking, precisely how much capital it will take, and who can do it, will be a somewhat open question in the future.

And though one might argue that access providers these days are in a multi-product business (mobile voice, fixed voice, video entertainment, Internet access), there also are examples of "disappearance."

AT&T, for example, never was able to evolve beyond its "long distance" revenue dependence. Nor did MCI. As crazy as it sounds, we cannot say for certain, today, how Internet access will be supplied in the future, and by whom.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Are Apple Earnings Evidence of a Coming New Era of Computing?

Students of computing history are familiar with the notion that each distinct era of computing has been lead by a different set of companies than lead the era that preceded the new era. that doesn't mean, in some mechanical fashion, that the leaders of a former era always disappear.

Some will note that IBM still exists, though as a far different sort of company. In fact, one might say other leaders in past eras, including HP and Dell, are trying to recreate themselves largely on the IBM model, which is to say as consulting specialists, not hardware suppliers.

Its too early to say if the pattern will hold in the next era to come. But history suggests the pattern will hold. If so, household names such as Apple might cease to be seem as the trendsetters of the next era.

It is a shocking concept, to be sure. But some observers would say the recent Apple earnings call, with its predictions of slowing growth, declining profit margins and a greater emphasis on the "value" element of owning Apple equity, rather than growth, illustrate the process at work.

As happened to Microsoft before it, Apple might be on the cusp of becoming a "value play," not a "growth play." The corollary, one might also argue, is that as Microsoft is seen in many quarters as "not leading" in computing any longer, so Apple in several years might also be seen as a past leader, not a current leader.

It's shocking, but history suggests it will happen.

Some will note that IBM still exists, though as a far different sort of company. In fact, one might say other leaders in past eras, including HP and Dell, are trying to recreate themselves largely on the IBM model, which is to say as consulting specialists, not hardware suppliers.

Its too early to say if the pattern will hold in the next era to come. But history suggests the pattern will hold. If so, household names such as Apple might cease to be seem as the trendsetters of the next era.

It is a shocking concept, to be sure. But some observers would say the recent Apple earnings call, with its predictions of slowing growth, declining profit margins and a greater emphasis on the "value" element of owning Apple equity, rather than growth, illustrate the process at work.

As happened to Microsoft before it, Apple might be on the cusp of becoming a "value play," not a "growth play." The corollary, one might also argue, is that as Microsoft is seen in many quarters as "not leading" in computing any longer, so Apple in several years might also be seen as a past leader, not a current leader.

It's shocking, but history suggests it will happen.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Netflix Success Challenge in a Nutshell

In a nutshell, the key challenge for Netflix is to "grow members and revenue faster than content spending," as the latest Netflix shareholder letter mentions. In other words, Netflix has effectively become a programming network, not just a content delivery service.

And as has been true for all programming networks, original and unique content is the growth driver. That doesn't mean every bit of content, or even most content, has to be unique to a particular network. But virtually all popular networks have one or more "signature series" that define the network and pull in viewers.

Netflix will have to invest to do so, and that means there is going to be a tension between doing so and then adding enough additional new subscribers to keep its profit margins intact.

And as has been true for all programming networks, original and unique content is the growth driver. That doesn't mean every bit of content, or even most content, has to be unique to a particular network. But virtually all popular networks have one or more "signature series" that define the network and pull in viewers.

Netflix will have to invest to do so, and that means there is going to be a tension between doing so and then adding enough additional new subscribers to keep its profit margins intact.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple Financial Results Answer No Key Questions

Apple's fiscal 2013 second quarter ended March 30, 2013 included quarterly revenue of $43.6 billion and quarterly net profit of $9.5 billion, compared to revenue of $39.2 billion and net profit of $11.6 billion for the same quarter of 2012.

Despite posting results most companies would be happy to report, such as "average weekly growth of 19 percent, Apple's quarterly results do not answer any of the strategic questions observers now have about the company.

What is the "next big thing" to drive Apple sales and customer delight?

Can Apple create yet another big new market? Perhaps most importantly, has Apple lost the creative edge and become a "normal company" with a "normal growth rate?

In fact, some think single-digit growth rates are where Apple is headed, in perhaps five years.

Nor, it appears, will it be possible to resolve any of those questions until perhaps September 2013, or possibly even 2014, when Apple says it will launch the next round of new products. "Our teams are hard at work on some amazing new hardware, software, and services that we can’t wait to introduce this fall and throughout 2014," CEO Tim Cook said.

And while the big strategic questions are not narrowly financial, financial performance is an issue. Gross margin was 37.5 percent compared to 47.4 percent in the year-ago quarter, for example.

Apple estimates its gross profit margin will dip a bit further in the next quarter, and the company faces sharply declining rates of growth. Questions about Apple strategy also revolve around the likely impact on margins if lower-cost iPhones, despite the company's denials, are launched, as is the case for lower-cost iPads as well.

International sales accounted for 66 percent of the quarter’s revenue, and growth was driven by the iPhone and iPad. Apple sold 37.4 million iPhones in the quarter, compared to 35.1 million in the year-ago quarter.

Apple also sold 19.5 million iPads during the quarter, compared to 11.8 million in the year-ago quarter.

By way of comparison, sales of sold just under four million Macs, compared to four million in the same quarter of 2012 show a slight decline.

Despite posting results most companies would be happy to report, such as "average weekly growth of 19 percent, Apple's quarterly results do not answer any of the strategic questions observers now have about the company.

What is the "next big thing" to drive Apple sales and customer delight?

Can Apple create yet another big new market? Perhaps most importantly, has Apple lost the creative edge and become a "normal company" with a "normal growth rate?

In fact, some think single-digit growth rates are where Apple is headed, in perhaps five years.

Nor, it appears, will it be possible to resolve any of those questions until perhaps September 2013, or possibly even 2014, when Apple says it will launch the next round of new products. "Our teams are hard at work on some amazing new hardware, software, and services that we can’t wait to introduce this fall and throughout 2014," CEO Tim Cook said.

And while the big strategic questions are not narrowly financial, financial performance is an issue. Gross margin was 37.5 percent compared to 47.4 percent in the year-ago quarter, for example.

Apple estimates its gross profit margin will dip a bit further in the next quarter, and the company faces sharply declining rates of growth. Questions about Apple strategy also revolve around the likely impact on margins if lower-cost iPhones, despite the company's denials, are launched, as is the case for lower-cost iPads as well.

International sales accounted for 66 percent of the quarter’s revenue, and growth was driven by the iPhone and iPad. Apple sold 37.4 million iPhones in the quarter, compared to 35.1 million in the year-ago quarter.

Apple also sold 19.5 million iPads during the quarter, compared to 11.8 million in the year-ago quarter.

By way of comparison, sales of sold just under four million Macs, compared to four million in the same quarter of 2012 show a slight decline.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...