In many ways, mobile service providers might hope Western Europe does not represent the future of the global business. In some ways, fixed network operators might hope Western Europe is a model for the future.

The reason is that fixed network revenue sources seem to be growing, as a percentage of total industry revenues, compared to mobile revenue sources, which seem to be shrinking, as a percentage of total industry revenues.

That doesn’t necessarily mean fixed network revenue is growing; it simply is shrinking more slowly than mobile revenues.

It appears mobile is poised for more serious revenue declines than fixed services. “A key factor is mobile's dependence on legacy non-data services compared with fixed-line or cable,” Analysys Mason says.

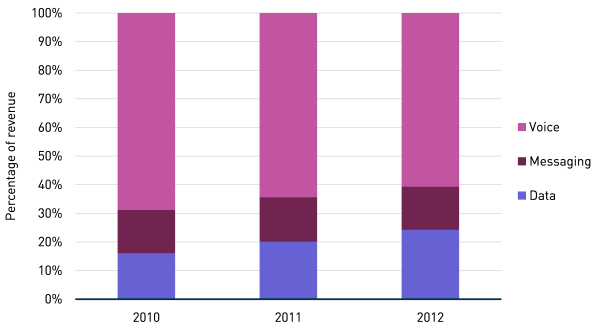

Already, about 67 percent of fixed operator revenue (excluding content) in Western Europe came from data in 2012.

In fact, though it will strike many as odd, the Great Recession and continuing economic sluggishness in Europe has produced evidence that European consumers consider their fixed service more essential than their mobile services, something many would assumed would operate in the reverse--with mobile services deemed more important than fixed.

Fixed service revenue seems to have been more stable than mobile revenues. In fact, fixed-line bundles have the best take-up in some of the more economically challenged countries, Analysys Mason notes.

Perhaps the primary reason for that fixed network preference is the value-price relationship, compared to the value-price relationship for mobile Internet access.

Also, with growing availability of Wi-Fi access in public and outside the home areas, it is easier to use “Wi-Fi only” or “Wi-Fi mostly” as the Internet access medium.

Oddly enough, after a long period where global growth was driven by mobile services, there now appears to be an opportunity for at least some new growth in the fixed network space based on providing services to mobile users.

Mobile data traffic increasingly is used at locations where fixed operators can supply most customer needs at lower cost and price. The reason is that most consumed data occurs when people are not “out and about,” but at stationary locations, most commonly the home or office.

Though a decade ago the notion that Wi-Fi hotspot networks could be a substitute for mobile access proved incorrect, some believer there could well be a different business terrain over the next several years.

Potentially, fixed broadband providers could cooperate with public Wi-Fi providers, or use owned assets, to create Wi-Fi access that is a reasonably useful primary Internet access method for some customers.

To counter that threat, mobile operators are adding their own public Wi-Fi networks, in part to offload traffic from the mobile network and in part to provide data services at lower cost.

The important potential new development is the reversal of “growth” prospects for mobile and fixed networks. Or, as some analysts suggest, which segment will decline less.

Mobile Service Provider Revenue Sources

Fixed Network Service Provider Revenues

Perhaps significantly, mobile spending is viewed as more discretionary than fixed network spending, by analysts at Analysys Mason.

Recent results from larger operators in Europe already show faster decline in mobile retail revenue than in fixed, and Analysys Mason forecasts that mobile will represent a declining share of total operator retail telecoms revenue during the next five years.

Spain might provide an example. Though overall service provider revenue is projected to decline over the next two years, fiber-based services on the fixed side and wholesale services or business-to-business mobile services are where revenue growth will be found, according to a new analysis by Pyramid Research.

The Spanish communications market generated €22.6bn ($29.0bn) in 2012, which represented an eight percent decline year-on-year.

Due to the prolonged economic recession, expected to last another two years in Spain, communications market service revenue will return to growth in 2015, up 2.3 percent a year.

Fiber to the home revenues will grow at a compound annual growth rate of 58 percent between 2013 and 2018, reaching $3.3bn in 2018,” says Pyramid Research Senior Analyst, Stela Bokun.

Mobile revenue growth will come from the enterprise and wholesale segments.

The key takeaway is that revenue growth will be tough, and that growth might be stronger (or declines less sharp) in the fixed network segment of the business.

It is not directly a commentary on the value of near field communications, but Google’s introduction of a new version of the Google Wallet app, rolling out the week of Sept. 15, 2013, is part of Google’s overall approach to apps, which is to make them available on all platforms.

It is not directly a commentary on the value of near field communications, but Google’s introduction of a new version of the Google Wallet app, rolling out the week of Sept. 15, 2013, is part of Google’s overall approach to apps, which is to make them available on all platforms.