Tuesday, October 15, 2013

Verizon Wireless Tests 80-Mbps Service in Manhattan

If you have enough bandwidth, you can offer really-fast Long Term Evolution. That is notably true for LTE networks. In that regard, Verizon Wireless seems to be testing LTE at 80 Mbps in Manhattan.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

How Much Difference Will LTE Make in U.K. Market?

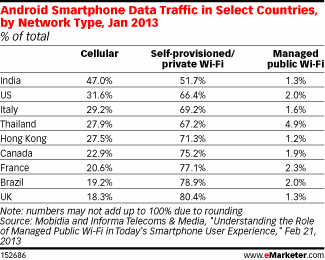

U.K. consumers increasingly are using mobile devices to connect to the Internet, but as is the case elsewhere, increasingly they also are using Wi-Fi to do so. In fact, some studies suggest as much as 80 percent of U.K. Internet access using a mobile handset uses a Wi-Fi connection for access.

U.K. consumers increasingly are using mobile devices to connect to the Internet, but as is the case elsewhere, increasingly they also are using Wi-Fi to do so. In fact, some studies suggest as much as 80 percent of U.K. Internet access using a mobile handset uses a Wi-Fi connection for access.

That could have important implications for fourth generation network Long Term Evolution demand. If 80 percent of Internet access is at home, on a Wi-Fi network, what is the value of out of home 4G access?

Even if 4G access provides a better experience than 3G, what is the value of better experience 20 percent of the time, especially if the out of home use is mostly for applications that do not necessarily require or benefit much from the faster speed?

According to the Oxford Internet Institute, 57 percent of web users in Great Britain will access the Internet using a mobile device in 2013.

According to the Oxford Internet Institute, 57 percent of web users in Great Britain will access the Internet using a mobile device in 2013.

Some observers including eMarketer, think the increased availability of 4G access will change consumer behavior. Others might be so sure.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Is Nokia a Metaphor for European Mobile Business?

Is Nokia in some ways a metaphor for Europe’s mobile industry? On the supply side, what I mean by that is simply that Nokia had such a great understanding and leadership of the feature phone market that it could not shift to the different smart phone market.

Is Nokia in some ways a metaphor for Europe’s mobile industry? On the supply side, what I mean by that is simply that Nokia had such a great understanding and leadership of the feature phone market that it could not shift to the different smart phone market.

On the demand side, it might be argued that consumer preferences in Europe and the United States simply are different. Nokia had such a lead in many markets because Nokia supplied what consumers wanted.

In that sense, are we at a point where European consumer demand for 4G services actually is limited, in the way demand for 3G once was limited, irrespective of supply?

In other words, though regulators and mobile service providers alike seem to agree more can be done to stimulate deployment of 4G Long Term Evolution networks in Europe, one wonders whether consumer preferences create barriers in that regard.

In other words, though regulators and mobile service providers alike seem to agree more can be done to stimulate deployment of 4G Long Term Evolution networks in Europe, one wonders whether consumer preferences create barriers in that regard.

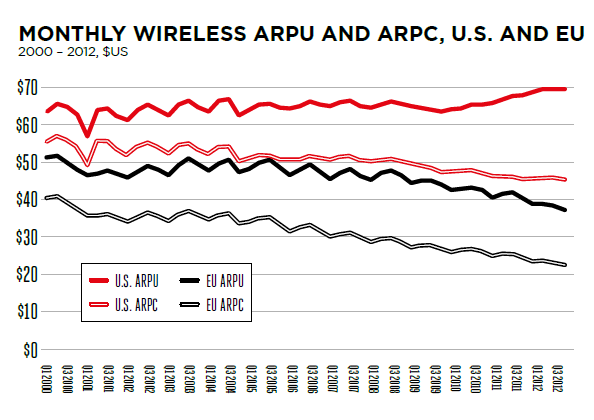

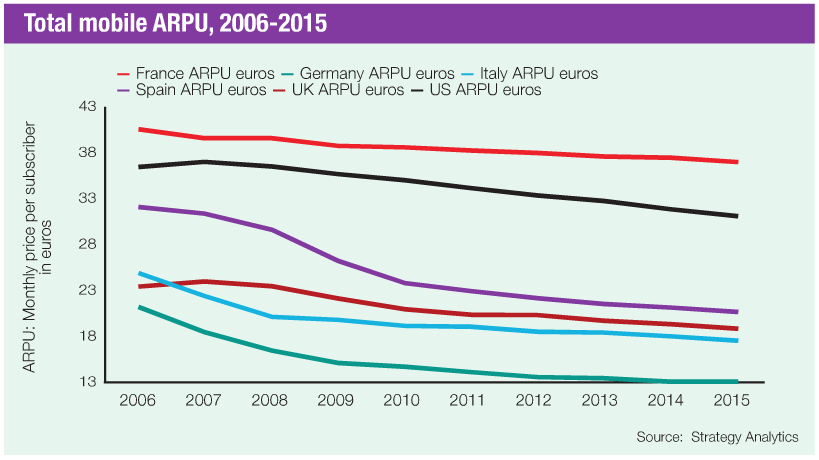

U.S. consumers use five times more voice minutes and nearly twice as much data as European consumers on a monthly basis. But Stéphane Téral, Infonetics Research principal analyst notes that mobile broadband is the revenue growth driver, even if European consumers seem to prefer to spend less on mobile Internet access than U.S. consumers prefer.

On the other hand, the question might be whether, at the moment, 3G is viewed by consumers as satisfactory. In the absence of a 4G alternative, it is hard to know for sure.

LTE broadband is growing the fastest of any mobile services category, Téral says. That might be why AT&T sees European expansion as potentially lucrative, and why regulators want faster 4G network deployment.

U.S. consumers might be more engaged with Internet apps than consumers in Europe might be, and use and value mobile broadband and fast data access more than European consumers do, at least for the moment.

That is not a matter of “ahead or behind,” but simply of “difference.” And demand can change.

As U.S. consumers once valued mobile phones and text messaging less than Europeans, that eventually changed. European demand for LTE 4G could change as well. The issue, for some, might be “when” demand changes.

To be sure, a lag in LTE is viewed as a problem. In May 2013, GSMA issued a report arguing Europe was “falling behind” the United States in next generation mobile deployment. Ignoring for the moment past claims of that sort that had the United States lagging Europe, which only suggests markets change, the GSMA worries about fourth generation network in Europe.

On average, U.S. consumers spend more each month than their EU counterparts and use mobile services much more intensely, consuming five times more voice minutes and nearly twice as much data.

Average mobile data connection speeds in the U.S. are now 75 per cent faster than those in Europe and by 2017 will be more than twice as fast.

One expression of the problem is that mobile Internet access revenue in Europe is not growing fast enough to offset losses of voice revenue, though some hope the decline can be arrested.

But why that is the case is the strategic issue, with respect to 4G investment. Perhaps mobile data consumption is not growing as fast because that is what consumers prefer, and not because the networks are limited in some way. If that is the case, building 4G will only cause more financial losses.

And it might be hard to dismiss the argument that consumers are being careful about paying more for mobile service because of current economic conditions, suggesting a slower introduction of LTE is not as big a problem as the level of consumer demand.

Mobile accounts continue to shrink in Spain, for example, a problem that some hoped had reached an end in May 2013, when accounts actually grew after 10 months of decline. But June 2013 showed another drop.

Spanish mobile accounts in service were 51.9 million at the end of June 2013, down 4.9 percent from 54.6 million for the same month of 2012. With the exception of acquisition-aided growth, every mobile operator lost customers.

Movistar, Spain’s biggest mobile operator, lost 102,000 lines during the month, Vodafone lost 90,000, and Yoigo lost 121,900 lines. Orange gained 41,000 based on acquired firm Simyo.

source: Analysys Mason

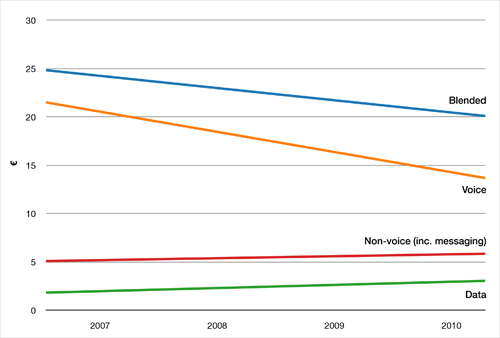

EU27: Average Revenue Per User (ARPU) 2007-2010

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, October 14, 2013

How Big a Problem are Smart Phone Device Subsidies?

Device subsidies are an issue for mobile service providers, as they are a drag on earnings, but device subsidies might not as big a problem as being viewed as a commodity provider of dumb pipe access.

Some argue mobile service providers would be better off not subsidizing devices at all. Others might agree in principle, but note that the device subsidies reduce a key barrier to end user adoption of more-capable devices that drive mobile Internet access revenue.

So mobile service providers might be said to face a “lesser of two evils” problem. Not subsidizing smart phones would improve operating results, but at the risk of slower adoption of mobile devices benefiting from mobile Internet access plans that now drive revenue growth.

And that is why, problem or not, mobile service providers face significant challenges getting “out of the device subsidy business.” Device subsidies or installment plans are a problem, but probably a lesser problem than jeopardizing demand for mobile Internet access.

There are other imponderables as well. Historically, it has been very difficult to create a positive brand image for a service provider. Consider, by way of comparison, the intense or at least significant importance of brand affiliation for personal care products, clothing, automobiles or other “personal” products.

You might argue that the smart phone is the first tangible expression, in the history of the telecommunications business, of an attribute of the communications experience that is truly “personal.” The problem is that the affiliation still is with a device, not with the actual “access service” or the provider of the access service, necessarily.

In getting out of the device business, service providers might forfeit even more distinctiveness in the market, shift end user affiliation even further in the direction of emotional bonding with the device, not the access provider brand, and have less leverage over consumer accounts.

So, yes, the cost of financing handsets is a “problem,” but it might well be less a problem than becoming more of a dumb pipe supplier of access than mobile service providers already face.

“Mobile carriers are subsidizing handsets, but not reaping the return on investment as over the top service providers take revenue share,” says ABI Research. That is true, but is true of the business, in some parts of the world, not a particular function of the device subsidies or installment plans.

That might be true even if a device subsidy is the single largest cost for a carrier over the lifetime of a subscriber’s contract. ABI Research argues that 68 percent of the revenue derived from a typical 24 month contract has to cover the cost of the device.

Some might quibble with the precise figure, but the point is that a device subsidy or installment plan does represent a significant part of the cost of customer account over a two-year period.

Some might argue the mobile cost of service is high “because of the subsidies.” Others might disagree. The posted retail prices in any country are hard to compare directly. What makes more sense is the affordability or cost of mobile service in terms of local purchasing power or income.

In fact, some might argue the price of mobile service in the United States is among the lowest in the world, expressed as a percent of personal income.

One might argue that is a good reason for improving the transparency of the device purchase. But one might also argue that mobile service providers already are doing so, creating installment plans that separate device acquisition from recurring service cost, for example.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

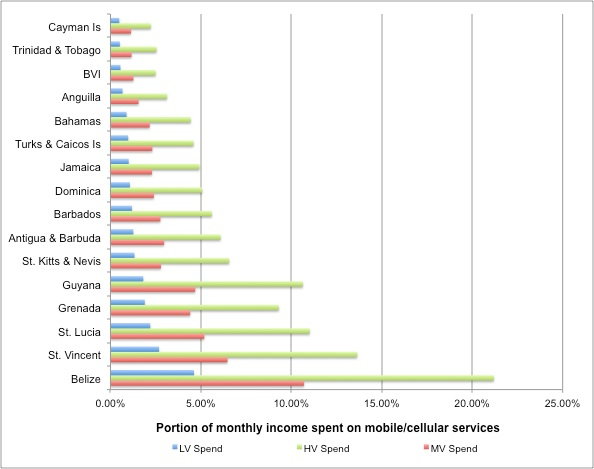

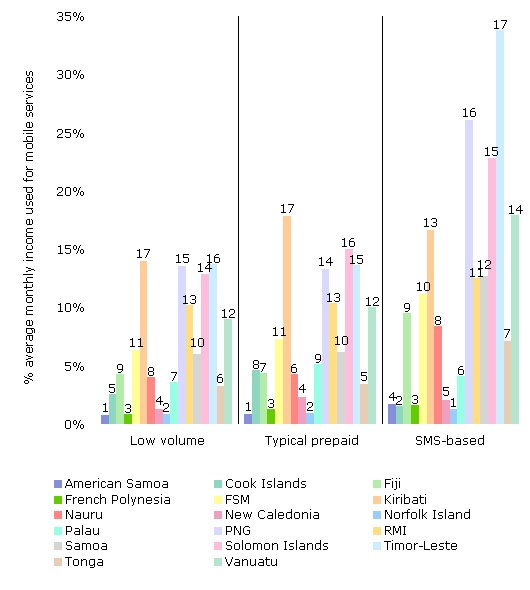

U.S. Mobile Service Prices Actually are Quite Low

Comparing retail prices for anything across countries is difficult, largely because income and costs for anything are different across countries. For that reason, some believe the better gauge is not actual prices for anything, but the price as a percentage of income and costs in any single country.

Comparing retail prices for anything across countries is difficult, largely because income and costs for anything are different across countries. For that reason, some believe the better gauge is not actual prices for anything, but the price as a percentage of income and costs in any single country.

The bottom line is that where a U.S. mobile service customer might represent a percent or two percent of income, in many countries in the Americas mobile service costs five percent to 15 percent of income, and the same situation prevails in many of the Pacific Islands, for example.

Beyond that, there are lots of other issues that make such determinations complicated. Light users will spend less than heavy users, prepaid users might pay less than postpaid users. Feature phone users might pay less than smart phone users. Users on shared service plans might pay less, per user, than single-person accounts.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Beyond that, there are lots of other issues that make such determinations complicated. Light users will spend less than heavy users, prepaid users might pay less than postpaid users. Feature phone users might pay less than smart phone users. Users on shared service plans might pay less, per user, than single-person accounts.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Structural or Cyclical Problems?

One good reason for studying and understanding economics is that it can concentrate the mind and alleviate any tendencies to think “one side or the other” is evil and incompetent, as so much of U.S. political discourse would illustrate.

One good reason for studying and understanding economics is that it can concentrate the mind and alleviate any tendencies to think “one side or the other” is evil and incompetent, as so much of U.S. political discourse would illustrate.

And with the caveat that long-term trends are difficult to discern without lots of data, collected over long periods of time (I am sitting at 5,278 feet, in an area that once was an inland sea), a rational person might at least hold open for discussion the notion that something “big” has changed, regarding the U.S. economy.

Look at the history of labor force participation rates (recessions marked by gray columns). The data might suggest there is something structural going on. And that is a tougher problem than a shorter-term cyclical problem.

If you care about people being able to find jobs, this is a big problem.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Australia to Study Impact of Broadband: Issue Really is Cost, Timing

The Australian government will conduct an independent cost-benefit analysis of the National Broadband Network and a review of the regulations relating to broadband, as new questions about the cost of the fiber-to-home network has come into question.

The more-abstract study of economic benefits of faster broadband is almost beside the point. It is not likely any truly-useful predictions can be made about the economic impact of various speeds and network architectures.

The more-important conclusions are likely going to be the projected cost of fiber-to-home versus fiber-to-neighborhood network architectures, speed to market and projected growth of consumer demand for higher speeds that would justify spending more, immediately, on one access method versus the other.

The Australian National Broadband Network has been unable to meet its planned construction targets, and the government now questions the cost, as well.

The more-abstract study of economic benefits of faster broadband is almost beside the point. It is not likely any truly-useful predictions can be made about the economic impact of various speeds and network architectures.

The more-important conclusions are likely going to be the projected cost of fiber-to-home versus fiber-to-neighborhood network architectures, speed to market and projected growth of consumer demand for higher speeds that would justify spending more, immediately, on one access method versus the other.

The Australian National Broadband Network has been unable to meet its planned construction targets, and the government now questions the cost, as well.

The change to a less fiber-intensive network is said to represent a final cost of A$20.4 billion (US$18.4 billion), well below the A$38 billion ($33.8 billion) originally stimated for the fiber to home plan, and far less than the $94 billion critics now say the former network would cost.

Some critics estimate that the Australian National Broadband Network (NBN) will cost A$94 billion dollars, not the A$44 billion its supporters have claimed. At least in part, that is because

of delays of several types and overly-optimistic assumptions.

The original business plan assumes wholesale revenue will start at $22 per month and then climb to $62 by 2020 or 2021 when the NBN is finished. That is growth of nine percent a year beyond inflation.

Other major ISPs might say average prices for Internet access do not climb more than nine percent a year.

So critics say revenue projections are wildly overestimated.

What study of the benefits of broadband access has ever found anything but "it is a good thing?" The choice in this case is between faster networks and slower networks, not so much between the "fastest network" and a "fast network."

The problem is that the Internet is an ecosystem. So upgrading access speeds on one end of a connection delivers only so much benefit, if the rest of the ecosystem is not upgraded for those speeds, at the same time. And, of course, that never happens. Change comes incrementally.

Still, some would argue it is better to "waste" bandwidth and capital by moving immediately to fiber-to-home architectures. Others would say the immediate benefits, for consumers, businesses and the economy, would not be so much greater for fiber to home that the extra time and capital should be invested.

What probably will happen is that a mix of technologies will be used, as originally was planned. Satellite will continue to be used in rural areas. Fiber to home will continue to be used where it is feasible. But a greater percentage of locations might use fiber to the neighborhood.

It never was envisioned that fiber to home would be the architecture for all areas.

What probably will happen is that a mix of technologies will be used, as originally was planned. Satellite will continue to be used in rural areas. Fiber to home will continue to be used where it is feasible. But a greater percentage of locations might use fiber to the neighborhood.

It never was envisioned that fiber to home would be the architecture for all areas.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Useful Life of a GPU is Not So Clear

Perhaps depreciation is not typically a key business model issue, but that seems not to be the case for hyperscalers who have extended the ...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...