It is starting to look as though tablet connections are the new near-term growth driver for at leaset a couple of the top-four U.S. mobile service providers. Specifically, Sprint probably still is losing phone accounts, Verizon Wireless is still gaining them, while T-Mobile US and AT&T Wireless are growing on the strength of tablet connections.

And that might explain why T-Mobile US to offer U.S. tablet owners up to 200 MB of free 4G LTE data every month for as long as they own their tablet, even if they're not yet a T-Mobile customer.

T-Mobile US is banking on those users adding mobile network service for their tablets, and offers a trade-in program allowing users to get a mobile-capable device instead.

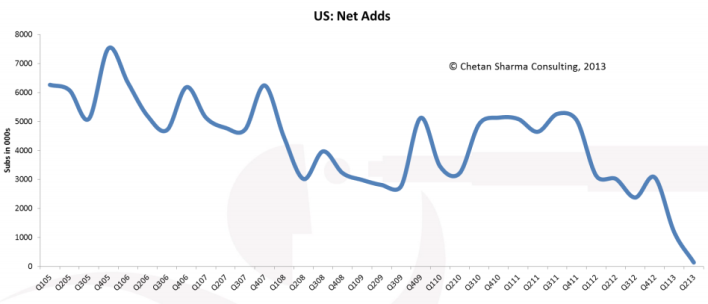

Indeed, the growing importance of tablet connections is about the only way to explain recent net addition trends at the big four national carriers.

If T-Mobile US and Verizon Wireless each gain nearly a million net customers in a quarter, AT&T adds half a million and Sprint loses half a million, in a context where 90 percent of net adds must come from some other carrier’s market share, the numbers do not add up. Simply, there are more accounts being added than are possible, counting only phones.

The only clear implication is that other service providers took about half a million Sprint customer accounts. Beyond that, the only significant change in U.S. mobile market dynamics is that T-Mobile, has moved from losing customers to gaining a significant number of them.

What seems to be happening is that most of the net new additions are driven by tablets and other machine-to-machine connections of various types, such as alarm connections.

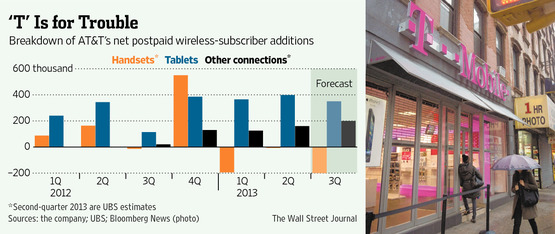

Analysts say AT&T has lost some phone accounts to T-Mobile US. Of 551,000 net postpaid wireless subscribers AT&T added in the second quarter, 398,000 were for tablets.

UBS estimates 160,000 were for other connections, such as home security or wireless home-phone service. AT&T lost a net 7,000 mobile-phone customers.

AT&T had not reported its third quarter results at the time this story was filed, but UBS analysts expected net additions of 350,000, virtually all from tablet connections , with 200,000 other net new connections canceling out a net loss of 200,000 phone subscribers.

That new tablet trend is especially crucial as overall mobile service provider net additions have been shrinking since the end of 2011, and perhaps 90 percent of all new net additions now are taken from another service provider.

And though we will have to wait for a full answer, a reasonable question for the future, when Sprint launches its expected effort to recapture market share, is which carriers will take share from which other carriers.

Will Sprint and T-Mobile US take market share from each other, from AT&T or from Verizon Wireless?

Verizon Wireless has been outpacing AT&T, Sprint and T-Mobile US at adding net new “customers” since about 2010.

Verizon Wireless, for example, added 1.1 million net retail connections, including 927,000 retail postpaid net connections, in the third quarter of 2013, to grow total retail connections to 101.2 million connections, up 5.5 percent year over year.

Some 95.2 million of those retail connections were postpaid connections. If AT&T, T-Mobile US and Sprint report third quarter results in line with their second quarter reports, we might expect T-Mobile US to add a million customers, AT&T to gain half a million and Sprint to lose about half a million.

So we might expect about 2.5 million net adds at Verizon, AT&T and T-Mobile US, with Sprint losing about half a million. In other words, about two million net accounts would be added, of which possibly 1.8 million represent market share shift.

If the market is mostly a zero-sum game, where 90 percent of all net adds are taken from a competitor, the net adds are greater than the net losses, and they should balance, if we are looking at a market that is 90 percent zero-sum.

That net adds exceed those figures illustrates the impact of tablets being added.