One would expect service providers to focus their sales and customer efforts in market segments where telecom industry revenue growth is highest, or where profit margins are highest, in both retail and wholesale portions of the business.

For example, U.S. local wholesale voice revenues will decline from $6.1 billion in 2013 to $5.4 billion in 2014, according to Atlantic-ACM, while U.S. long distance wholesale voice revenues will decline from $2 billion in 2013 to $1.6 billion in 2014.

In a market with total U.S. telecom revenue in the $400 billion range (including video entertainment revenues), that level of wholesale voice revenue is almost nothing.

In the United Kingdom, there is some evidence that aggregate wholesale revenues began to decline, as a percentage of total service provider revenues, in 2011.

Total European wholesale revenue declined by 6.2 percent in 2012 to $45.1 billion, Ovum estimates, while service provider retail revenues fell by 10 percent in the same period. As you might guess, voice revenue declines were key drivers of the change.

In 2012 the European wholesale fixed voice sector accounted for less than a third of total wholesale revenues in the region, while revenues were 13 percent lower than in 2011, part of a downward trend in place for more than a decade.

Under those conditions, one would expect suppliers to focus on growth segments (new customers, apps or geographies) while deemphasizing declining and small segments.

Findings of a survey conducted by Atlantic-ACM of global wholesale buyers suggests that principle is at work in the wholesale telecom business , even if overall buyer satisfaction has remained stable since 2010.

Early in 2014, satisfaction among large customers virtually leaped five percent among large customers. On the other hand, satisfaction among smaller customers declined 0.5 percent early in 2014.

Customers in fixed network verticals reported satisfaction levels 1.1 percent lower, while satisfaction among customers with operations in mobile service grew 5.3 percent.

Customers in “emerging markets” (cable/content/ISP verticals, resellers/systems integrators and data center/hosting/cloud providers) reported satisfaction levels 2.1 percent higher.

But a reasonable argument also can be made that satisfaction will be higher in some geographies, since growth prospects are so much higher in a few regions, such as some newly-emerging parts of Asia.

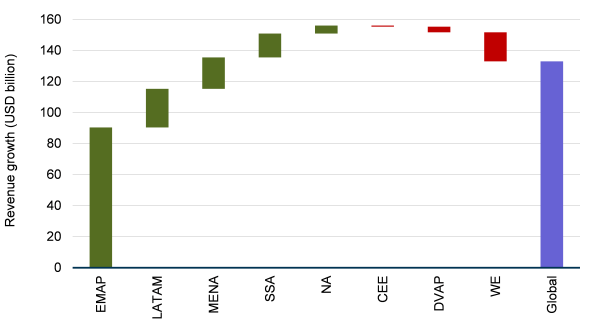

Between 2012 and 2017, most of the incremental revenue will be generated in the emerging Asian countries. In Central and Eastern Europe, developed Asian markets and Western Europe, revenue actually will shrink.

According to Analysys Mason, the global market for telecom services generated retail revenue of US$1.54 trillion in 2012, of which around two thirds was from the developed markets of North America (NA), Western Europe (WE), Central and Eastern Europe (CEE) and Developed Asia–Pacific (DVAP).

About a third of revenue came from emerging markets, including “Emerging Asia–Pacific” (EMAP), Latin America (LATAM), Middle East and North Africa (MENA), and Sub-Saharan Africa (SSA).

The United States was the largest market (US$378 billion), followed by China (US$151 billion), Japan (US$133 billion), Brazil (US$61 billion) and Germany (US$53 billion).

Analysys Mason predicts that retail revenue worldwide will grow at a 1.7 percent compound annual growth rate between 2012 and 2017, with growth in mobile (3.2 percent) more than offsetting a decline in fixed (–0.6 percent).

Global Telecom Service Revenue Growth

source: Analysys Mason

{kind=link}