Disruption on a major scale of the U.S. video entertainment ecosystem seems highly unlikely, for the moment, despite building pressures that suggest the current pattern cannot last forever.

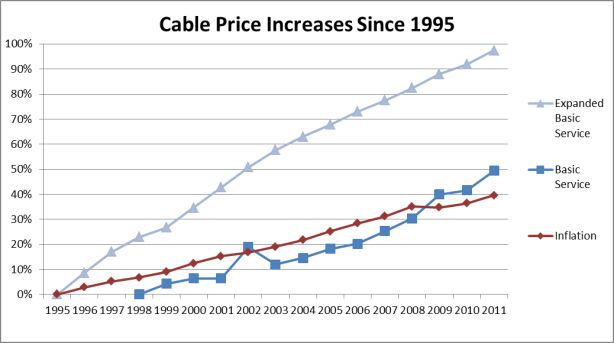

Virtually every observer notes that U.S. cable TV prices have grown at least 100 percent over a decade, at least double the underlying rate of inflation, as measured by the consumer price index.

Many would rationally argue that cannot continue for decades more, as the value-price relationship will grow unappetizing.

Should current rate increases prevail, in 10 years a typical consumer could be paying $200 to $300 a month for the equivalent of today’s “expanded basic” package, while other prices grow less than 33 percent over a decade, and possibly less.

Perhaps enough value will be added that such prices are deemed reasonable. But many would argue that seems unlikely.

Since 2000, the U.S. consumer price index (which excludes housing prices) increased by about 34 percent, while another index, the “Everyday Price Index,” which includes such costs, shows a 57 percent increase between 2000 and 2012.

Even using the EPI figures, cable TV prices have grown nearly twice as fast between 2001 and 2011 as average consumer prices, and as much as three times as much by some standard measures, for example.

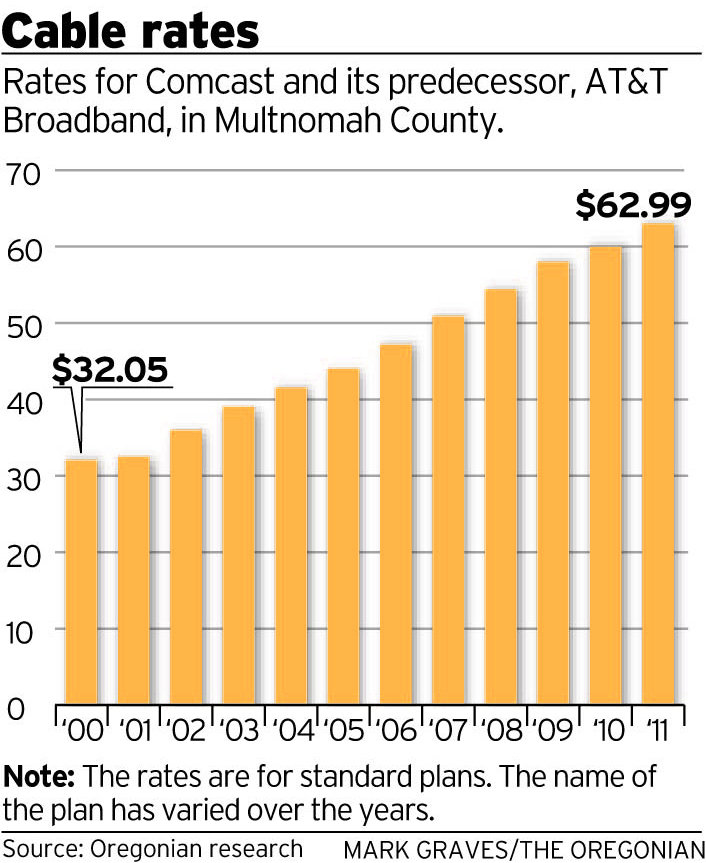

Video prices subscription prices In Multnomah County, Oregon, for example, grew by about 100 percent from 2000 to 2011, exceeding the background consumer price index and the everyday price index.

Some might point to services such as Netflix, available for roughly $10 a month, and compare that to an HBO subscription, which might cost $15 a month, and see a way for single channels to be sold at retail for about $10 to $20 a month on a stand-alone, streamed basis.

If similar economics prevailed for most networks generally, whether any given subscriber is better served buying a la carte, or buying a subscription, hinges on the number of channels or programs normally viewed.

If single channels could be purchased for $15 a month, then a consumer now paying $90 a month would break even at about six channels. A household habitually viewing more than six channels still would come out ahead simply buying a bundled subscription. But nobody really knows what economics of unbundled channel access actually would emerge.

Some argue that essentially little change would occur, and that typical households might wind up paying about the same amount each month, in an unbundled scenario where customers can buy channels one by one.

Studies by the Federal Communications Commission are inconclusive about whether unbundling would, or would not, save money. One of the studies suggested “consumers that purchase at least nine networks would likely face an increase in their monthly bills” when buying a la carte.

Likewise, one of the studies suggested bill increases ranging from 14 percent to 30 percent under a la carte, while the other suggests a consumer purchasing 11 cable channels would face a change of bill ranging from a 13 percent decrease to a four percent increase, with a decrease in three out of four cases.

The point is that it is very hard to tell, conclusively, what might happen if providers shifted to a la carte viewing.

Nor, given content owner preferences and contract clauses, are we likely to find out very soon.

In truth, video distributors have little discretion about where to place channels (most contracts for ad-supported channels require placement on the most-viewed tier of service), and no freedom to sell any channel a la carte.

But the system has to break at some point.

source: FCC