Vodafone’s recent moves to acquire cable operations Kabel Deutschland and Ono in Spain are a clear sign of the next escalation in product bundling.

Vodafone’s recent moves to acquire cable operations Kabel Deutschland and Ono in Spain are a clear sign of the next escalation in product bundling.

The acquisitions also indicate how competitive communications markets are in Europe, where total service provider revenues are dropping.

In competitive markets, where incumbents and multiple attackers each have substantial market share, it is unusual for any single service provider to have much more than 20 percent to 33 percent share.

Under such conditions, any single contestant might face the danger of stranded network assets as high as 80 percent, and commonly 66 percent. In other words, a service provider might have built network passing nearly 100 percent of locations, but generates revenue from a fraction of those homes.

There is much less risk when a competitor is able to use wholesale assets, but even then, competition tends to drive prices lower, affecting both gross revenue and profit margins.

Product bundling has a number of attractive features. Discrete prices are obscured, making it harder for consumers to focus on the prices of each product component. That tends to help blunt price-focused comparisons.

Consumers get an overall discount by buying in volume. Also, customer churn is reduced.

The quad play also allows contestants to take market share from other providers, though.

BT hopes the creation of a new quadruple play offer including Long Term Evolution mobile services, fixed network voice, video entertainment and high speed access will boost revenue per account and slow fixed network voice line churn rates.

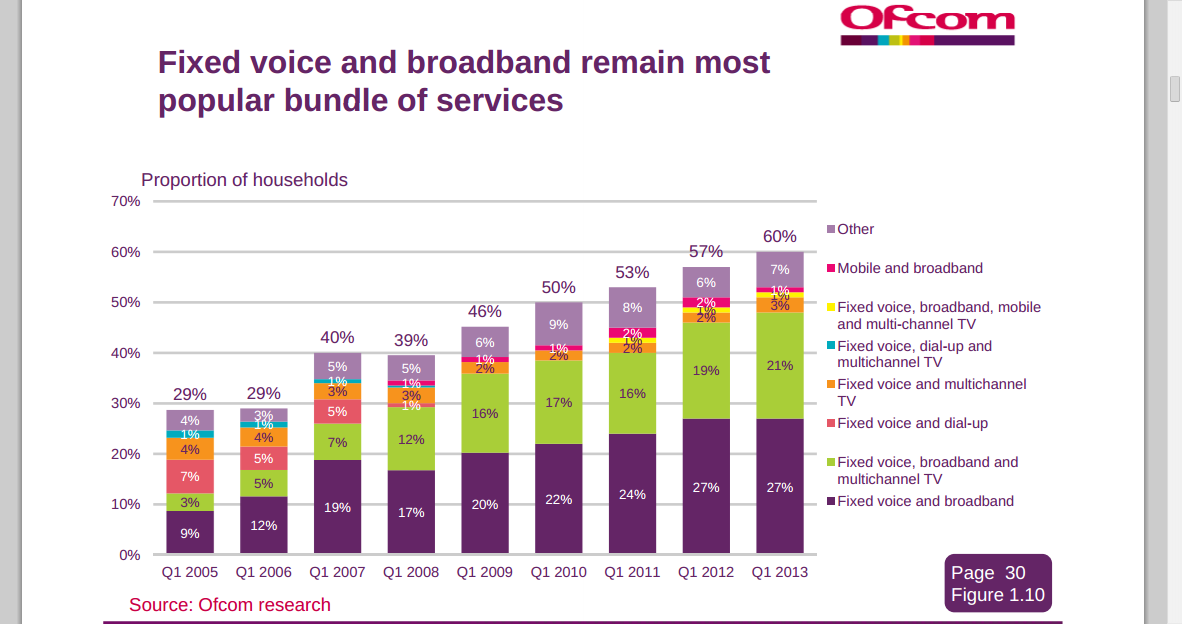

About 60 percent of U.K. consumers buy a bundle of some sort, often the two-product bundle of fixed network voice and high speed access, according to Ofcom, the U.K. communications regulator. Some 27 percent of U.K. households buying a bundle purchase the voice-plus-broadband package.

About 21 percent buy a triple play package including video entertainment as well as voice and high speed access.

Just three percent buy a quad play package, and those customers largely are Virgin Media (Liberty Global) customers, it appears. And that is the attraction for BT. Very low adoption of quad play packages suggests most of the market still is available.

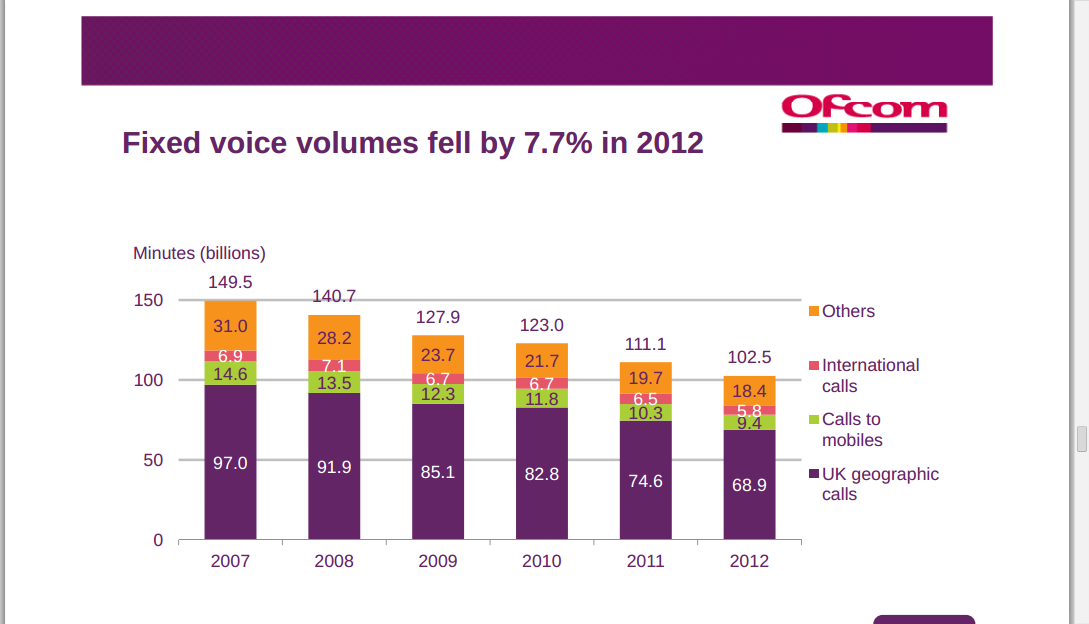

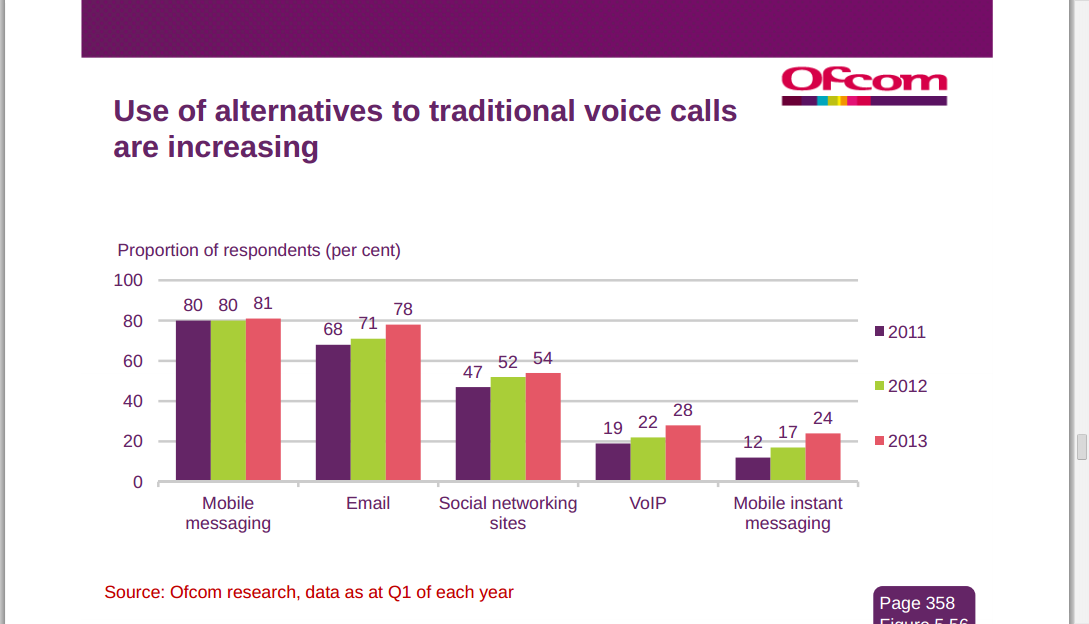

Between 2008 and 2012, fixed network call volumes have fallen 27 percent, according to Ofcom, with no real expectation the decline can be arrested. In fact, even mobile call volumes dipped in 2011 and 2012 as well.

In fact, it might be that 2010 was the peak year for mobile minutes of use, as 2000 was the peak year for U.S. access lines in service.

By some estimates, usage of fixed network voice has fallen as much as 50 percent in just the last six years, and might dip as much as 66 percent by 2020, representing a revenue loss of perhaps £600 million, according to the Financial Times.

If the quad play slows erosion of fixed lines, BT preserves some revenue it otherwise would have lost and gains additional time to grow the value of substitute businesses.

According to Chris Adams, Ofcom Head of Market Intelligence for Telecoms and Networks, the story for U.K. telecom includes declining revenues, lower call volume and fewer fixed lines in service.

According to Chris Adams, Ofcom Head of Market Intelligence for Telecoms and Networks, the story for U.K. telecom includes declining revenues, lower call volume and fewer fixed lines in service.

Total telecom revenue fell 1.8 percent in 2012, for example. But that has been the trend since at least 2007.

Also, the cost of a mobile-originated call now is lower than the cost of a fixed network originated call, which will drive more traffic to mobile, and off the fixed network.

Overall, the move to quad play offers is simple enough: if BT is going to have fewer customers, it has to sell more products to a smaller base of users.