To some extent, cable operators and many telcos have different strategic imperatives where it comes to high speed access services.

To some extent, cable operators and many telcos have different strategic imperatives where it comes to high speed access services.

For cable operators and telcos owning only fixed assets--not mobile--the network is the foundation for nearly 100 percent of revenue.

For telcos with significant mobile assets, the fixed network represents less than half of total revenue, and little of the revenue growth.

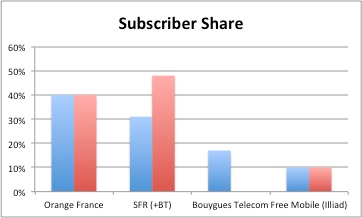

|

| source: High Speed Internet |

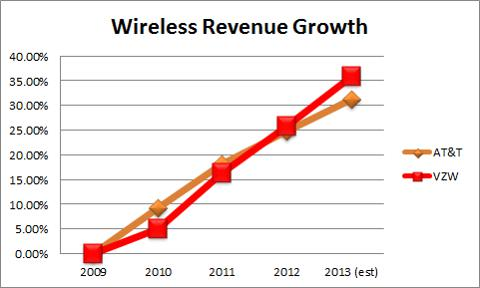

For AT&T and Verizon, mobile revenue has grown in the 30 percent annual range, in 2013.

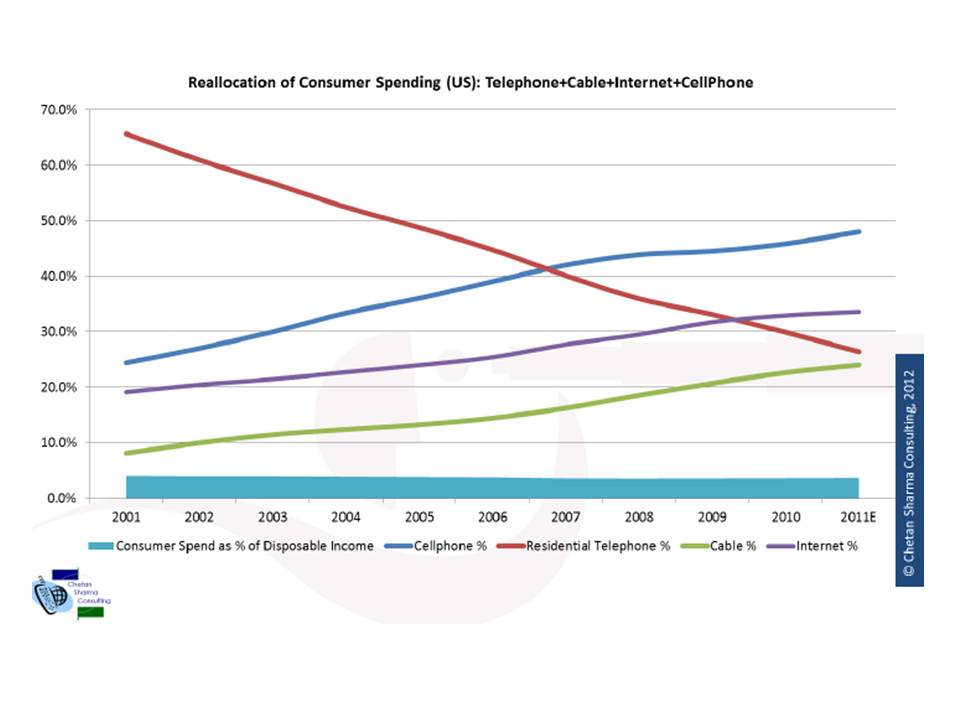

For AT&T, fixed network data services revenue (enterprise, small business and consumer) represents about 28 percent of total revenue.

In recent quarters, mobile has driven about 53 percent of revenue, and virtually all the growth.

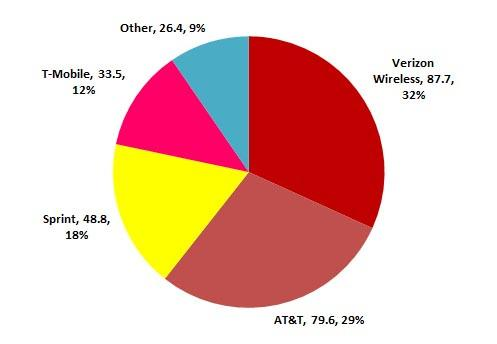

|

| source: High Speed Internet |

To be sure, the fixed network is becoming an important strategic asset for mobile service providers, as a way to supplement mobile data access.

Also, virtually everybody expects today’s linear video services to shift substantially to “over the top” delivery, which will add to the value of a high speed Internet access connection.

So the fixed network remains a substantial asset, even for firms such as Verizon and AT&T that earn the majority of their revenue, and nearly all the revenue growth, from mobile services.

Still, strategic considerations are key. Cable companies and fixed-only telcos must invest in their core asset.

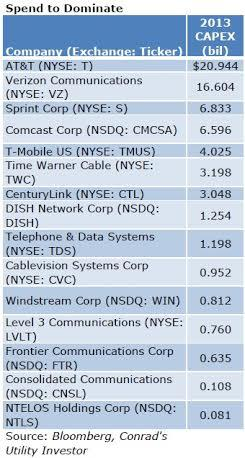

|

| source: Seeking Alpha |

Mobile-mostly service providers such as Verizon and AT&T, and mobile-only providers such as Sprint and T-Mobile, have to weigh the returns from investing in mobile, versus fixed access.

So it is that Verizon, which made a big bet on FiOS, has concluded it must presently avoid several new big city builds, as the financial returns are not deemed adequate.

AT&T, on the other hand, has stepped up the pace of its U-Verse builds, and even is upgrading some areas for gigabit access, in response to competition from Google Fiber.

|

| source: IP Carrier |

But the strategic imperatives are matched by results on the ground.

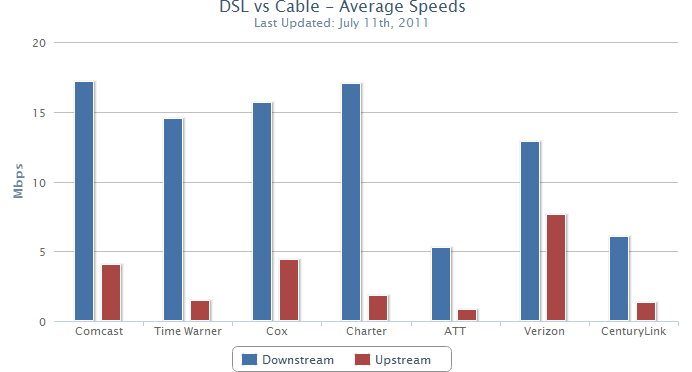

Since about 2009, cable high speed access has pulled away from digital subscriber line, in terms of top speed. The Docsis 3.0 standard supports top downstream speeds of about 105 Mbps. AT&T’s U-Verse (fiber to a neighborhood with copper drops) can achieve about 24 Mbps.

To be sure, telcos can install very high speed DSL or fiber to the home. At the moment, though, telcos are losing DSL customers faster than they are gaining subscribers for their faster broadband offerings.

During the second quarter of 2012, for example, cable companies took a 140 percent share of broadband new additions, according to UBS Research telecom analyst John Hodulik.

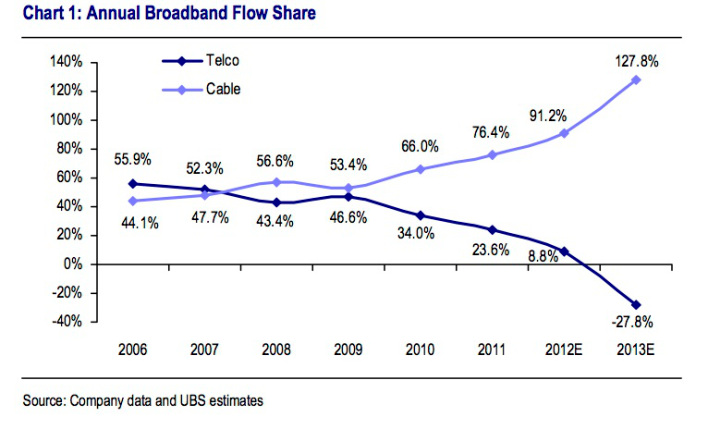

|

source: Seeking Alpha

|

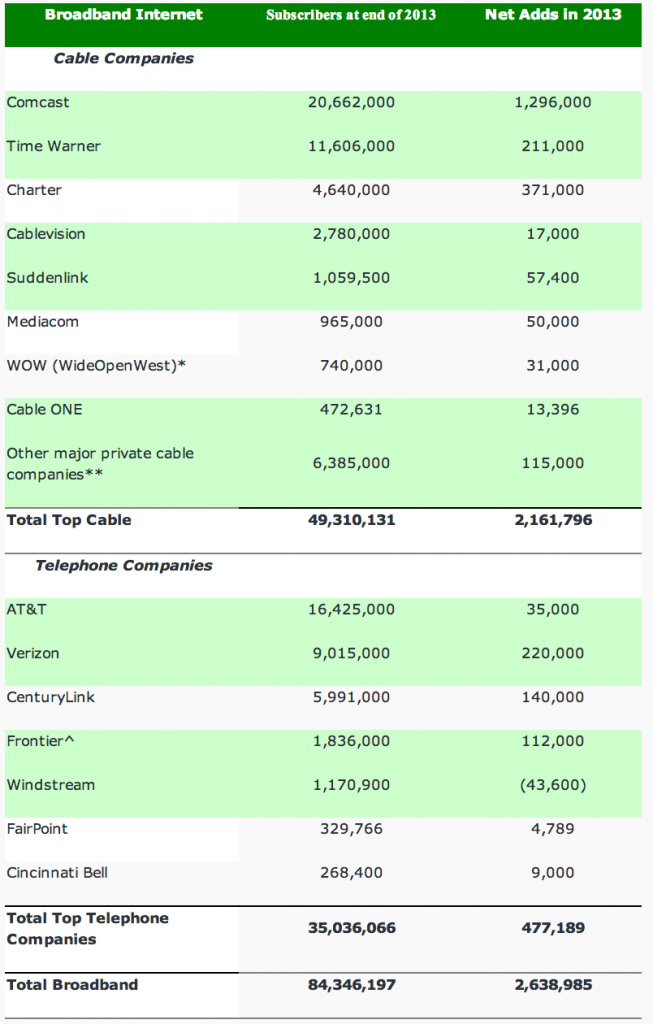

In fact, cable high speed net additions are soundly outpacing telco net additions. In 2013, for example, the top cable companies added a net 2.2 million high speed access connections, compared to 477,000 for top telcos.

Just how much telcos must invest--and where--is the issue. Fixed network operators, without mobile assets, have to invest to stay competitive, or risk losing their businesses.

AT&T and Verizon have to balance investment between the mobile and fixed segments. So for cable, investments in high speed access--as is the case for Google Fiber--are offensive in nature, designed to take market share.

For many telcos, such investments largely are defensive, intended mostly to protect market share.