It's only one anecdote, but one does wonder whether incentives for "saving" an account could have something to do with what many could say is an overly-aggressive effort by one Comcast CSR to save an account, when the customer wanted to halt service.

Few might consider the call a pleasant experience.

I had the diametrical opposite experience recently when changing service levels for my mom's Verizon FioS video account. I needed to downgrade one premium video service and also end purchase of a backup and security service for the Internet access account.

The former downgrade was because she doesn't watch so much TV, and certainly was not watching the premium service. The latter downgrade was because, after moving mom to a Chromebook, the online backup and security package simply was unnecessary.

I got everything done, right away, on the Verizon website, with no need to make a call, talk to a customer service representative and endure the "save the revenue" script I suspect I'd otherwise have encountered.

To be sure, Verizon's customer-friendly approach to online downgrades meant Verizon did not have one more shot at avoiding the two downgrades.

On the other hand, I appreciated the chance to quickly and easily accomplish a service level change without grief.

Perhaps one should not conclude too much from just a couple of customer interactions with a major service provider.

But it also is hard not to wonder whether a different approach is at work in these two instances.

I probably am not the only potential customer, or existing customer, who has encountered what appears to be a deliberate effort by a service provider to make dropping or downgrading more difficult.

Tuesday, July 15, 2014

"Customer Surly" and "Customer Friendly" Service: 2 Anecdotes

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Can 5G Erase Difference Between Mobile and Fixed?

Though it is early to specify what characteristics future fifth generation (5G) mobile networks will feature, at least some think 5G will be the first next-generation mobile network with a specific applications focus and the first mobile platform that erases performance differences with the fixed networks.

Those are among some of the conclusions one might draw from the 5G “Public Private Partnership,” a new European 5G initiative.

Ironically, given the amount of present argument advanced about the need for maintaining “best effort only” access (no packet prioritization), the 5G PPP document also notes the “future challenge will be to guarantee and continuously improve customer experience offered by cloud-based services.”

“Such experience relies on the end-to-end QoS, and more generally on respective SLAs in place for a given service,” the document notes.

So there, once again, you have the inherent tension between “best effort only” access and “quality of service,” which in the 5G PPP document explicitly indicates that QoS mechanisms are necessary to ensure good end user experience.

There are, to be sure, many ways to enhance experience at the end user level. But “admission control” always has been a feature of public networks that must share key resources, and can become congested at peak hours of use.

Among other key 5G objectives is a mobile network with three orders of magnitude more capacity than was typical in 2010.

Another angle is that the 5G PPP envisions devices connecting with multiple networks over time, and possibly more than one network at any moment, meaning there will be more orchestration of access.

Whether that enhances, degrades or is neutral with respect to the “value” of networks, and how such orchestration affects the “commodity access” or “dumb pipe” position of access networks also is unclear.

Though 5G would not be the first next-generation mobile network to enable new apps, 5G arguably will be the first such network built with a specific category of applications in mind.

In some ways more dramatic, at least some observers predict 5G also will erase the distinction between “fixed” and “mobile” networks, with “capabilities and performances of mobile networks becoming similar to those of fixed networks in terms of capacity and services diversity,” argues the 5G “Public Private Partnership” a new European 5G initiative.

That might sound fanciful, were it not the case that small cells, carrier and other Wi-Fi resources, ideally, will allow devices to interwork seamlessly, erasing, from a user standpoint, the difference between “using a fixed network and using a mobile network.”

Essentially, all those techniques shift bandwidth demand from “mobile” to “fixed” access.

The other change is the deliberate architecting of network standards to support both machine-to-machine apps (Internet of Things) and person-to-person communications.

5G will be about the Internet of Things, argues Neelie Kroes, European Commission VP. If that prediction turns out to be correct, 5G will be the first next-generation mobile network defined by applications, not just air interfaces and bandwidth.

“It will also offer totally new possibilities to connect people, and also things, being cars,

houses, energy infrastructures,” Kroes argues. “All of them at once, wherever you and they are."

One might argue those sorts of comments also are part of a political agenda. Perhaps oddly, the mobile infrastructure business now is lead by European and Chinese firms. So initiatives related to 5G arguably are part of an effort to keep Europe at the forefront of mobile infrastructure businesses in the future.

On the other hand, initiatives such as the 5G “Public Private Partnership” also speaks to a fear that Europe fell behind in 4G device and application innovation and leadership.

And, as always, the positive impact on economic growth and jobs are part of the rationale for pushing ahead in 5G.

The document also notes why mobile data is at the heart of the proposed 5G architecture.

Within Europe, “revenue from mobile data services compensates for the declines in total spending for both the fixed and mobile voice services markets,” the group says.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, July 14, 2014

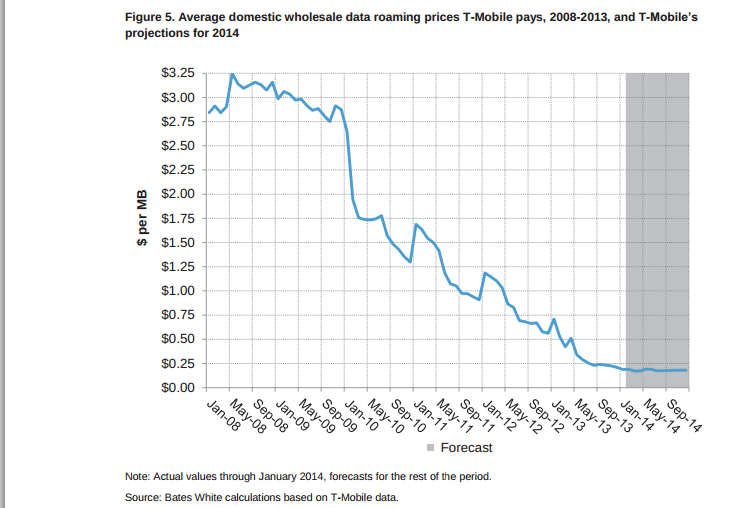

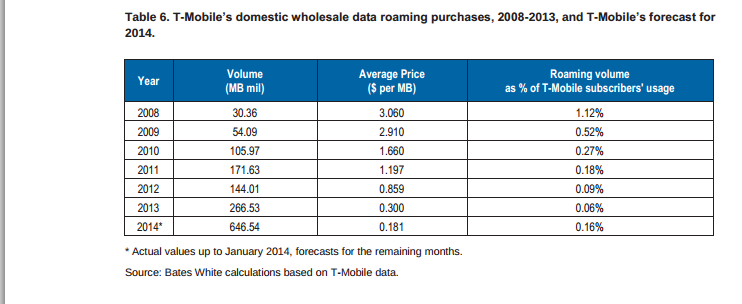

T-Mobile US Wants Lower Mobile Data Roaming Costs

In Europe, mobile wholesale voice and data roaming rates have been lowered by action of the European Commission. In the United States, at least according to T-Mobile US, mobile data roaming rates likewise are dropping.

In Europe, mobile wholesale voice and data roaming rates have been lowered by action of the European Commission. In the United States, at least according to T-Mobile US, mobile data roaming rates likewise are dropping.

And T-Mobile US wants the Federal Communications Commission to take action to drop mobile data roaming rates T-Mobile US pays to AT&T or other service providers able to support GSM roaming.

To be sure, data roaming represents only about 0.16 percent of T-Mobile US customer data usage.

But smaller service providers typically argue they pay roaming rates that are too high, in large part because smaller networks nearly always pay more in roaming fees than larger networks pay to smaller networks.

But smaller service providers typically argue they pay roaming rates that are too high, in large part because smaller networks nearly always pay more in roaming fees than larger networks pay to smaller networks.  Scale is the reason: most calls or instances of roaming will occur when smaller network customers roam onto larger networks, simply because the larger networks represent most of the customers who communicate.

Scale is the reason: most calls or instances of roaming will occur when smaller network customers roam onto larger networks, simply because the larger networks represent most of the customers who communicate.

Larger numbers of customers also mean lower likelihood a big network’s customers will need to access a roaming network, simply because there is a greater likelihood a called or connected party is “on network.”

AT&T has a bigger deployed network than T-Mobile US. So AT&T customers arguably will need to roam less frequently off the core AT&T network when traveling.

With a smaller network, T-Mobile US customers are more likely to need to roam onto AT&T’s networks when traveling.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Devices a Smartphone Replaces

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

For Every Public Purpose, There is a Corresponding Private Interest

Who pays for Internet access? Consumers and businesses.

But advertisers or sponsors might pay on behalf of users of their services. Internet service providers might sponsor use of some applications.

In some cases, application providers pay, on behalf of their customers.

But mostly, it is end users who pay all the costs.

And though it is true that there are genuine policy issues surrounding a seemingly-endless list of "network neutrality" instances, there also are important commercial interests.

For access providers, the issue is whether apps that impose disproportionate network costs should help defray the direct costs they impose.

For application providers, the issue is avoiding such costs, as they would directly affect app provider business models.

And as the Internet has fragmented, there now are different kinds of Internet domains. The sort people generally are familiar with are Internet service providers who provide mobile or fixed network access. Those "eyeball" networks aggregate end users.

Content domains are different, especially domains that supply video entertainment or video content. Such domains represent the majority of all demand on access networks.

To the extent that ISP eyeball networks have to supply additional capacity to support such apps, the costs now are borne exclusively by end users, in the form of higher access fees.

The issue is whether dual revenue streams will develop that resemble the way much print, TV and audio content is subsidized by advertisers.

That notion is contentious as a matter of public policy. But the differences also reflect very real business models, and revenue and cost winners and losers in the internet ecosystem.

As always is the case, for every public purpose there is a corresponding private interest. Proponents never directly say so. But it always is there.

But advertisers or sponsors might pay on behalf of users of their services. Internet service providers might sponsor use of some applications.

In some cases, application providers pay, on behalf of their customers.

But mostly, it is end users who pay all the costs.

And though it is true that there are genuine policy issues surrounding a seemingly-endless list of "network neutrality" instances, there also are important commercial interests.

For access providers, the issue is whether apps that impose disproportionate network costs should help defray the direct costs they impose.

For application providers, the issue is avoiding such costs, as they would directly affect app provider business models.

And as the Internet has fragmented, there now are different kinds of Internet domains. The sort people generally are familiar with are Internet service providers who provide mobile or fixed network access. Those "eyeball" networks aggregate end users.

Content domains are different, especially domains that supply video entertainment or video content. Such domains represent the majority of all demand on access networks.

To the extent that ISP eyeball networks have to supply additional capacity to support such apps, the costs now are borne exclusively by end users, in the form of higher access fees.

The issue is whether dual revenue streams will develop that resemble the way much print, TV and audio content is subsidized by advertisers.

That notion is contentious as a matter of public policy. But the differences also reflect very real business models, and revenue and cost winners and losers in the internet ecosystem.

As always is the case, for every public purpose there is a corresponding private interest. Proponents never directly say so. But it always is there.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Which Analogy for ISP Interconnection: Retransmission or Carrier Interconnection?

Netflix and major U.S. ISPs use different metaphors to describe the process of interconnecting Internet domains.

Verizon, AT&T and Comcast, for example, use the analogy of carrier interconnection, where the amount of traffic exchanged determines whether any particular bilateral interconnection is settlement free (roughly equal amounts of traffic exchanged) or requires payment by the network delivering much more traffic than that network is accepting.

Netflix uses a different analogy, that of broadcast TV "retransmission fees," the fees paid by video subscription services to TV broadcasters for the rights to retransmit off-air signals as part of a video subscription.

Whatever one thinks of the reasonablenes of those analogies, there now is a huge traffic imbalance between "eyeball networks" that terminate Internet traffic for consumers, and "content networks" that deliver traffic to eyeball networks, but accept only modest traffic from the eyeball networks back to the content networks.

The reason is simple enough: content networks send video and other content to end users, but generally do not need to accept much upstream traffic from consumers, whose operations are generally confined to ordering a movie to watch or updating a play list.

Verizon, AT&T and Comcast, for example, use the analogy of carrier interconnection, where the amount of traffic exchanged determines whether any particular bilateral interconnection is settlement free (roughly equal amounts of traffic exchanged) or requires payment by the network delivering much more traffic than that network is accepting.

Netflix uses a different analogy, that of broadcast TV "retransmission fees," the fees paid by video subscription services to TV broadcasters for the rights to retransmit off-air signals as part of a video subscription.

Whatever one thinks of the reasonablenes of those analogies, there now is a huge traffic imbalance between "eyeball networks" that terminate Internet traffic for consumers, and "content networks" that deliver traffic to eyeball networks, but accept only modest traffic from the eyeball networks back to the content networks.

The reason is simple enough: content networks send video and other content to end users, but generally do not need to accept much upstream traffic from consumers, whose operations are generally confined to ordering a movie to watch or updating a play list.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"Opportunity Cost" Might be the Biggest Downside to "Upgrading" Existing Product Lines

Marginal cost has proven to be a key concept for products sold in most mass markets, and telecommunications is not exempt from that trend.

Any number of retail prices and packages are set basically to reflect the marginal cost of adding the next incremental customer. In fact, over time, economists might argue, current retail costs for goods and services tend to move towards marginal cost.

The concept has lots of relevance in telecommunications, where large amounts of capital investment are “sunk,” and incremental usage actually imposes little additional operating cost.

The traditional way of illustrating the principle is to answer the question “how much does adding one more minute of use of the voice network cost?” In practice, the cost is almost solely limited to the cost of adding one more transaction on a billing system.

In the Internet era, we are accustomed to the notion that the next increment of usage of any consumer app actually costs the suppliers almost nothing.

In most cases, that next increment of usage costs the end user almost nothing, as well. You of course know the business problem thus created. When costs are nearly zero, retail price will tend to move towards zero as well.

As useful as that is for consumers, it is a huge problem for communications suppliers. Very low marginal cost explains why VoIP and messaging providers are able to offer their services literally for free, or nearly for free.

Low marginal cost is the foundation for the business model known as “freemium.”

Low marginal cost explains why suppliers of long distance calling, facing declining margins, try to compensate by encouraging additional usage volume.

And low marginal cost will be the reason why gigabit access services costing only $70 to $80 a month are possible, in large part.

Observers offer any number of suggestions to service providers about how to sustain their businesses under conditions where retail pricing for many products drops to marginal cost, and when marginal cost is quite low.

Many of those suggestions, though sound enough, have problems. Solutions that call for adding more value to existing products assume users will value the incremental new value enough to pay incrementally more revenue.

Strategies that call for creating new lines of business face execution risk (can telcos really do it?) as well as scale risk (will the new revenue streams be big enough to justify the effort?).

Assuming that creating new lines of business is both essential and realistic, the subsidiary issue then is how much to continue investing in legacy businesses that are declining in absolute value.

Two fundamental approaches can be taken: harvest or invest. The former essentially admits a business is mature, and will decline. The objective then is to preserve the magnitude of the revenue stream as long as possible, at the highest level possible.

The latter calls for spending more money to upgrade products, adding enough value that prices and usage can be sustained, or hopefully that usage and prices can even raised.

Low marginal cost might suggest harvesting is the more realistic strategy for most service providers. Adding more value might be capital and human capital intensive enough that the net result is a negative number.

Some of us would argue that if a given product line is powerfully affected by low marginal cost, the wiser choice is harvesting. The upside from big, or even significant investments, might not be large enough to justify the cost, time and human effort.

“Opportunity cost,” effort that might have gone elsewhere, also is a concern. No matter how large, organizations only have so much ability to invest in brand-new lines of business and revenue streams.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...