Sometimes, service providers make strategic investments not strictly related to "return on invested capital." That might seem irrational. It is not.

Large or small, fixed network telcos continue to face very-tough decisions about high speed access. For several decades, telco planners have modeled financial returns from fiber-to-home projects and generally have faced a hard reality.

In most cases, though such investment often has to be justified for strategic reasons, the financial return often is difficult and tenuous. Verizon Communications, for example, has in the past argued that a significant portion of the return comes not from the ability to offer new services, but from reduced operating expenses.

One might conclude Verizon no longer believes the expected maintenance savings are as great as were originally expected. In 2010, Verizon’s suspended its FiOS program in major metro areas where it had not already begun construction. In 2014, Verizon executives said they would consider expanding FiOS deployments when doing so would recover the cost of capital committed to the effort.

In other words, FiOS probably does not return its cost of capital in many markets.

To be sure, there are other considerations. Verizon and AT&T now drive revenue growth from the mobile business, so returns on invested capital are much higher when available capital is invested in the mobile business.

In the first quarter of 2014, Verizon operating income for the mobile segment was an order of magnitude higher than for the fixed line business.

In the third quarter of 2014, mobile segment operating income margin was 31.9 percent and segment earnings (EBITDA) margin on service revenues was 49.5 percent.

Compare that performance with results from the fixed network segment.

Fixed network operating income margin was 2.3 percent in the third quarter of 2014, up from 1.5 percent in third-quarter 2013. So mobile operating income margin was an order of magnitude higher than fixed network operating income margin.

Smaller telcos without mobile assets will not have the option of directly available capital to the mobile network.

So the decision about investing in fiber-to-home facilities remains a challenge. Cincinnati Bell, for example, sold its mobile business and half of its data center business to raise capital to build its “Fioptics” fiber-to-home network.

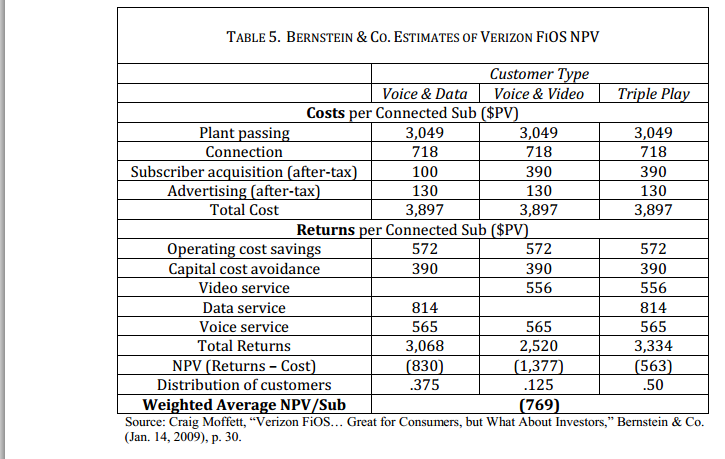

Analyst Craig Moffett of Bernstein and Company estimated in 2009 that Verizon’s cost per subscriber was about $4,000, while estimating the expected revenue from a FiOS-connected household was just $3,200.

Though network element costs arguably have declined since then, the business case remains challenging. So why do telcos move ahead? There are strategic reasons. Unless a fixed network telco upgrades, it might be unable to compete with cable TV operators.

Simply, the investment in fiber-to-home has to be made so “you get to keep your business,” as one executive said. Strict return on capital considerations are secondary.

Sometimes a business decision has to be made for reasons other than strict return on invested capital grounds. Investment in gigabit networks would appear to be such a decision.

|

| Source: Craig Moffett, Bernstein & Co. |