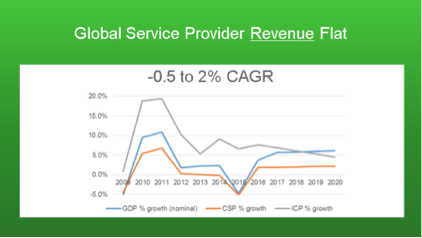

No market ever grows to the sky, financial analysts sometimes quip, while maturing markets often see competitive pressures that lead to price cuts and thinner profit margins.

The reason is simple enough: in a mature market, new accounts generally must be taken from other existing providers. These days, saturation and new competition can come rather suddenly.

As important as mobile services have been over the past couple of decades as the single most-important driver of service provider revenue growth, big changes are happening. Globally, subscriber growth has flattened.

In many markets, the immediate revenue growth opportunity is incremental data services revenue. Beyond that, similar big new sources remain to be discovered, which is why there is so much attention paid to the Internet of Things.

If sales to humans are saturated, then the next big wave of growth might well come from sales to enterprises who require huge sensor and control networks, or sell retail mass market products using such sensor capability.

Of course, new competition--in addition to the underlying price-per-megabyte price drops that are characteristic of chip-based products--can disrupt even data markets that are relatively early in their growth cycles.

Reliance Jio's launch of 4G services in 2016 could disrupt data pricing in the Indian mobile service provider market, causing revenue-per-megabyte to tumble 30 percent to 40 percent this year, according to the India Ratings and Research (Ind-Ra).

To be sure, lower revenue-per-megabyte is a fundamental trend in the transport and access business, so a decline is not unexpected. Only the magnitude is unusual, for a one-year period.

At the same time, given expected lower prices, data services average revenue per user also will decline, although the number of accounts should increase, while data consumption also climbs, over time.

Revenue per megabyte declined by 4.5 percent to 5.5 percent, sequentially, in the third quarter, for Bharti Airtel and Idea Cellular.

Ind-Ra believes expects a further softening of data tariffs in the current year of perhaps negative eight percent to 10 percent.

Those are among the least controversial observations that could be made about Reliance Jio’s entry into the Indian mobile services market.

India Ratings and Research (Ind-Ra) “expects the launch of Reliance Jio Infocomm Limited (RJio) to intensify competition which will squeeze the market share, EBITDA margins and credit metrics of incumbents.”

At the same time, debt burdens will increase, as competitors and Reliance Jio itself invest heavily in their networks and spectrum.

Ind-Ra also expects voice revenue to decline. Airtel and Idea reduced voice tariffs by eight percent to 10 percent last year.

Those changes could come even as growth in the often red hot smartphone market is slowing globally, for example.

Even if India is predicted to become the world’s second-largest smartphone market by about 2017, trailing only China, India smartphone growth rates to 2017 will drop from 47 percent in 2015 to about 17 percent in 2017, according to Strategy Analytics.