It’s hard to have fruitful discussions when we do not agree on the “facts” of the matter at hand. So it is with the amount of capital investment in access networks in the wake of regulation of such investments under common carrier rules.

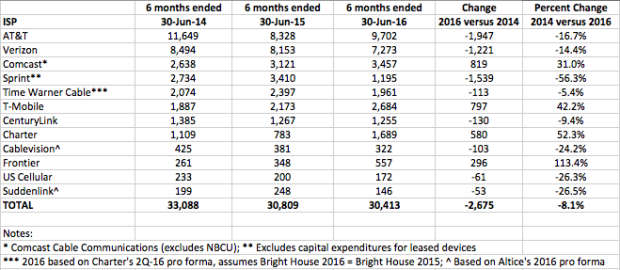

According to economist Hal Singer, common carrier regulation has depressed investment, even if many claim the reverse to be true. Singer compares the first six months of 2016 with the same period in 2014, the last year in which ISPs were not subject to Title II regulation, and finds a decline of eight percent.

http://marketrealist.com/2015/01/key-costs-wireless-wired-telecom/

http://marketrealist.com/2015/01/key-costs-wireless-wired-telecom/

Still, it is not a simple matter to determine the specific impact of the rules, as distinct from background economic factors or changes in company strategies. Generally speaking, big economic shocks (the popping of the internet bubble in 2000 and the Great Recession of 2008) will drive capex declines.

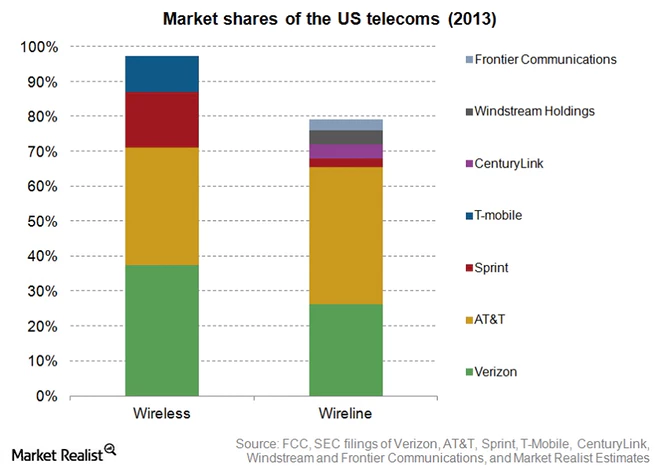

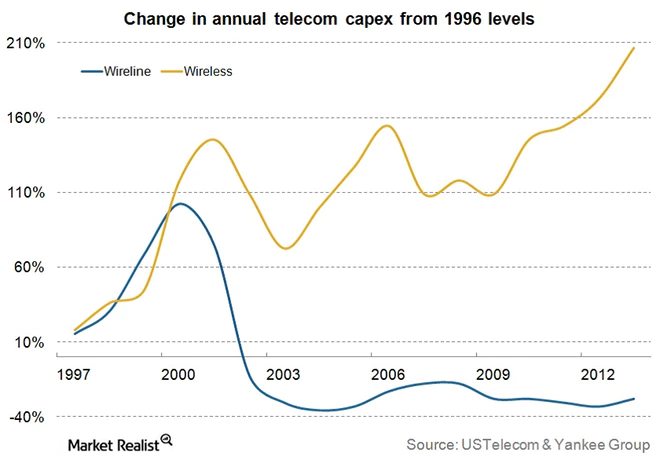

Also, it is an undeniable fact that most U.S. telcos have shifted capex to mobility, and away from the fixed networks, so that is another factor. Prior to imposition of the rules, fixed network capital investment had dropped very sharply from 2000 peak levels.

Conversely, mobile networks clearly were the drivers of firm revenue growth since 2000, and saw generally higher investments, especially compared to fixed network investment.

You can see that telcos generally spent less, while cable companies spent more. In fact, those who argue that common carrier regulation did not depress investment invariably point to higher levels of investment by cable companies.

You might argue that flows form a correct understanding that those investments would generate incremental revenue for cable companies and a similar understanding by telcos that even high investment would not produce favorable financial returns. In fact, those simple understandings largely would account for high cable investment and low telco investment, for basic reasons related to return on investment.

It still remains difficult to say what might have happened, in terms of telco investment, if telcos had seen much higher revenues from doing so.

You might argue that flows form a correct understanding that those investments would generate incremental revenue for cable companies and a similar understanding by telcos that even high investment would not produce favorable financial returns. In fact, those simple understandings largely would account for high cable investment and low telco investment, for basic reasons related to return on investment.

It still remains difficult to say what might have happened, in terms of telco investment, if telcos had seen much higher revenues from doing so.

“Aggregate capital expenditure (capex) declined by nearly $2.7 billion relative to the same period in 2014,” Singer argues.

While Title II can’t be blamed for all of the capex decline, it is reasonable to attribute some portion to the FCC’s rules, he argues.

The rules bar ISPs from creating new revenue streams from content providers, and (needlessly) expose ISPs to price controls, Singer argues. Both measures truncate an ISP’s return on investment, which makes investment less attractive at the margin he argues.