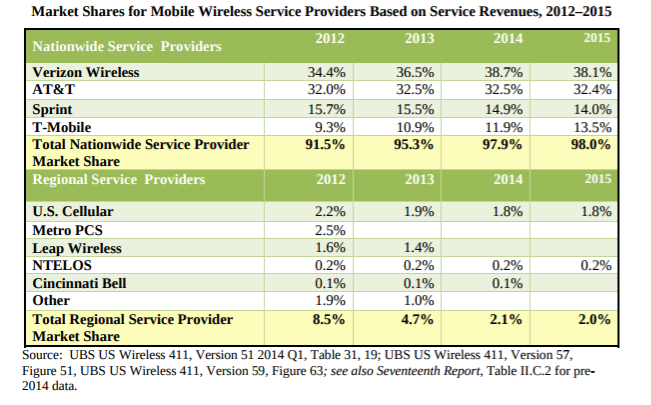

It likely still is true that the top four U.S. mobile service providers have about 98 percent market share.

Perhaps just as significant, from a market structure perspective, is the way antitrust regulators typically quantify the conditions that suggest a market is “concentrated,” which is a warning sign about the potential competitive impact of market consolidation.

This already has been an issue twice in the last decade regarding consolidation among the top-four providers, and obviously there is talk between Sprint and T-Mobile US about trying again, for a third time in a decade, to consolidate the ranks of the leaders from four to three.

Some believe a change of presidency is going to mean better prospects for any such effort. By most accounts, the U.S. mobile market has been “highly concentrated,” using the Department of Justice methodology, since 2005, and has grown more concentrated over the last decade.

So the issue, in the U.S. and many other markets, is what regulators believe is necessary to sustain competition. By definition, any combination of Sprint and T-Mobile US makes the U.S. market more concentrated.

There is an argument that more concentration can lead to more competition, though that clearly is not what virtually all analysts looking at the matter seem to believe. The reason equity analysts generally are in favor of such a merger is that it strengthens pricing power and reduces competition.

Since that leads to an ability to raise prices, consolidation arguably strengthens all the surviving three firms for the long term. In that view, higher profits for the survivors ensures survival, and therefore three leaders, not a duopoly.

Though some argue that the new merged Sprint-T-Mobile US would be in better position to challenge Verizon and AT&T more vigorously, there is an equally-strong case to be made that a stronger Sprint-plus-T-Mobile US would not want to rock the boat, and would back off its challenges.

That can--and arguably does happen--in stable markets because it is deemed advantageous to maintain the stability of a market that deters new attackers but also allows reasonable margins for each of the top-three providers.

Logically, even in that scenario, having three choices is better than having just two choices.

And, in the U.S. market, it is possible that a relatively-stable duopoly in the fixed network business still has delivered significant consumer benefit. So it cannot be dismissed, out of hand, that a three-provider market representing 98 percent market share would still deliver some competitive benefits, and possibly could work as well as the fixed network duopoly.

But it is hard to say what actually would happen. Optimists might point to market entry by the likes of Comcast, Charter and other cable companies, plus other forays by new entities with different business models that could provide new competition.

Pessimists will point to the low degree of consumer benefit under the old duopoly conditions before Sprint and others entered the market using 2-GHz spectrum.

Optimists will point to T-Mobile US success as an example of what might happen in a three-leader market.

Some might say that, yes, there will be less competition in a three-provider market, but that this is required to maintain profitable competition, rather than ruinous competition. Some might point to Sprint’s “nn-profitable” status as an example that four profitable providers are not possible in the U.S. market.

The rejoinder is that there are other ways to envision a stronger mobile market that still has four providers, including participation by Comcast or even other new owners with different business models, able to bring new assets to bear.

It is hard to say what might be allowed. But the U.S. mobile market will continue to be deemed “highly concentrated” by antitrust authorities, that much is clear.