Artificial intelligence, edge computing, cloud computing, gigabit mobile networks (5G and others), internet of things and big data all are key trends across many industries.

What we tend to miss, as so much change is happening, is simply that so much change is coming. It is better to view the cluster of innovations as the big change, and not so much the disruption each separate trend represents.

For it is the cluster of technologies that is so unusual. In the past, it has been easier to model the impact of a single innovation (personal computer, mobile phone, internet). It will be much harder in the coming era, since so many fundamentally disruptive technologies are emerging at the same time.

Big data now requires cloud computing. Big data will get bigger as internet of things sensors are widely deployed. So only artificial intelligence can sift through all the data to discern useful patterns.

And some of that data will have to be analyzed fast enough that edge computing is necessary. But 5G and other connectivity solutions will be needed to acquire all the data.

It is nearly impossible for a human to model all the possible interactions with enough detail to make the output useful. From a mobile operator’s point of view, it might be logical to put 5G at the center.

Other industries are going to put AI, or cloud, or IoT or big data at the center. No matter. The point is that the cluster of technologies is what really matters, not any single one of the technology trends.

In this unusual situation, impact will not be measured by market share stats. The percentage of work loads, the location of work load processing, the number of sensors and connections, the use of analytics and machine learning systems will fail to tell the full story.

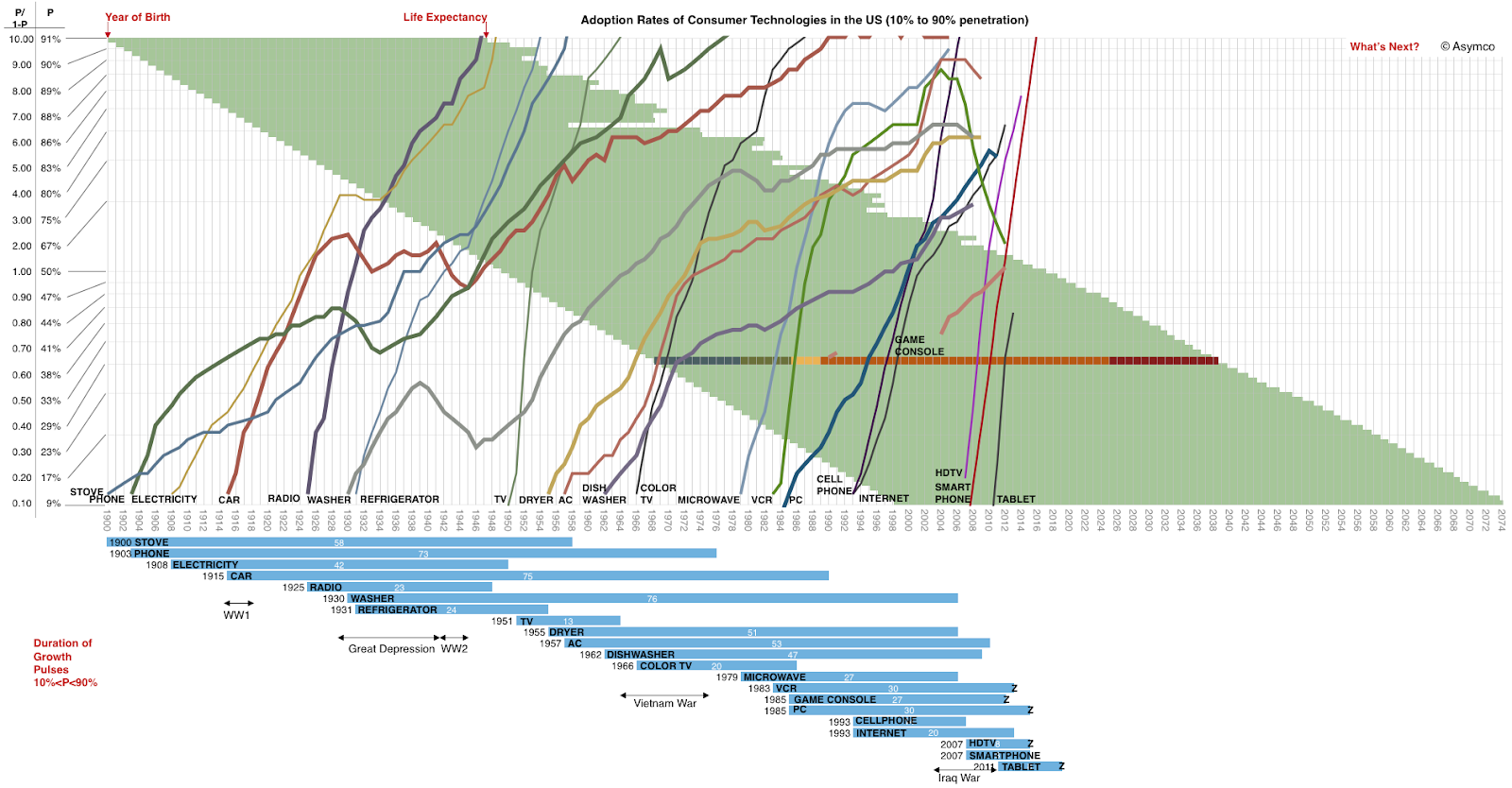

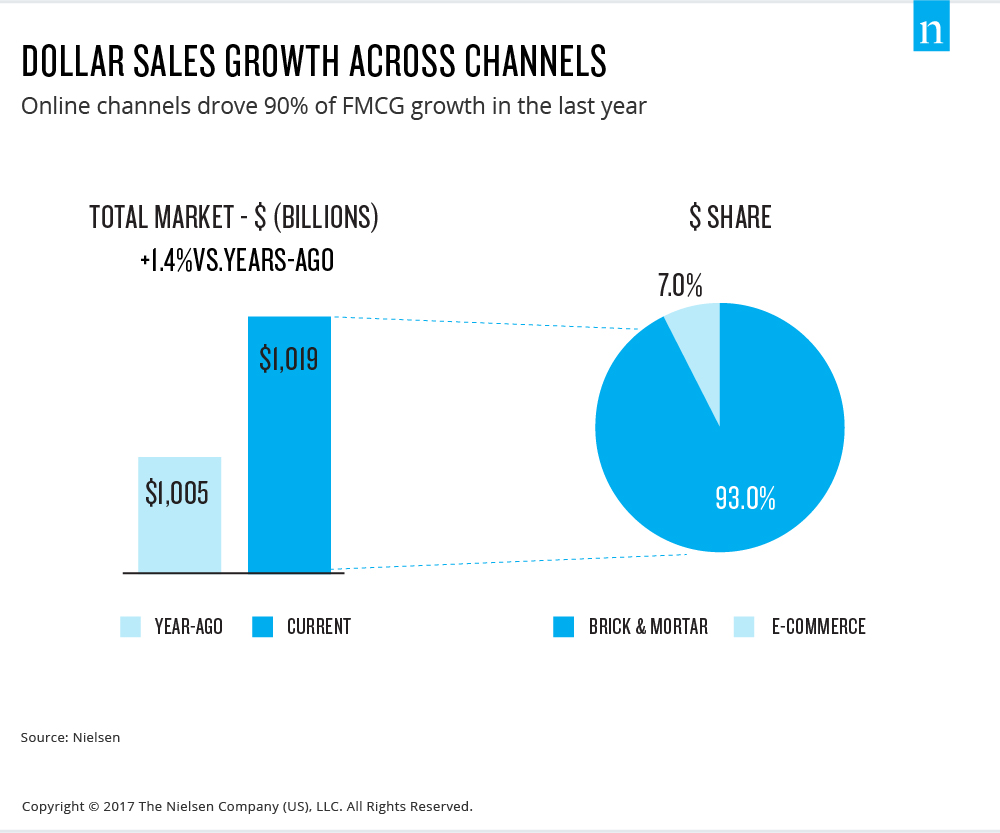

As useful as market share analysis might be, it fails to capture the underlying market dynamics when a disruption is underway. Consider that, after nearly two decades, online commerce claims only about seven percent of total retail commerce volume.

Most of us, asked to evaluate the potential impact of a substitute technology platform that has gotten only seven percent share after nearly two decades would likely say that technology is not a major disruptor of the legacy platform.

But we would be quite wrong. If history is a useful guide, we are about three share points away from a decisive change in the adoption rate--and market share--of the new platform.

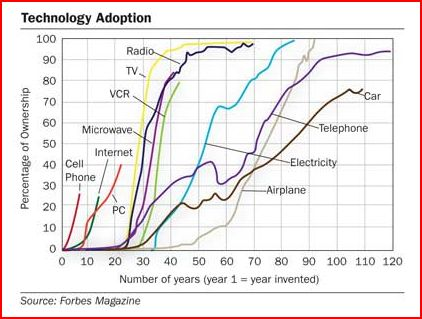

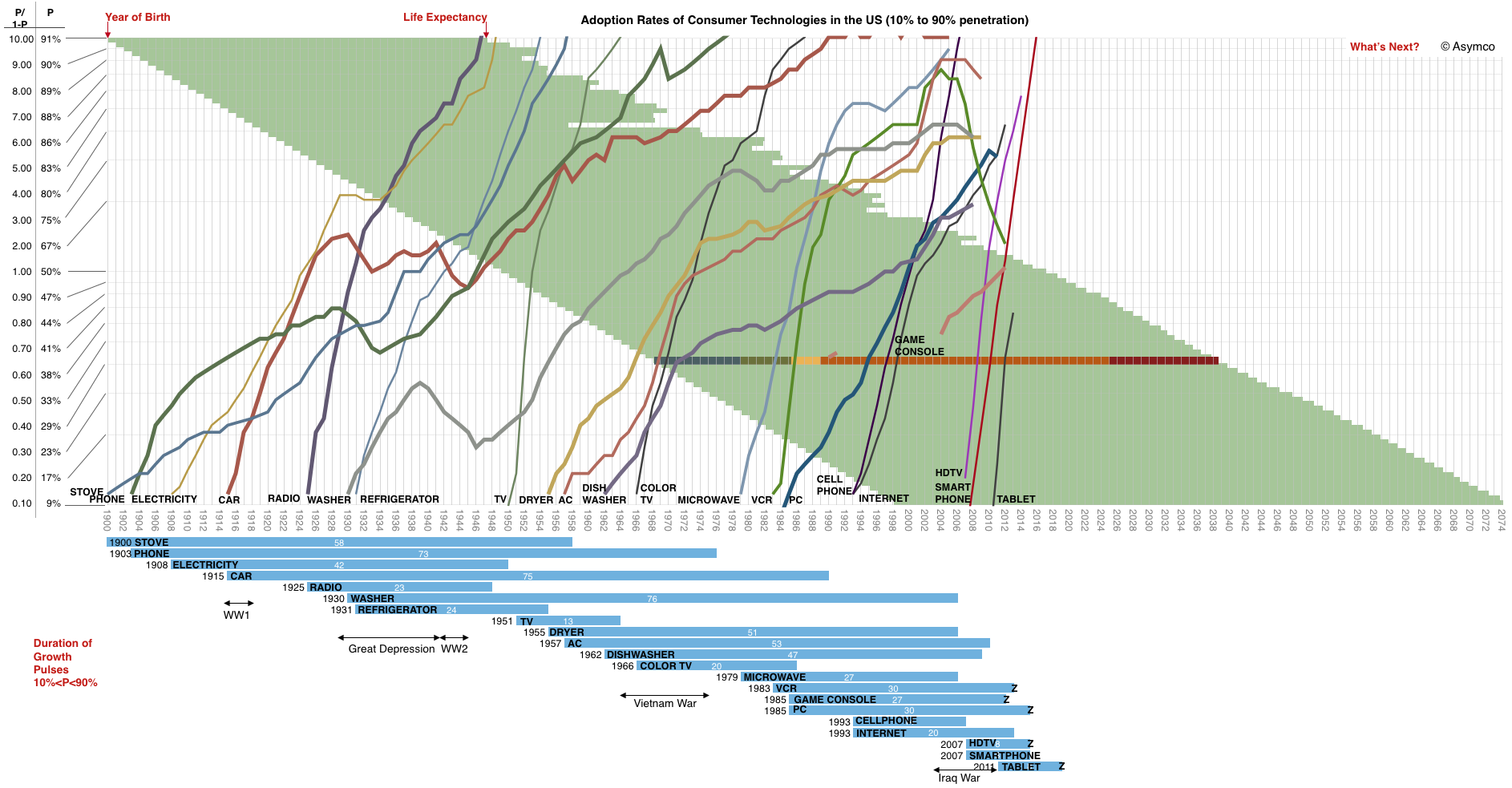

The reason for that assertion is that, in the past, transformative technologies and successful consumer electronics innovations hit an inflection point at 10 percent adoption, no matter how incremental the prior moves had seemed.

This chart by Asymco shows adoption rates of popular consumer products after 10 percent adoption was reached, no matter how long the gestation.

As you probably would expect, particular products introduced into developed ecosystems tend to be adopted faster, while products that require further development of an ecosystem can take longer to reach 10-percent adoption rates. Automobiles required a huge infrastructure of roads and gas stations.

The telephone required network economics, as the value of having a phone line was fairly low, for most users, when few other people had them. Likewise, supplying electricity required power plants and transmission lines, plus local power distribution networks.

And though it is a lesser point, as in some other markets, online commerce represents virtually 100 percent of the net growth.

source: www.nielsen.com

Researchers have been predicting for several decades that computing is going to be pervasive. What we are seeing is the realization of that prediction. Some say "fourth industrial revolution" is coming. Some of us might simply say the era of pervasive computing, as predicted, is arriving.

It is not simply "production" that is going to be affected, affecting industries and economics. Human consumption, lifestyles and behaviors are going to change, as well. This is big, very big.

{kind=link}