The Federal Communications Commission will vote in November 2017 to make available 1,700 MHz of high-frequency spectrum for 5G.

Two spectrum bands will be allocated, providing 700 MHz in the 24 GHz band and 1 GHz in the 47 GHz band.

A year ago, the FCC allocated 11.65 GHz of spectrum with 3.85 GHz of that allocated in the 28 GHz and 37 GHz to 40 GHz bands. Additional spectrum is still under consideration to be allocated in the future.

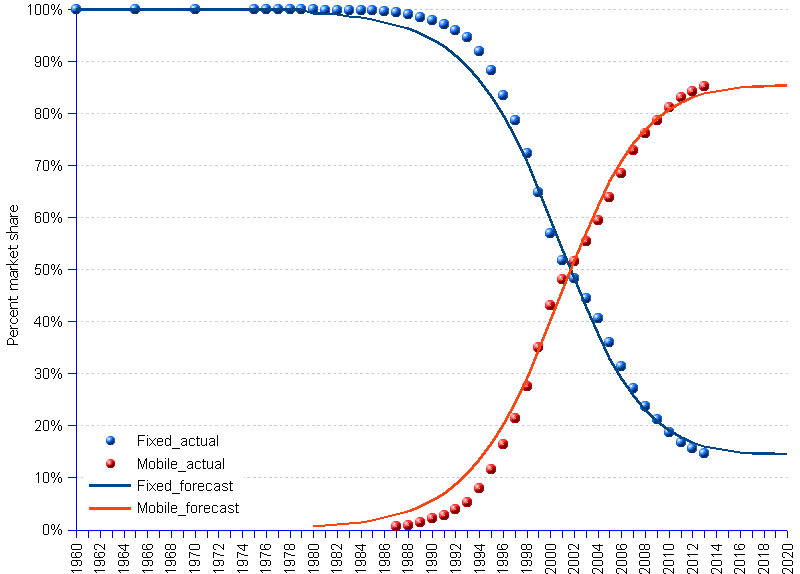

All that new spectrum, plus spectrum sharing and spectrum aggregation, will lead to mobile internet access becoming very price-competitive with fixed internet access, for many users and use cases.

Some might still doubt that 5G will create, for the first time, full product substitution by mobile networks for fixed network internet access. Traditionally, the objections were well founded, and based on value and price objections.

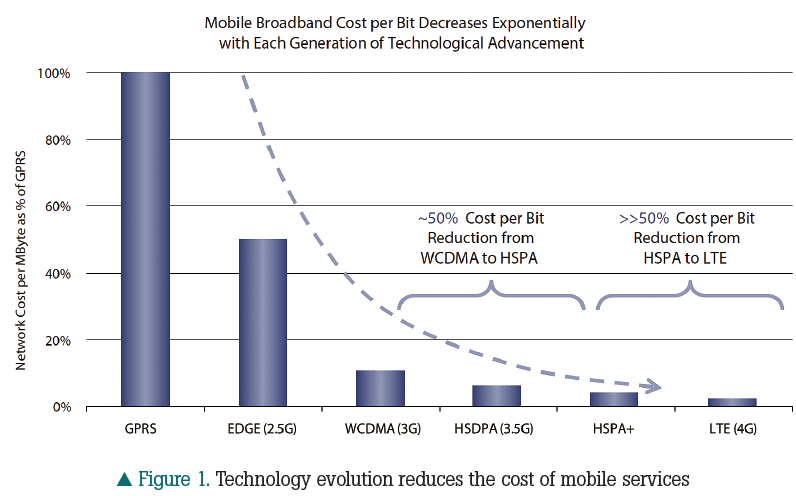

Mobile traditionally has been much slower than fixed, and cost per bit has been at least an order of magnitude higher for mobile alternatives.

Of course, nothing stands still, where it comes to network platforms and technologies for internet access. Even before spectrum sharing, aggregation of licensed and unlicensed spectrum and new allocations of millimeter wave capacity, each mobile broadband network generation has reduced cost per bit by about 50 percent.

So there is little reason to believe 5G will be different. To wit, a reasonable person would forecast that cost per bit for mobile internet access will drop at least another 50 percent.

To be sure, mobile bandwidth, on a cost-per-bit basis, remains an order of magnitude or so more expensive than fixed alternatives.

Of course, that comparison has been based solely on “mobile” versus “fixed” economics. In the next era of spectrum sharing and aggregation of licensed and unlicensed assets, “fixed” access becomes part of “mobile” access.

That logically should propel “mobile” access faster down the cost curve, as “mobile” access is based, in substantial part, on use of unlicensed (“no incremental cost”) assets.

When aggregating mobile access with unlicensed, the assumed cost of the unlicensed capacity is fairly close to zero, as there is no “cost of goods” (the unlicensed access is provided on a no-additional-charge basis).

A mobile service provider supplying a unit of access service to a device blends the cost of using its own network ($ per delivered gigabyte) with “no out of pocket cost” (close to zero dollars per gigabyte) unlicensed gigabytes.

If you assume the mobile network cost of delivering a gigabyte will drop 50 percent from 4G to 5G, an incremental drop will be added by shifting much usage to the Wi-Fi or other unlicensed spectrum networks.

The point is that the cost of using a gigabyte of “mobile” access will be quite close to the cost of using a gigabyte of “fixed” access, especially on an “actual consumption” basis.

Obviously, the actual cost of using any internet access service, no matter what the posted retail rate, is directly related to the actual amount of usage, compared to the retail recurring cost.

A user might pay for use of 10 Gbytes on a mobile network, at $2 to $8 per gigabyte, compared to a fixed network cost of perhaps five cents per gigabyte.

The out of pocket cost of the mobile access might be $30 a month, while the cost of the fixed access might be $60 a month. The new reality, though, is that the mobile cost will include use of an almost-unlimited amount of unlicensed network access.

That means the “actual” cost of a $30 a month mobile plan includes hundreds of gigabytes of effective usage. In that case, the cost per bit of mobile access is virtually indistinguishable from the cost per bit for fixed access.