Online advertising markets face significant long-term challenges, including growing demands for privacy that will have the practical effect of raising operating costs for ad platforms. That trend has been a threat since the rise of ad blockers, is raised by new data privacy rules and might evolve again if blockchain and other approaches to user ownership of data actually become ubiquitous.

But challengers also will not stop trying to unseat Google and Facebook, either.

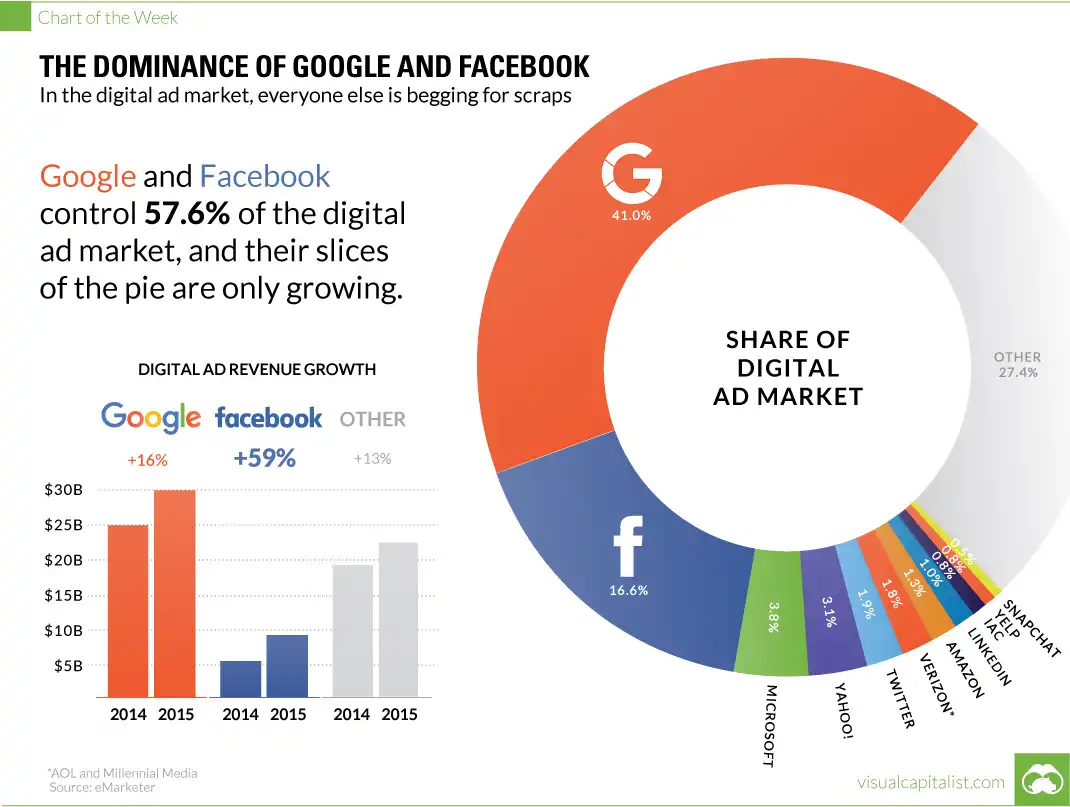

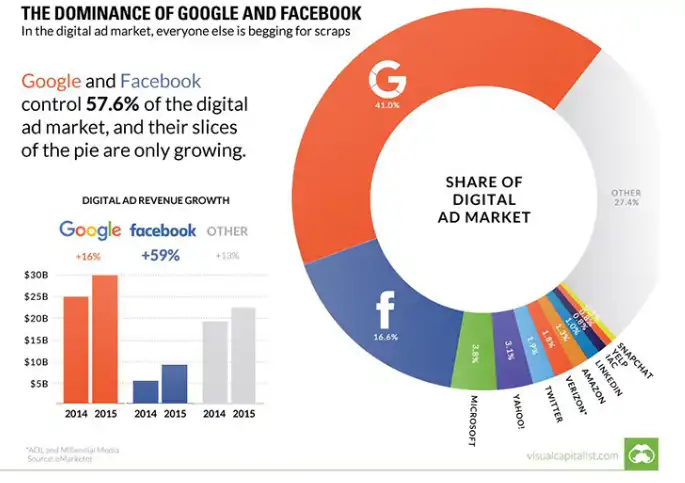

AT&T hopes to create a viable ad exchange platform for advertisers who want an alternative to Google and Facebook. Verizon hopes to do the same, with less universal scope. In that regard, a number of other app providers also hope they can become the third option to Google and Facebook. And that list of would-be contenders includes Amazon and Twitter, for example. So it will not be easy for any contender to emerge as a significant third alternative.

Some 43 percent of respondents felt negatively towards advertisements, compared to a similar survey from April of 2017 where only 34 percent reported a negative sentiment. So digital platforms perhaps are making some of the same mistakes linear video advertising channels have made, namely showing too many ads.

But challengers also will not stop trying to unseat Google and Facebook, either.

AT&T hopes to create a viable ad exchange platform for advertisers who want an alternative to Google and Facebook. Verizon hopes to do the same, with less universal scope. In that regard, a number of other app providers also hope they can become the third option to Google and Facebook. And that list of would-be contenders includes Amazon and Twitter, for example. So it will not be easy for any contender to emerge as a significant third alternative.

According to at least one new survey, consumers tend to see Google and Facebook as the most influential ad platforms. Facebook (54 percent) and Google (44 percent) were cited by consumers as the most influential platforms for advertising.

Instagram (23 percent), Spotify (28 percent), and Pandora (24 percent) followed Google and Facebook.

Some 43 percent of respondents felt negatively towards advertisements, compared to a similar survey from April of 2017 where only 34 percent reported a negative sentiment. So digital platforms perhaps are making some of the same mistakes linear video advertising channels have made, namely showing too many ads.