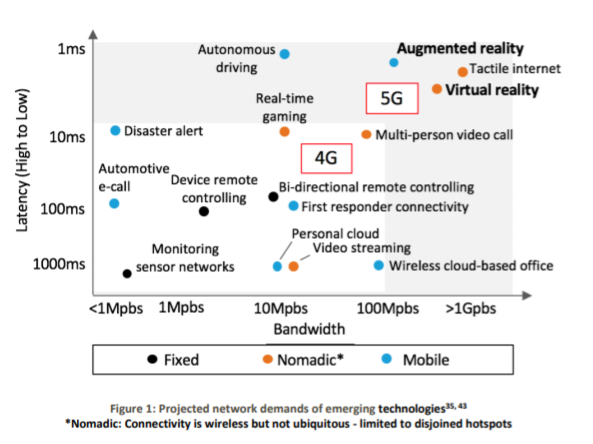

We sometimes rhetorically ask “which came first, the chicken or the egg?” when attempting to explain how some change, requiring multiple changes to create a useful new product. So it is with many potential innovations 5G might help enable, from precision farming to parking.

Nor does it seem an unusual or uncommon problem in the connectivity or application businesses. #Chicken and egg” strategy problems occur whenever the value proposition for two separate groups is dependent on adoption and use by the other.

In other words, where network effects exist--such as for communications networks--there always is a chicken-and-egg problem. Investments precede actual use; the network and capabilities have to exist before customers can buy and use them. So chickens come before eggs.

In the applications business, this is particularly important if the new business has a winner-take-all character, as so many platform businesses seem to have. That roughly explains the strategy of investing to gain share fast, instead of investing more slowly to produce operating profits.

Amazon, eBay, YouTube, Facebook and even the Microsoft operating system required or benefitted from network effects or scale.

The general problem is that a critical mass of potential customers and users is required before investments make sense, but availability ot the infrastructure is required before customers can use the product.

Consider connected parking, where vehicles with microservices and connectivity can pay for city parking without the use of dedicated parking meters. The whole system does not work autonomously until every car is equipped with connectivity, sensors and software, which likely means a 20-year transition period, until every non-equipped vehicle is retired.

There are some partial workarounds, such as using smartphones to conduct the transactions, but that does not dispense with the need to support the existing infrastructure as well as the new.

Chicken-and-egg strategies seem generally to require some period of investment before critical mass is achieved; never an easy sell to investors. Printers cannot be sold without ample access to ink refills, or consumer goods without access to shelf space and good placement. So payments to retailers to stock the products, or assure prominent shelf placement, might be necessary.

Blackberry by Research in Motion never seemed to solve that problem of creating a robust base of app developers for its hardware. In addition, Blackberry’s operating system never worked as well as newer operating systems optimized for mobile web interactions.

In other cases it might be possible to create scale by identifying an existing mass of creators, suppliers or products, and then building on them to create scale. Many note that Microsoft DOS profited by its compatibility with word processing app WordStar and spreadsheets VisiCalc and Lotus 1-2-3.

Some might note that Airbnb gained by allowing its listing to be shown on Craigslist, while Google allowed Android to be used by many handset vendors.

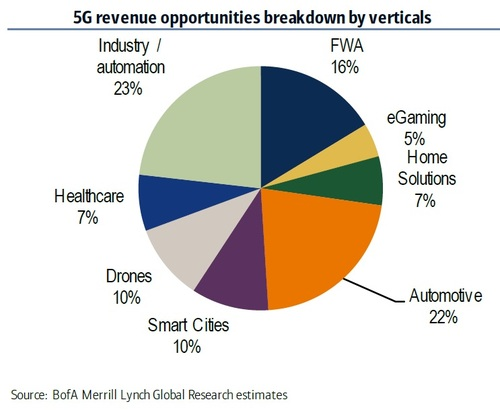

The point is that telecom services represent classic chicken-and-egg problems, and 5G will not be different. The network has to be in place before innovators and developers can start to figure out how to take advantage of the platform.