Sunday, September 6, 2020

Keyboard Made from Paper Operates Without Batteries or Power Sources

Devices that work using only ambient energy are interesting for many sensor or internet of things applications. But researchers also are experimenting with keyboards that require no external source of power, either.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"MEC Platform" is Intriguing, if Difficult

Few terms are harder to define than "platform." Some define "platform" as the computer architecture and equipment using a particular operating system. So Windows or IoS or Android are platforms. Others might say a computing platform or digital platform is the environment in which a piece of software is executed.

Some might say cloud computing or virtual machines are platforms. Apple's App Store often is considered a platform.

A platform also can be a business model that creates value by facilitating exchanges between two or more interdependent groups, usually consumers and producers. So eBay, Amazon.com, Uber, Airbnb and any advertising marketplace are platforms.

Some telcos are optimistic about prospects for multi-access edge computing, including the opportunity to function as a platform for edge computing. The MobiledgeX initiative is a good example of that belief. MobiledgeX hopes to build an ecosystem of developers able to use common global interfaces, telco data centers and integrated 5G access.

The MEC is envisioned as being complementary to the current hyper-scale computing as a service platforms such as AWS Wavelength and Azure Edge Zone. The issue, as always, is how much value actually can be created by a telco-owned edge computing platform or even actual edge computing as a service.

Already, hyperscalers are moving to create their own edge computing as a service offers. In those instances, telcos become providers of real estate services and connectivity, but not the platform for developers or actual edge computing as a service.

It remains at this point an open question whether, and to what extent, a MEC platform can be created, and what value any potential platform can provide.

It never is easy for any participant in an ecosystem to emerge in additional roles, and has historically been challenging for telcos. Edge computing might not prove much different.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Any Revenue Growth for Telecom in 2020?

Before the Covid-19 pandemic, many telecom service providers expected modest revenue growth. In 2020, most are likely to show flat to negative revenue and revenue growth. Many service providers now expect revenue shrinkage instead.

But the longer-term trend will reassert itself fairly quickly, in all likelihood, as global revenue growth has been pretty close to flat for some years.

Overall, the global industry might not even hit one percent revenue growth in 2020.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

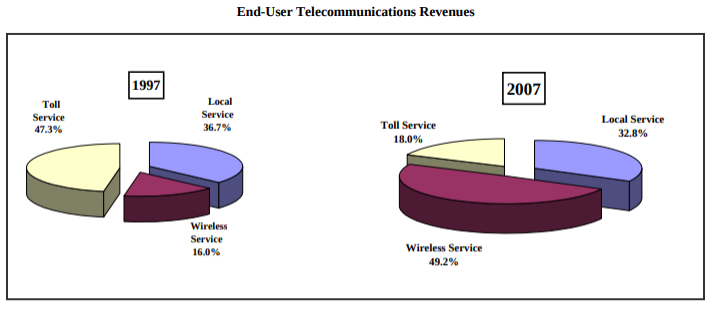

International Voice Shrinks 5% a Year

Researchers at Omdia estimate that international wholesale voice revenue will continue to decline at a compound average rate of growth of -4.8 percent through 2021 (and likely beyond) under the threat from over-the-top voice and messaging services. That trend was not completely clear 20 years ago, as the number of people using phones has grown dramatically.

Since then, especially as voice and messaging alternatives have grown, with declines starting in the U.S. market about 2001, and elsewhere about 2003.

In the monopoly era, it was principally such revenues that produced most of the profits in the telecom industry, and provided the surplus to support consumer services that, in many cases, actually lost money.

The industry long ago ceased to rely on international voice as the key revenue source. By the 1990s, mobile services had taken the place of international voice as the key revenue growth driver. More recently, text messaging and internet access have taken the place of mobile voice growth.

A similar trend can be noted for European Union mobile revenues between 2010 and 2018, a period of less than a decade, but still a time when voice revenue dropped from about 80 billion euros to about 45 billion euros, while messaging dropped from about 19 billion euros to perhaps 10 billion euros and mobile internet access grew from about 18 billion euros to perhaps 42 billion euros.

In the U.S. market, long distance voice still provided nearly half of all U.S. telco revenues. By 2007, mobility had grown to about half, while long distance had shrunk to about 18 percent.

What comes after mobility is a big question.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What to Do about Dominant Platforms?

Big digital platforms, especially Facebook, Google, YouTube and Twitter, are facing growing scrutiny about monopoly power and censorship. Consider the matter of political censorship, complaints which are growing louder.

Traditionally, the right of free speech, as enshrined in the First Amendment to the U.S. constitution, protects speakers from government censorship, but only government action. There is a long legal history that extended First Amendment protections to new electronic media.

The internet, though, and particularly the rise of social media platforms, seems to raise entirely new questions, such as whether free speech rights can, or ought to, be extended to protect citizens from censorship by private corporations. That is almost entirely new ground, and up to this point, the right of free speech does not exist on any social platform in the United States.

But some believe the traditional right of free speech, protecting citizens from government censorship, should be expanded in an era where “certain powerful private entities—particularly social networking sites such as Facebook, Twitter, and others—can limit, control, and censor speech as much or more than governmental entities,” argues David L. Hudson Jr., Justice Robert H. Jackson Legal Fellow at the Foundation for Individual Rights in Education.

The issue is whether it is possible to enlarge the space within which constitutional protections on free speech are expanded, yet also avoid damage to private property rights of platforms. And that is the issue. It is not clear that regulation can do so, whether the issue is a remedy for business monopoly or the promotion of free speech.

You might think the simplest answer is to simply allow people to speak their minds, with the exceptions of harassment and intimidation, threats of violence or promotion of criminal acts. But therein lies the problem, given the aggressively uncivil behavior one now sees on social media.

What one speaker sees as the free expression of ideas will be seen as aggression and threat from another. Some 30 years ago this was not really a problem. People were simply more polite. But it is hard to mandate polite behavior.

Many solutions seem to require “more regulation of platforms” which tends to mean “less freedom” for platforms, if arguably in pursuit of “more freedom” for speakers. And that raises an old issue: “who” has the right of free speech and its benefits, the speaker or the reader or listener.

The U.S. Bill of Rights, the first 10 amendments to the U.S. Constitution, provided that “Congress shall make no law” prohibiting the free exercise of speech or the press. Note the language, which protects people as speakers and the “press” as a speaker from government restriction.

Later broadcast media regulations sometimes shifted the focus a bit to the rights of listeners or viewers, rather than speakers. Generally speaking, however, the protected right is held by “speakers,” not “audiences.”

Perhaps the seminal case was Red Lion Broadcasting Co. v. FCC (395 U.S. 367, 393 (1969), which allowed some content regulation of broadcasting for reasons of promoting the public interest. The point is that speaker rights were somewhat subordinated to the rights of viewers and listeners (the public interest).

Complicating matters further is the issue of “who” the speaker is, in the context of a social media site or business: the platform or the users of the platform. Up to this point, it is the rights of the platform as “the speaker” which have been upheld, even if a platform supposedly is a neutral matchmaker between users who might, arguably, be considered the actual “speakers.”

The approach prioritizing the rights of audiences (listeners, readers, hearers) is exemplified by Alexander Meiklejohn’s book Free Speech and Its Relation to Self-Government, in which he says “what is essential is not that everyone shall speak, but that everything worth saying shall be said.”

All that assumes a singular public interest could even be identified.

It will not be easy to create a workable framework that expands the realm within which free speech protections exist on platforms, as the temptation will be to limit platform freedom to create more freedom of speech for users of platforms. But one philosophical choice might have to be made.

Is it the platform which has the right of free speech or is it platform users who have that right? And even if it is determined that platform users have the right, is it the speakers or the viewers, readers and listeners whose rights are to be protected?

Beyond all that, how algorithms or systems can be designed to accomplish, in neutral fashion, any of those goals also remains an issue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, September 5, 2020

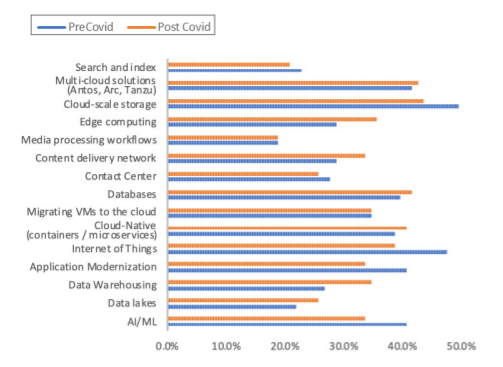

Big and Permanent Changes in Enterprise IT Priorities Post Covid?

With the caveat that intentions often do not match actual behavior, large enterprise professionals who are heavy cloud computing customers have post-Covid-19 priorities that have changed from pre-Covid levels. You would not be surprised if effort to support remote work had increased, for example.

But the differences, while showing some shifts, do not appear to have changed key priorities, or even the relative importance of various objectives. And since budgets and effort are essentially a zero-sum game, increased effort in some areas is matched by decreased effort in other areas.

The survey included 100-plus cloud-focused information technology directors at companies with at least $500 million in annual sales and IT budgets of at least $50 million per year, from many industries including technology, financial services, manufacturing, retail, oil and gas, life sciences, consumer packaged goods and media and entertainment, all using at least two different cloud platforms.

The point is simply that post-Covid behavior might not change as much as many now anticipate.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

No "New Normal" for 5G Searches

One frequently hears these days that a “new normal” has been created by the Covid-19 pandemic; that “nothing will be the same” afterwards. That is not to deny either a “temporary” change in behavior nor a step change in many aspects of life and business, where it comes to underlying trends.

We incontestably are behaving in different ways, partly the result of government mandates which are expected to be temporary. What happens after the pandemic is the issue. We should certainly expect a reversion to mean. Whatever trends were in place before the pandemic will reassert themselves, albeit from a higher level in many cases.

But that might not mean the rate of change changes very much. In fact, one might argue we already have seen this. This is a graph of Google searches for “5G.” Note the spike. That happened in March 2020 as many U.S. locations went into work-from-home and stay-home-from-school rules.

We have to guess at why the surge in searches happened, then so quickly receded, but a reasonable guess is that people were looking for remote work support solutions. But the spike only lasted from the end of March to mid-April. Then interest backed off to levels higher than before, but on the prior trend line.

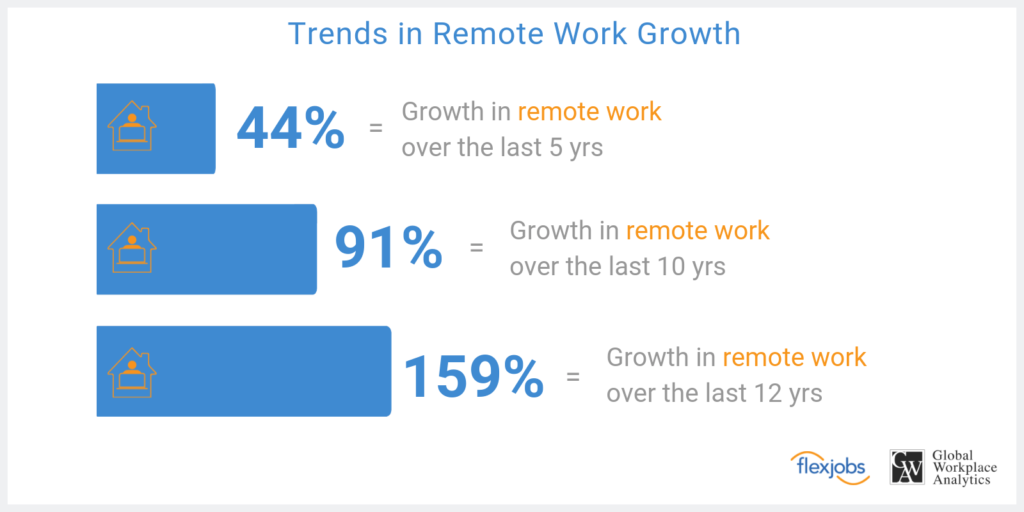

As hard as it might be to envision, that is likely to happen with many business, economic and personal trends, post-pandemic, and after a few years. Consider “remote work.”

In the midst of the Covid-19 pandemic, statistics on remote work are impressive enough to convince many observers that a fundamental and permanent shift has been made. We will know in five years whether that is an accurate assessment, but we also have to remember that “remote work” includes many disparate activities, many of which do not substantially affect the amount of time people actually spend at work places.

Work from home statistics often include actions such as “taking home some work from the office” (ranging from reading documents to correspondence management), working while traveling on business, unscheduled and episodic work from home, routine and planned work from home as well as permanent, full-time remote office or at-home workspaces.

Long-term trends in office space requirements, for example, typically depend on the amount of full-time, permanent basing at home locations, as well as permanent work-at-home for days per week or month.

One issue is how many jobs theoretically could be done entirely from home. “We estimate that 56 percent of the U.S. workforce holds a job that is compatible (at least partially) with remote work,” say researchers at Global Workplace Analytics. That noted, pre-Covid-19, “only 3.6 percent of the employee workforce works at home half-time or more, the firm notes.

Using every definition of work from home, including casual “take work home with you,” Gallup data from 2016 shows that 43 percent of the workforce works at home at least some of the time. So much hinges on the shift of the workforce to work from home at least 50 percent of the time.

source: Global Workplace Analytics

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

Enterprise Leaders Say They Now Use Generative AI Tools Routinely

A new survey by the Wharton School (University of Pennsylvania) Human-AI Research suggests that enterprise leaders now use generative arti...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...