Mobile operators worldwide lost an estimated $33 billion from security breaches and fraud in 2020 and will lose $41 billion in 2024, according to Kaleido Intelligence. Those of you with long histories in the industry might agree that keeping losses in about that range might well be as good as it gets.

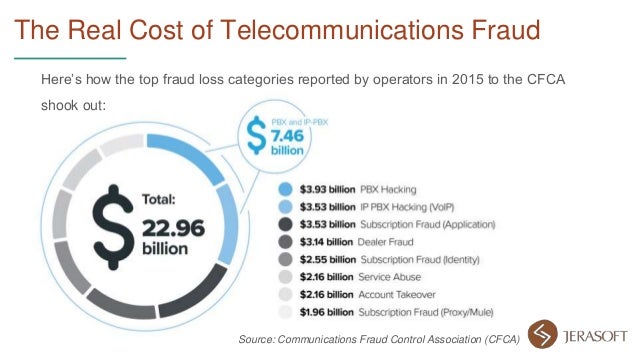

Others will dispute those figures. According to the Communications Fraud Control Association, in 2021 losses from fraud--globally--will amount to about $28.3 billion. The problem for loss control staffs is that no single type of fraud dominates.

There is simply a bit of revenue leakage cross many parts of the operation of a communications service provider business. According to CFCA, the biggest single source of revenue leakage, at $5 billion, is international revenue share fraud, something that happens between service providers.

One might argue this is less “fraud” than “mistakes.” But most sources of revenue leakage do not amount to much more than $1 billion or $2 billion annually, on a global basis. The point is that the actual loss for any single service provider is relatively small.

So the issue is how much time, effort and money can reasonably be spent to reduce the amount of such leakage. It probably is not reasonable to reduce such “fraud” or mistakes to zero.

The more relevant question is how to protect most revenue from shrinkage, knowing that some shrinkage will occur, even when the best billing and other practices are in place. One might also argue that industry practices already have reduced a substantial amount of fraud and mistakes.

In 2013, global service provider losses (fixed network plus mobile network) from long distance alone were about $46 billion, according to Over the Wire. Others will dispute the size of the loss.

By some estimates, in 2019 the amount of long distance fraud from business phone systems was less than $3 billion. In 2015 business phone system losses were probably in the $23 billion range.

The point is that service providers should protect themselves from fraudsters and maintain other policies that reduce shrinkage caused simply by billing and other largely preventable failures.

But stopping all revenue shrinkage might cost more than it saves.

{kind=link}