It’s fairly easy to explain why cable TV programming networks face an existential crisis. Shrinking audiences attack 85 percent to 90 percent of the revenue base.

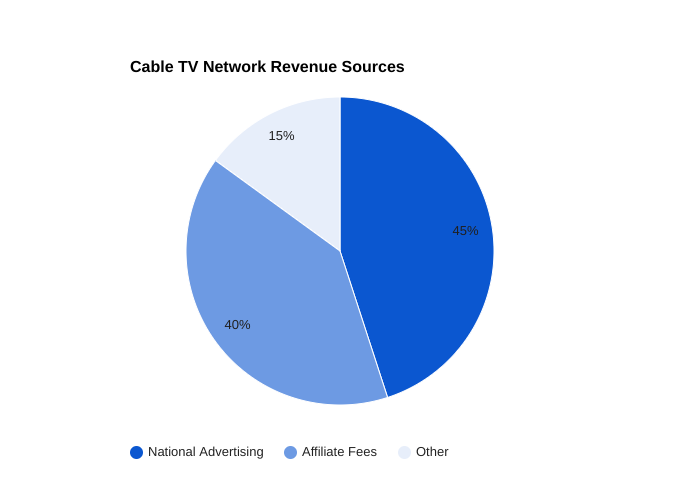

Their revenue is driven by advertising (perhaps 40- to 45 percent of total) and affiliate fees paid by distributors (about 50- to 55 percent). The former is dependent on the volume of viewers, which is declining every year. The latter is dependent on the number of potential viewers a distributor can deliver (subscribers).

Both are essentially “potential attention” metrics and are declining. Subscriber volume provides potential larger audiences while also making any particular distributor more or less valuable as a platform for such potential audiences.

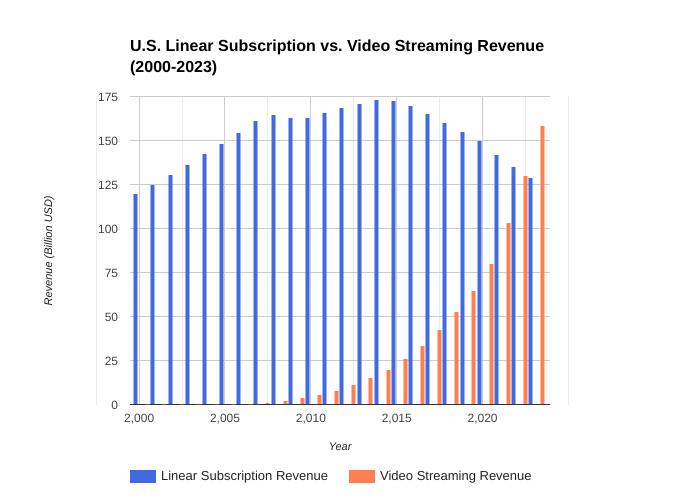

If subscription decline is irreversible, then so are advertising and affiliate fee revenues. By some estimates, video streaming revenue already has surpassed the level of linear video subscription revenue.

But most content business models also have been disrupted by the internet and digital content distribution. So far, most of the angst about artificial intelligence has been on its potential to disrupt content industry jobs by automating the functions.

Industry | Traditional Business Model | Disrupting Technology/Trend | New Business Model |

|

|

|

|

Cable TV | Subscription-based service for linear channels | Streaming services (Netflix, Hulu, etc.), cord-cutting | Subscription-based streaming services, ad-supported streaming, live TV streaming |

Long Distance Calling | Per-minute charges for long-distance calls | Voice over IP (VoIP) technology | Flat-rate long-distance plans, VoIP services |

Local Telephone Service | Landline phone service with monthly fees | Mobile phones, VoIP services | Mobile phone plans, VoIP services |

Postal Services | Physical delivery of letters and packages | Email, digital messaging, online shopping | Digital delivery of mail, specialized shipping services |

Retail Shopping | Physical stores, in-person shopping | E-commerce, online marketplaces (Amazon, eBay) | Online shopping, omnichannel retailing, subscription boxes |

Music Distribution | Physical media (CDs, vinyl records) | Digital music distribution (iTunes, Spotify) | Digital music streaming, music subscription services |

Newspapers | Print newspapers, subscription-based model | Online news, digital subscriptions | Online news, digital subscriptions, ad-supported news |

Magazines | Print magazines, subscription-based model | Digital magazines, online content | Digital magazines, online content, ad-supported content |

Movie Theaters | In-theater movie screenings | Streaming services, video-on-demand | Streaming services, video-on-demand, premium video-on-demand |

Home Video | Physical media (DVDs, Blu-rays) | Digital video rental, streaming services | Digital video rental, streaming services, video-on-demand |

While an apt observation, it is the disruption of existing business models which will have the greater impact. It might be easy to suggest that AI will restructure many business processes in content industries. What is harder to ascertain is the ultimate impact on business models.

The mere fact that AI creates content instead of humans does not necessarily disrupt the revenue model, only changing the cost model. Distribution could be an area of greater change, though, as most content industry disruptions are founded on distribution (display) technology changes.

Television disrupted movie theater exhibitions. Cable TV disrupted over-the-air broadcasts. The VCR enabled the home video business, the DVD improved it; video streaming ended it. Audio tape, then compact discs largely displaced the records business. But music streaming largely displaced all physical media distribution.

Industry | Traditional Business Model Characteristics | Potential AI Disruption | New Business Model Characteristics |

Content Creation | Human creators, editors, and producers | AI-generated content, automated editing, and production | AI-assisted content creation, personalized content experiences, dynamic content adaptation |

Content Distribution | Traditional media channels, physical distribution | AI-powered personalized content delivery, direct-to-consumer distribution | AI-driven content recommendation systems, dynamic pricing, real-time content adaptation |

Content Consumption | Passive consumption, linear storytelling | Immersive experiences, interactive storytelling, personalized content | AI-powered interactive content, virtual and augmented reality experiences, personalized content journeys |

Copyright and Intellectual Property | Traditional copyright laws, licensing fees | AI-generated content ownership, copyright infringement challenges | AI-powered copyright management systems, dynamic licensing models, new revenue streams from AI-generated content |

Advertising | Traditional advertising models (TV, print, digital) | AI-powered targeted advertising, programmatic advertising | AI-driven personalized advertising, dynamic ad placement, brand experiences powered by AI |

Education and Training | Traditional classroom-based learning, standardized content | AI-powered personalized learning, adaptive content | AI-driven learning platforms, personalized tutoring, skills-based learning |

Entertainment | Traditional entertainment formats (movies, TV shows, games) | AI-generated entertainment, interactive gaming, virtual reality experiences | AI-powered interactive entertainment, personalized gaming experiences, virtual and augmented reality content |

The cumulative impact of digital media and internet distribution has enabled a shift to on-demand consumption and away from linear formats across virtually all media. That, in turn, has altered the advertising and affiliate revenue basis for linear video subscription services.

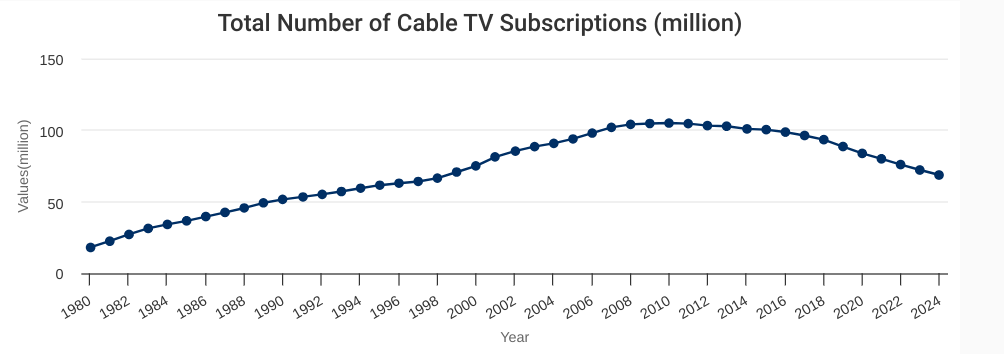

U.S. subscriptions, for example, peaked around 2010 and have been steadily declining since then.

source: IBISWorld

Though there are many reasons for the lower demand for linear video subscription services, the threats to advertising and affilate fee revenue streams are the most obvious.

Challenges for Linear TV & Cable TV | Advantages of Streaming Alternatives |

Rigid Scheduling: Viewers must watch programs at set times. | On-Demand Viewing: Content is available anytime, allowing flexibility. |

High Subscription Costs: Cable packages are expensive and include unwanted channels. | Lower Cost Options: Streaming services offer affordable subscription plans and bundles. |

Ad Interruptions: Traditional TV has frequent and lengthy ad breaks. | Ad-Free or Limited Ads: Streaming platforms offer ad-free tiers or fewer interruptions. |

Lack of Personalization: Limited ability to customize programming to individual tastes. | Personalized Recommendations: AI algorithms suggest content based on viewing habits. |

Limited Mobility: Watching requires a TV or cable box at a fixed location. | Cross-Device Access: Streaming is available on phones, tablets, smart TVs, and laptops. |

Outdated Content Delivery: Programming is tied to fixed schedules, making discovery difficult. | Content Libraries: Vast libraries of current, past, and exclusive content are accessible anytime. |

Declining Viewer Engagement: Younger audiences are abandoning traditional TV. | Appeals to Younger Audiences: Streaming platforms cater to younger demographics with interactive and diverse content. |

Complicated Bundles: Bundled cable TV packages force customers to pay for unwanted channels. | A La Carte Options: Consumers can subscribe only to the services or shows they want. |

Geographical Restrictions: Content availability is often tied to specific regions. | Global Accessibility: Streaming platforms offer consistent access to content worldwide. |

Slower Technology Adoption: Traditional TV struggles to incorporate new technologies quickly. | Cutting-Edge Technology: Features like 4K, HDR, offline viewing, and voice control enhance the experience. |