The International Telecommunications Union recently defined “LTE-Advanced” and “WirelessMAN-Advanced” as the only "official definitiions of "fourth generation" networks, automatically making networks operated by Sprint, Clearwire, Verizon, MetroPCS and all other operators of WiMAX and Long Term Evolution networks something other than standards-based "4G" networks.

Now the ITU has muddied the waters even more, saying that some "3G" networks are "4G," while the formal "pre-4G" networks in existence, or about to be built, also are "4G."

"As the most advanced technologies currently defined for global wireless mobile broadband communications, IMT-Advanced is considered as “4G”, although it is recognized that this term, while undefined, may also be applied to the forerunners of these technologies, LTE and WiMax, and to other evolved 3G technologies providing a substantial level of improvement in performance and capabilities with respect to the initial third generation systems now deployed," the ITU says in a new statement.

Huh? Some of us have had no issue with T-Mobile USA saying its new HSPA+ network offers "speeds equivalent to 4G," because the WiMAX and HSPA+ networks do offer comparable access speeds. But it does create a definitional muddle. It's one thing for marketplace contestants to position their networks in one way or another.

It might be quite another for a "standards" body to argue that 3G is 4G, existing 4G is 4G, and other possible networks might also be 4G.

What's the point of a standard when it isn't a standard any longer? In this case, it might mean that the "non-standard" standards will grow organically to the point that the newly-minted "4G" standard simply ceases to be relevant, much as adherence to the supposedly-"legacy" TCP/IP completely killed the shift to new protocols for layers one through four of the data communications protocols.

One might say the ITU flip flop is merely embarassing, and yet another example of standards bodies attempting to define "next generation" networks. It might result in something far more substantial than that. One might suggest that the whole effort now is questionable, in terms of helping shape the development of 4G.

Once critical mass developments around the real-world 4G and advanced 3G networks, services, revenue elements and devices, evolution will happen based on those factors. That doesn't mean operators will abandon the effort to keep developing more-capable networks. But as we have seen with TCP/IP and other data "standards," the market often decides what a standard is.

So far, the markets, and end users, have decided the path for next-generation networks, in large part. That could well happen here as well. No matter what the ITU thinks, if voluntary groups such as the GSM decide to evolve LTE in some other direction, the existence of a formal standard will not deter them.

That is not to fault the well-intentioned hard work of the technologists working on the standard. The point is simply that the global telecommunications industry has yet to prove it can devise a "next-generation" network standard that real-world operators actually embrace obviously, and with great commercial success. Instead, the pattern so far has been that network operators and end users sort of grope towards better solutions as best they can.

But it is equally true that, up to this point, real-world commercial success has not been driven so much by the standards as by solutions that users believe are workable and useful.

For a discussion f the ITU standards, read this: http://www.itu.int/itunews/manager/display.asp?lang=en&year=2008&issue=10&ipage=39&ext=html and this http://www.networkworld.com/news/2010/121710-itu-softens-on-the-definition.html.

For a discussion of the change, arguing that the ITU now has erred twice on the same subject, see http://www.abiresearch.com/research_blog/1520.

Showing posts sorted by relevance for query ITU. Sort by date Show all posts

Showing posts sorted by relevance for query ITU. Sort by date Show all posts

Sunday, December 19, 2010

ITU Says Some 3G Networks are 4G, Pre-4G is 4G, and 4G is 4G

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, March 24, 2022

When "Data" Does Not Match "Perceived Reality" Perhaps the Data or Your Perceptions are "Wrong"

Trying to figure out what people really pay for home broadband is tricky. Prices differ by provider, location and the number of competitors in a market. Prices also vary by the level of government subsidies and take rates of such subsidies.

One has to decide which plans to compare, and those choices shape the outcomes. The other issue is the inability to adjust the analysis for discounts and promotions that affect what customers actually pay. In other words, the retail tariffs we choose to compare are not necessarily reflective of active consumer behavior.

The most recent example of this is an analysis of home broadband costs by the Internatiomal Telecommunications Union, which reports that the “lowest-priced home broadband plan” offered by the largest U.S. supplier average more than $130 a month.

If you follow U.S. broadband prices, you know that is incorrect. Since the largest U.S. ISP is Comcast, the ITU must have looked at Comcast’s stated prices. And if you check, you can see that the stated retail price (after a promotional period) does jibe with the ITU figures.

The issue is that Comcast customers do not seem to be paying triple-digits for the “lowest-cost” home broadband plans.

That seems wildly incorrect. Methodology is an issue. The lowest-cost budget plans typically are in the $10 to $15 a month range and support speeds around 50 Mbps (moving higher, as do speeds on all plans).

Those are the plans ITU should have reviewed were it looking at the comparable “lowest-cost plans offering 5 Gbytes of usage and minimum speeds.”

source: HighSpeedInternet.com.

But those plans are rarely listed on websites showing available plans. You would have to hunt to find plans offered by all leading ISPs for low-income households.

Instead, the ITU researchers seemingly looked at prices shown on the Comcast websites that do not represent the comparable lowest-cost plans. To be sure, Comcast, the largest U.S. ISP, shows charges of $30 a month for services operating at 100 Mbps.

And, to be sure, Comcast also says those prices are good only for one year, with sharp price increases after 12 months. Comcast says its 100-Mbps plan will grow to $81 a month after 12 months.

The issue is that it would be hard to find anybody who actually pays that amount for a 100-Mbps service, even after a 12-month period.

The average U.S. home broadband service costs about $64 a month. If the cost of the lowest-priced plan really were more than $100 a month, as the ITU analysis suggests, the “average” U.S. price could not be as low as $64. By definition, the average would have to be much higher.

According to Openvault, only about 20 percent of U.S. households purchased services operating at 100 Mbps or less in the second quarter of 2021 and only 18 percent in the third quarter of 2021 and 17 percent by the fourth quarter of 2021.

And that is why methodology is so important. Actual measurements of home broadband speed show only 17 percent of subscribers are provisioned for speeds less than 100 Mbps. Only nine percent are provisioned for speeds of 50 Mbps or slower.

The point is that any analysis of home broadband focused on the lowest tier of service, in terms of speed or price, would not tell you very much, in any country. What is arguably much more useful is an analysis of the “typical” plans customers buy, and not the highest or lowest price plans; fastest or slowest speed options available.

Unless one is clear about methodology, it is easy to make unclear or misleading statements, such as “X percent of customers do not have access to Y speeds.” Does that mean such customers cannot buy because the service is not available? Or does it mean they could buy, because the service is available, but they choose not to buy, preferring some other plan?

The answers matter.

I may choose not to buy a Tesla. That does not mean I cannot buy a Tesla. Some will rightly argue that home broadband is a necessity, and a Tesla is not. Noted. But virtually all the global data shows that, over time, the cost of home broadband globally has declined, measured as a percentage of gross national income per person.

To be sure, according to the ITU, fixed broadband prices (adjusted using the purchasing power parity method) have risen since 2015, after dropping since 2008, while mobile data costs have dropped steadily.

But 2020 prices were still lower than in 2008, and that assumes we accept the data as accurate, which I do not. If the same methodological issue applies to other markets, then prices are overstated.

Beyond all that, there are hedonic adjustments, referring to the change in a product’s performance over time. Beyond price, the performance of our smartphones, personal computers or home broadband are vastly different than they were 20 years ago.

Is the $300-per month 756 kbps internet access connection I was buying about 1996 the same product as the gigabit connection I now buy that costs possibly $85 a month? Is that gigabit connection the same product as the 300-Mbps connection I was buying a year ago, even if that product “cost less” than the gigabit connection?

Methodology always matters when evaluating home broadband availability, quality and cost. In this case, the ITU analysis seems quite flawed.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, September 24, 2013

Fixed Broadband Prices Have Dropped 82% Over 5 Years

Over the past five years, fixed broadband prices as a share of gross national income per capita have dropped by 82 percent, the ITU says.

In 2012, fixed broadband services remained expensive, though, accounting for 30.1 percent of annual monthly incomes in developing countries, compared to just 1.7 percent in developed countries), By the end of 2013, there will be more than three times as many mobile broadband connections as there are conventional fixed broadband subscriptions, according to the International Telecommunications Union’s State of Broadband Report.

In 2012, the number of developing countries where broadband cost less than five percent of annual income remained the same as in 2011, at a total of 48.

In 22 developing countries, prices ranged up to two percent of average income, while in 26 countries prices were between two percent and five percent.

The point is that people can afford broadband when it costs less than five percent of their annual income. That implies that fixed broadband access is unaffordable for 3.9 billion people, and mobile broadband is unaffordable for over 2.6 billion people around the world.

The number of developing countries where broadband cost between five percent and 10 percent

of average income has increased from 15 in 2011 to 24 in 2012, the ITU says. In 18 developing countries annual cost is between five percent and eight percent of annual income, while in six countries broadband cost is between eight and 10 percent of annual income.

In 49 economies in the world, primarily developed economies, broadband access in 2010 cost less than two percent of average income.

This compares to 32 economies in the world in 2010 where broadband access cost more than half of average national income.

In 2010, there were 35 developing economies (out of 118) where broadband access cost less than five percent of average monthly income, up from 21 two years earlier.

Current ITU development goals include a target of entry-level broadband services, available at less than five percent of average monthly income, in developing countries by 2015.

By the end of 2013, the number of broadband subscriptions in the developing parts of the world will exceed the number of broadband subscriptions in the developed regions of the planet for the first time, the ITU also notes.

Licensed spectrum has underpinned the growth of the mobile industry and remains essential, unlicensed spectrum (Wi-Fi, primarily) has become an important part of the way people get access to the Internet.

Other forms of spectrum sharing also are starting to get attention.

Mobile broadband also is the fastest growing technology in human history, according to the ITU.

By the end of 2013, the ITU predicts there will be 2.1 billion mobile broadband subscriptions in use, equivalent to one third of the total number of mobile cellular subscriptions in service globally. In 2011, mobile broadband was used by 20 percent of mobile customers.

Morgan Stanley estimates that the number of unique smart phone users is around 1.5

billion in 2013, with smart phone subscriptions estimated to exceed four billion by 2018. Mobile broadband is projected to reach seven billion subscriptions in 2018.

Mobile broadband subscriptions, which allow users access to the Internet from their smart phones, tablets and WiFi-connected laptops, are growing at a rate of 30 percent per year, the ITU says.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, February 19, 2009

ITU Issues Views on Recession Impact on Telecom

At a high level, nobody is completely sure consumer behavior in this recession will match behavior in past recessions, for any number of painfully obvious reasons. There also is some thinking that as broadband had not attained mass adoption status during the last recession, this will be the first test of demand elasticity for fixed broadband.

And nobody seems to believe that wireline voice will in any way be helped. There is probably less consensus on what will happen in the wireless business, but wireless service providers likely are among the best-placed industry segments during the recession, in part because of greater "flexibility in their cost structure and capex and fixed-mobile substitution," a new report by the International Telecommunications Union says.

And though broadband access demand is believed to be relatively inelastic, that almost certainly will not be the case for fixed voice.

"Telecom services are likely to come under further price pressure, as operators will fight for a more cost-focused customer, resulting in further erosion of margins," the ITU suggests. And that is going to favor mobile operators as well.

"The more flexible cost structure of mobile networks means that mobile operators are winning more of the lower usage end of the fixed services customer base," the ITU says. "This has happened in voice, and 2008 has demonstrated that mobile broadband can substitute for light-usage DSL."

For countries where data services are popular, data revenues could be adversely impacted by a reduction in consumers’ real incomes, ITU says. Also, more consumers are likely to opt for prepaid and flat-rate packages for telecom services to try and control their expenditure.

Unemployment may accelerate fixed-mobile substitution, with consumers preferring to switch

fully to mobile services. Young people may delay decisions to adopt a fixed broadband or voice line in addition to mobile service.

Unemployment will accelerate households’ decisions to give up fixed services, either because they are unaffordable, or because a mobile alternative is cheaper.

"In terms of practical pricing strategy, the economic slowdown will increase pressure on operators to reduce prices," the ITU says. Operators will find it harder to promote value-added services and the adoption of new services such as mobile TV will be affected, ITU believes.

And nobody seems to believe that wireline voice will in any way be helped. There is probably less consensus on what will happen in the wireless business, but wireless service providers likely are among the best-placed industry segments during the recession, in part because of greater "flexibility in their cost structure and capex and fixed-mobile substitution," a new report by the International Telecommunications Union says.

And though broadband access demand is believed to be relatively inelastic, that almost certainly will not be the case for fixed voice.

"Telecom services are likely to come under further price pressure, as operators will fight for a more cost-focused customer, resulting in further erosion of margins," the ITU suggests. And that is going to favor mobile operators as well.

"The more flexible cost structure of mobile networks means that mobile operators are winning more of the lower usage end of the fixed services customer base," the ITU says. "This has happened in voice, and 2008 has demonstrated that mobile broadband can substitute for light-usage DSL."

For countries where data services are popular, data revenues could be adversely impacted by a reduction in consumers’ real incomes, ITU says. Also, more consumers are likely to opt for prepaid and flat-rate packages for telecom services to try and control their expenditure.

Unemployment may accelerate fixed-mobile substitution, with consumers preferring to switch

fully to mobile services. Young people may delay decisions to adopt a fixed broadband or voice line in addition to mobile service.

Unemployment will accelerate households’ decisions to give up fixed services, either because they are unaffordable, or because a mobile alternative is cheaper.

"In terms of practical pricing strategy, the economic slowdown will increase pressure on operators to reduce prices," the ITU says. Operators will find it harder to promote value-added services and the adoption of new services such as mobile TV will be affected, ITU believes.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, September 25, 2012

How Long Can Separate Regulation of Broadcasting, Cable, Communications Continue?

It long has been a fixture of regulatory policy that different media have had distinct regulatory frameworks. In the U.S. market, the fundamental frameworks include unregulated “media,” partially regulated broadcasting and cable; and heavily-regulated common carrier services.

That “regulation by function” made sense at the time. As all networks become multi-purpose networks, the logic of regulating networks “by function or media type” is subverted. That necessarily raises huge issues that affect the foundation of contestant business models.

In a simple way, the issue is whether stricter common carrier rules should be applied to "less regulated" media, or whether less regulation should be applied to common carrier services.

Also, some would argue, the growing instability of all legacy revenue models, across print, video, music, audio, television and communications industries means that regulation has to incorporate, as a primary objective, the fostering of innovation and investment in network facilities, as there is much less certainty than in the past.

Greater risk, all other things being equal, means less investment.

A new International Telecommunications Union broadband report incorporates a healthy measure of those perspectives.

“Service providers have struggled with legacy inherited laws and regulations that award licenses per service, and many companies have taken the issue to court – for example, cable TV companies seeking to provide telephone service over their networks, and telephone companies wanting to upgrade their networks to offer video programming services and compete with the cable companies,” the ITU report says.

“More modern approaches to regulation may be needed – such as converged regulation, simplifications to the licensing regime or unified licensing, where one unified license can allow any telecommunication company to provide any service, as long as consumer rights are protected, and the competitiveness of markets is not threatened,” the International Telecommunications Union broadband report suggests.

The historic division between regulation of communications and separate regulation for broadcasting was acceptable in the past when spectrum and telecommunications were clearly divided, and regulation of content was a major focus of any broadcasting agency, the ITU says.

With the shift of virtually all networks to Internet Protocol, virtually all networks can deliver any type of media. And that complicates any efforts to regulate media, broadcasting and communications separately.

The ITU study notes that policy-makers and regulators now must “stimulate” demand for broadband and in promote investment in infrastructure. That also requires a “balance” of technologies and policy approaches appropriate to specific situations, including more wireless effort.

The growth rate in global mobile data traffic is projected to grow 60 percent annually from 2011 to 2017, which will result in a 15-fold increase in traffic by 2017, mainly due to video traffic.

“Such an explosion in data traffic requires more spectrum,” the ITU says. In this regard,

policy-makers and regulators can help to create a supportive environment and encourage

investment and ensure sufficient availability of quality spectrum, the ITU says.

That “regulation by function” made sense at the time. As all networks become multi-purpose networks, the logic of regulating networks “by function or media type” is subverted. That necessarily raises huge issues that affect the foundation of contestant business models.

In a simple way, the issue is whether stricter common carrier rules should be applied to "less regulated" media, or whether less regulation should be applied to common carrier services.

Also, some would argue, the growing instability of all legacy revenue models, across print, video, music, audio, television and communications industries means that regulation has to incorporate, as a primary objective, the fostering of innovation and investment in network facilities, as there is much less certainty than in the past.

Greater risk, all other things being equal, means less investment.

A new International Telecommunications Union broadband report incorporates a healthy measure of those perspectives.

“Service providers have struggled with legacy inherited laws and regulations that award licenses per service, and many companies have taken the issue to court – for example, cable TV companies seeking to provide telephone service over their networks, and telephone companies wanting to upgrade their networks to offer video programming services and compete with the cable companies,” the ITU report says.

“More modern approaches to regulation may be needed – such as converged regulation, simplifications to the licensing regime or unified licensing, where one unified license can allow any telecommunication company to provide any service, as long as consumer rights are protected, and the competitiveness of markets is not threatened,” the International Telecommunications Union broadband report suggests.

The historic division between regulation of communications and separate regulation for broadcasting was acceptable in the past when spectrum and telecommunications were clearly divided, and regulation of content was a major focus of any broadcasting agency, the ITU says.

With the shift of virtually all networks to Internet Protocol, virtually all networks can deliver any type of media. And that complicates any efforts to regulate media, broadcasting and communications separately.

The ITU study notes that policy-makers and regulators now must “stimulate” demand for broadband and in promote investment in infrastructure. That also requires a “balance” of technologies and policy approaches appropriate to specific situations, including more wireless effort.

The growth rate in global mobile data traffic is projected to grow 60 percent annually from 2011 to 2017, which will result in a 15-fold increase in traffic by 2017, mainly due to video traffic.

“Such an explosion in data traffic requires more spectrum,” the ITU says. In this regard,

policy-makers and regulators can help to create a supportive environment and encourage

investment and ensure sufficient availability of quality spectrum, the ITU says.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wednesday, May 6, 2015

5G will Not Only Build on 4G, But on Cloud Computing, Virtualization and Big Data

As radical as it might seem, fifth generation mobile networks now have a design goal of eradicating the difference between access speed between fixed and mobile networks. Equally important, 5G thinking includes one millisecond end to end latency that will force a rethink of how all networks are designed and where computing activities occur.

Those requirements show how hard it will be to clearly delineate “cloud computing” from “big data” from “access networks” and “computing architecture.”

LIkewise, it will be hard to separate “fixed” from “mobile” access or “network functions virtualization” and “software defined networks” from “networks” in general.

Every one of those "silos" of thinking and practice will have to be integrated to achieve 5G objctives. At the same time, though much work lies ahead, it is possible to argue that 5G will be built on existing trends, and extrapolate logically from those trends. It is not so simple as saying "5G will be built on 4G."

It is more accurate to say that, if 5G objectives are met, 5G will be built on a variety of present trends, including cloud computing, big data, fast backhaul and fixed-mobile integration.

With the caveat that we might be overly aggressive in terms of our expectations for fifth generation mobile networks, a new International Telecommunications Union group looking at 5G fixed infrastructure shows just how much might be changing.

ITU has established a new Focus Group to identify the fixed network requirements for 5G.

The ITU notes that its IMT 2020 program already envisions “wireless communication to match the speed and reliability achieved by fibre-optic infrastructure.”

As others note, the next generation of potential apps will require extremely low latency--with a goal of one millisecond, end to end latency as the 5G design goal.

“One-millisecond end-to-end latency is necessary for technical systems to replicate natural human interaction with our environment, a goal that experts say should be within reach of future networks,” the ITU said.

“Air interfaces and radio access networks are progressing rapidly, but there is a need to devote more attention to the networking aspects of IMT-2020,” said ITU Secretary-General Houlin Zhao.

“Today’s network architectures cannot support the envisaged capabilities of IMT-2020 systems,” said Chaesub Lee, ITU Telecommunication Standardization Bureau director.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, November 6, 2012

One Thing Everybody Can Agree On: UN Shouldn't Control the Internet

The International Telecommunication Union (ITU) plans to hold a treaty conference, the World Conference on International Telecommunications, in December 2012, which will revise a 1988 treaty.

At stake are the ways communication network owners compensate each other for terminating international voice calls through the payment of settlements. But that is but one of many huge implications. Observers say the danger is direct controls on freedom of Internet expression.

The ITU is seeking to gain more control over Internet content. One reason is that countries such as Russia have called for restrictions over the internet where it is used to" interfere in the internal affairs of a state."

Opponents rightly say this represents a dramatic threat to the openness of the internet, where countries could regulate content not just within their own borders but globally.

But there are many practical business implications as well. The ITU proposes to change the way the Internet is governed, in ways that will harm the Internet by raising the cost and complexity of exchanging traffic, Analysys Mason researchers argue.

In part, the ITU wants to create a new Internet traffic “settlements regime” modeled on voice precedents that will be difficult to administer and raise overhead costs.

But there could be other significant effects. First, operators might be induced to maintain their customers‘ websites abroad. One of the significant benefits of establishing an internet exchange point is to make it attractive for domestic websites to be hosted at home, in order to increase their performance and lower costs, Analysys Mason notes.

However, given that foreign websites will generate a source of incoming settlements revenue, the incentive to keep them abroad would increase.

At the same time, foreign operators, in order to compensate for the higher settlements costs, would likely raise the price of hosting websites serving countries with high settlement rates.

While this could be seen to increase the incentives to locate content in the target country in order to avoid settlements, that is often not efficient, particularly for small or undeveloped markets from which access to a regional server may be sufficient, Analysys Mason argues.

In addition, it is likely that infrastructure investment decisions would be affected, as providers would be reluctant to invest in providing infrastructure to a particular country to which it is expensive to deliver traffic. In other words, there will be financial reasons not to build more undersea links to certain countries, for example.

Also, huge volumes of Internet traffic could be artificially generated in order to arbitrage a rate-regulated model, to generate inbound payments, alter traffic balances, or otherwise unfairly leverage any accounting rate regime that may be applied to the Internet.

Entities that believe they would be net recipients of settlements, based on current projections of traffic flows, might find themselves net payers as a result of the manipulation of traffic flows by other players. In other words, the incentives for arbitrage will increase.

Consider the flows of traffic. The notion of settlements is that a carrier that terminates traffic incurs costs to deliver that traffic. So a sending carrier pays the terminating carrier. In many cases, the traffic flows should largely balance each other, so the net payments are relatively small in magnitude.

But there are scenarios where traffic is unbalanced, and that causes problems. In the voice settlement regime, carriers that accept more traffic than they send wind up paying money. Carriers that send more traffic than they receive make money.

Some of you will remember, or even be able to point to, instances where revenue arbitrage was possible precisely because of such asymmetrical traffic flows. Server farms and “free conference calling services” in the United States provide examples.

In the proposed ITU framework, it is server farm traffic that could be troubling for some carriers.

Multimedia content, for example, might represent as much as 98 percent of Internet traffic. Right now, where those servers are located does not have implications for inter-carrier settlements.

For cost reasons, many of those servers are located in Africa. In 1999, 70 percent of international Internet bandwidth originating in Africa went to the United States. In 2011, less than five percent goes to the United States.

These days, content is stored at African server farms, for distribution largely to Africa, Analysys Mason notes. In some ways, that is helpful to African consumers, for quality and cost reasons. In other ways, high cross-border charges are unhelpful.

While it is true that IXPs are emerging to facilitate local exchange of traffic in Africa, the cost of cross-border connectivity between many African countries is still quite high, and this is hindering the emergence of regional IXPs to help exchange traffic and distribute content.

The bandwidth from Latin America presents the same broad picture. Between 1999 and 2011, the percentage of bandwidth going to the United States fell from just under 90 percent to 85 percent, replaced by more intra-regional traffic.

The main similarities between Africa and Latin America are that over 80 percent of their Internet bandwidth is connected to another region (Europe and the US respectively). At the same time, little bandwidth goes between countries within the region. Intra-Latin American traffic is 15 percent of total, while intra-African traffic is two percent.

In ways directly related to human freedom, the free flow of information and the cost of getting information anywhere on the planet, U.N. governance of the Internet would be harmful.

At stake are the ways communication network owners compensate each other for terminating international voice calls through the payment of settlements. But that is but one of many huge implications. Observers say the danger is direct controls on freedom of Internet expression.

The ITU is seeking to gain more control over Internet content. One reason is that countries such as Russia have called for restrictions over the internet where it is used to" interfere in the internal affairs of a state."

Opponents rightly say this represents a dramatic threat to the openness of the internet, where countries could regulate content not just within their own borders but globally.

But there are many practical business implications as well. The ITU proposes to change the way the Internet is governed, in ways that will harm the Internet by raising the cost and complexity of exchanging traffic, Analysys Mason researchers argue.

In part, the ITU wants to create a new Internet traffic “settlements regime” modeled on voice precedents that will be difficult to administer and raise overhead costs.

But there could be other significant effects. First, operators might be induced to maintain their customers‘ websites abroad. One of the significant benefits of establishing an internet exchange point is to make it attractive for domestic websites to be hosted at home, in order to increase their performance and lower costs, Analysys Mason notes.

However, given that foreign websites will generate a source of incoming settlements revenue, the incentive to keep them abroad would increase.

At the same time, foreign operators, in order to compensate for the higher settlements costs, would likely raise the price of hosting websites serving countries with high settlement rates.

While this could be seen to increase the incentives to locate content in the target country in order to avoid settlements, that is often not efficient, particularly for small or undeveloped markets from which access to a regional server may be sufficient, Analysys Mason argues.

In addition, it is likely that infrastructure investment decisions would be affected, as providers would be reluctant to invest in providing infrastructure to a particular country to which it is expensive to deliver traffic. In other words, there will be financial reasons not to build more undersea links to certain countries, for example.

Also, huge volumes of Internet traffic could be artificially generated in order to arbitrage a rate-regulated model, to generate inbound payments, alter traffic balances, or otherwise unfairly leverage any accounting rate regime that may be applied to the Internet.

Entities that believe they would be net recipients of settlements, based on current projections of traffic flows, might find themselves net payers as a result of the manipulation of traffic flows by other players. In other words, the incentives for arbitrage will increase.

Consider the flows of traffic. The notion of settlements is that a carrier that terminates traffic incurs costs to deliver that traffic. So a sending carrier pays the terminating carrier. In many cases, the traffic flows should largely balance each other, so the net payments are relatively small in magnitude.

But there are scenarios where traffic is unbalanced, and that causes problems. In the voice settlement regime, carriers that accept more traffic than they send wind up paying money. Carriers that send more traffic than they receive make money.

Some of you will remember, or even be able to point to, instances where revenue arbitrage was possible precisely because of such asymmetrical traffic flows. Server farms and “free conference calling services” in the United States provide examples.

In the proposed ITU framework, it is server farm traffic that could be troubling for some carriers.

Multimedia content, for example, might represent as much as 98 percent of Internet traffic. Right now, where those servers are located does not have implications for inter-carrier settlements.

For cost reasons, many of those servers are located in Africa. In 1999, 70 percent of international Internet bandwidth originating in Africa went to the United States. In 2011, less than five percent goes to the United States.

These days, content is stored at African server farms, for distribution largely to Africa, Analysys Mason notes. In some ways, that is helpful to African consumers, for quality and cost reasons. In other ways, high cross-border charges are unhelpful.

While it is true that IXPs are emerging to facilitate local exchange of traffic in Africa, the cost of cross-border connectivity between many African countries is still quite high, and this is hindering the emergence of regional IXPs to help exchange traffic and distribute content.

The bandwidth from Latin America presents the same broad picture. Between 1999 and 2011, the percentage of bandwidth going to the United States fell from just under 90 percent to 85 percent, replaced by more intra-regional traffic.

The main similarities between Africa and Latin America are that over 80 percent of their Internet bandwidth is connected to another region (Europe and the US respectively). At the same time, little bandwidth goes between countries within the region. Intra-Latin American traffic is 15 percent of total, while intra-African traffic is two percent.

In ways directly related to human freedom, the free flow of information and the cost of getting information anywhere on the planet, U.N. governance of the Internet would be harmful.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, December 15, 2012

The 3% Rule for Pricing Broadband Access Services, Anywhere

Why are broadband access prices so different, around the world? There's a simple answer, actually: retail prices are directly related to cost of construction in each market, and also substantially directly related to median household income.

You might think "things cost what they cost," and that is true, but what things cost varies from place to place

Recent studies published by ITU reveal that broadband penetration is directly related to its cost, relative to an average family income, as well as to the availability of products and services that accommodate the general population’s purchasing ability.

That also explains why high speed access costs vary rather broadly from country to country. Areas where it costs more to create the infrastructure will tend to be more expensive, at the retail level. Areas where it costs less to create networks will correlate with lower retail costs.

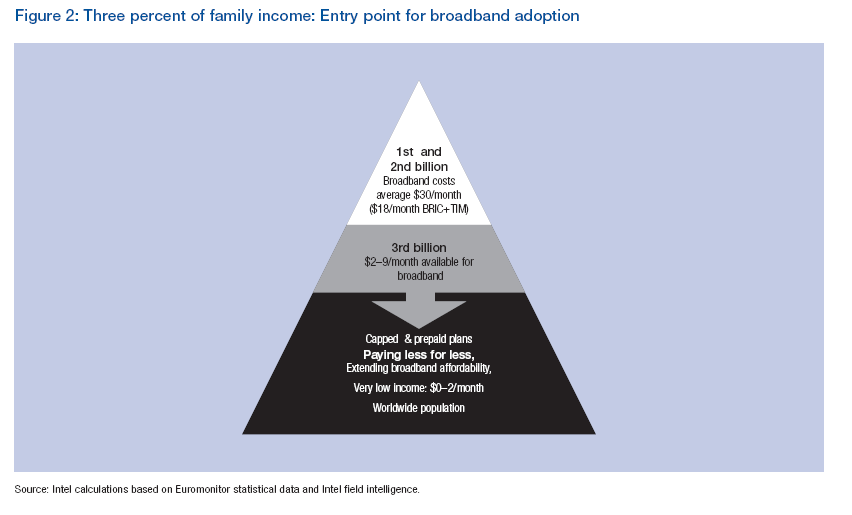

For example, as the annual cost of broadband drops below three percent of a family’s annual income, broadband usage begins to increase dramatically.

For developed countries, this relative cost has already been achieved, but for at least 34 countries worldwide, the cost of broadband remains higher than the average annual family income, the ITU says.

But that’s an important bit of retail pricing advice for would-be ISPs in developing regions: set monthly prices no higher than three percent of median household income.

And prices are falling, globally.Between 2008 and 2009, 125 countries saw reductions in access prices, some by as much as 80 percent, the ITU says. Between 2009 and 2011, for example, prices for fixed broadband have dropped by 52.2 percent on average and mobile broadband prices by 22 percent, globally.

Affordable broadband programs are starting to emerge in countries such as Sri Lanka and India, with service providers offering connectivity solutions starting as low as US$2 per month.

And while it is natural for a seller to want higher prices, for Internet access providers, less is more, in the sense of keeping at or below the “three percent of median household income” rule for retail pricing.

The trade-off is lower average revenue per user, but many more users. So where median high speed access costs in developed regions might run about $30 a month, in the BRIC+TIM areas costs might be $18 a month.

Somewhere between $2 and $9 a month would reach another billion or so households in a number of regions and countries. In the poorest nations, prepaid plans costing less than $2 a month will be needed.

Brazil, Russia, India, China, Turkey, Indonesia, and Mexico (BRIC+TIM countries), for example, could grow their available market by 860 million people by reducing the cost of entry for broadband by about 50 percent..

In 2011, the price of fixed broadband access cost less than two percent of average monthly income in 49 economies in the world, mostly in the industrialized world.

Meanwhile, broadband access cost more than half of average national income in 30 economies. In 19 of the lesser developed countries, the price of broadband exceeds average monthly income.

By 2011, there were 48 developing economies where entry-level broadband access cost less than five percent of average monthly income, up from just 35 countries the year before.

To take the example of Kenya, family income levels mean that only about seven percent of the population can afford a service that offers uncapped monthly broadband access for US$20 per month. A prepaid broadband access service capped at 200 MB of data for US$5, however, could be within the reach of more than 60 percent of the Kenyan population.

Safaricom, the largest Internet service provider in Kenya, launched a segmented prepaid broadband offer in the end of 2009 targeted at different income levels.

There were 589 million fixed broadband subscriptions by the end of 2011 (most of which were located in the developed world), but nearly twice as many mobile broadband subscriptions at 1.09 billion, the ITU says.

Beyond that, since trenches, ducts and dark fiber represent as much as 70 percent of total cost to build a broadband network, the wisdom of using wireless is obvious. Wireless attacks that part of the effort consuming up to 70 percent of capital investment.

You might think "things cost what they cost," and that is true, but what things cost varies from place to place

Recent studies published by ITU reveal that broadband penetration is directly related to its cost, relative to an average family income, as well as to the availability of products and services that accommodate the general population’s purchasing ability.

That also explains why high speed access costs vary rather broadly from country to country. Areas where it costs more to create the infrastructure will tend to be more expensive, at the retail level. Areas where it costs less to create networks will correlate with lower retail costs.

For example, as the annual cost of broadband drops below three percent of a family’s annual income, broadband usage begins to increase dramatically.

For developed countries, this relative cost has already been achieved, but for at least 34 countries worldwide, the cost of broadband remains higher than the average annual family income, the ITU says.

But that’s an important bit of retail pricing advice for would-be ISPs in developing regions: set monthly prices no higher than three percent of median household income.

And prices are falling, globally.Between 2008 and 2009, 125 countries saw reductions in access prices, some by as much as 80 percent, the ITU says. Between 2009 and 2011, for example, prices for fixed broadband have dropped by 52.2 percent on average and mobile broadband prices by 22 percent, globally.

Affordable broadband programs are starting to emerge in countries such as Sri Lanka and India, with service providers offering connectivity solutions starting as low as US$2 per month.

And while it is natural for a seller to want higher prices, for Internet access providers, less is more, in the sense of keeping at or below the “three percent of median household income” rule for retail pricing.

The trade-off is lower average revenue per user, but many more users. So where median high speed access costs in developed regions might run about $30 a month, in the BRIC+TIM areas costs might be $18 a month.

Somewhere between $2 and $9 a month would reach another billion or so households in a number of regions and countries. In the poorest nations, prepaid plans costing less than $2 a month will be needed.

Brazil, Russia, India, China, Turkey, Indonesia, and Mexico (BRIC+TIM countries), for example, could grow their available market by 860 million people by reducing the cost of entry for broadband by about 50 percent..

In 2011, the price of fixed broadband access cost less than two percent of average monthly income in 49 economies in the world, mostly in the industrialized world.

Meanwhile, broadband access cost more than half of average national income in 30 economies. In 19 of the lesser developed countries, the price of broadband exceeds average monthly income.

By 2011, there were 48 developing economies where entry-level broadband access cost less than five percent of average monthly income, up from just 35 countries the year before.

To take the example of Kenya, family income levels mean that only about seven percent of the population can afford a service that offers uncapped monthly broadband access for US$20 per month. A prepaid broadband access service capped at 200 MB of data for US$5, however, could be within the reach of more than 60 percent of the Kenyan population.

Safaricom, the largest Internet service provider in Kenya, launched a segmented prepaid broadband offer in the end of 2009 targeted at different income levels.

There were 589 million fixed broadband subscriptions by the end of 2011 (most of which were located in the developed world), but nearly twice as many mobile broadband subscriptions at 1.09 billion, the ITU says.

Beyond that, since trenches, ducts and dark fiber represent as much as 70 percent of total cost to build a broadband network, the wisdom of using wireless is obvious. Wireless attacks that part of the effort consuming up to 70 percent of capital investment.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, May 14, 2012

Is There a Mobile Broadband "Divide" That Cannot be Fixed Rapidly by the Market?

Policymakers, it might be argued, should try to solve real problems, not imagined problems.

Policymakers, it might be argued, should try to solve real problems, not imagined problems.Likewise, policymakers and regulators sometimes should be encouraged to avoid mucking about when key problems already are being resolved.

Sometimes, "doing nothing," or perhaps "not getting in the way" is the right course of action. That would seem to be the case for global mobile broadband services, despite the

contention of some International Telecommunication Union researchers that a big problem exists.

“As the broadband revolution unfolds, large segments of the world’s population are being left

behind,” the International Telecommunications Union argues.

Oddly, other ITU data suggests that mobile broadband adoption is growing rapidly.

The ITU rightly suggests that “over five billion people have never experienced the Internet or have only experienced it through public or shared access, let alone experienced the Internet through broadband access.”

The ITU rightly suggests that “over five billion people have never experienced the Internet or have only experienced it through public or shared access, let alone experienced the Internet through broadband access.”But the ITU also has said that a third of the world’s seven billion people now use the Internet. Over the last five years (2006 to 2011), developing countries have increased their share of the world’s total number of Internet users from 44 percent in 2006 to 62 percent in 2011.

The logical and natural implication is that as Internet usage gradually shifts to broadband modes, users in all markets also will shift their usage in the same direction.

In fact, mobile voice adoption accomplished in less than a decade what policymakers had fretted over for many decades, namely the issue of how to provide phone service to human beings in the developed world. That no longer is a significant issue, and the problem was solved with minimal action by global regulators.

The ITU notes that there are 5.9 billion mobile subscriptions now in use, representing mobile penetration of 87 percent overall and 79 percent in the developing world. The next issue will be broadband service, but the previous success with voice suggests the broadband problem is anything but insurmountable.

The ITU notes that there are 5.9 billion mobile subscriptions now in use, representing mobile penetration of 87 percent overall and 79 percent in the developing world. The next issue will be broadband service, but the previous success with voice suggests the broadband problem is anything but insurmountable. Mobile broadband subscriptions have grown 45 percent annually over the last four years and today there are twice as many mobile broadband as fixed broadband subscriptions. Though much of that activity occurs in the developed world, there is no particular reason to believe broadband will not be adopted rapidly in developing regions as well.

So the notion that people anywhere in the world “are being left behind” completely misses the rapid adoption of mobile services by all users, everywhere, at a pace regulators might have found “impossible.”

To be sure, broadband adoption has not yet reached the levels of mobile use. But few believe there is any fundamental reason why that will not continue to evolve at a rapid rate, everywhere.

To be sure, broadband adoption has not yet reached the levels of mobile use. But few believe there is any fundamental reason why that will not continue to evolve at a rapid rate, everywhere. It is one matter to note that, at the moment, “there is a wide disparity in broadband access around the world, both within countries and between countries.” It is quite another matter to make the argument that structural barriers are so significant that consumer demand and supplier cleverness cannot fill the gap quickly.

Without diminishing some important role for regulators in the telecommunications business, once again it seems regulators are far behind the curve.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, November 25, 2018

Are Telecom Prices Too High?

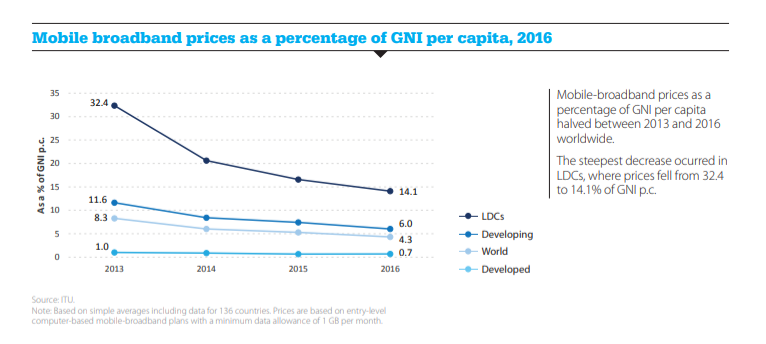

One argument we always hear about any communications service is that it is “too expensive.” That clearly is true in developing or lesser-developed nations, where mobile internet access can cost 14 percent of gross national income per person. In developing markets, mobile internet access can cost about six percent of GNI, per person.

Consider mobile internet access. In developing countries, mobile internet access costs about 0.7 percent of gross national income, per person, according to International Telecommunications Union data.

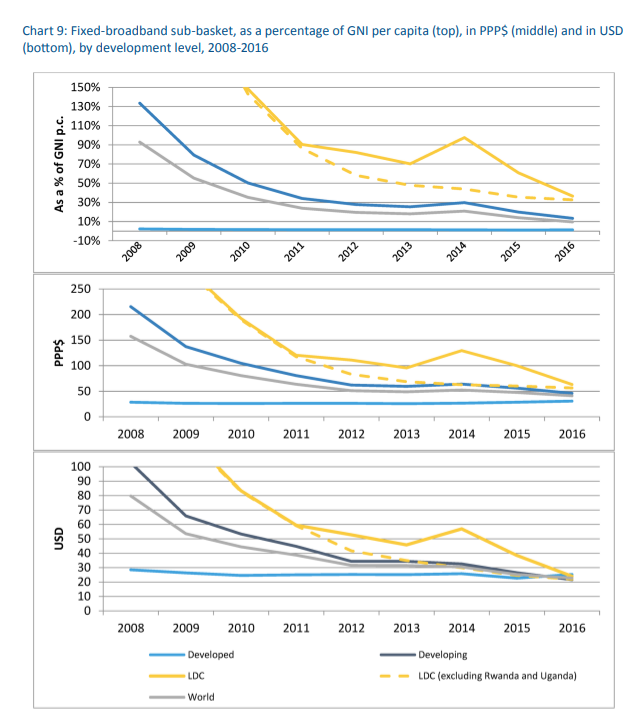

Much the same story holds for fixed network internet access as well. Fixed network internet access in developed nations costs less than one percent of GNI per person, perhaps 11 percent of GNI per person in developing nations and as much as 30 percent of GNI per person in lesser-developed nations.

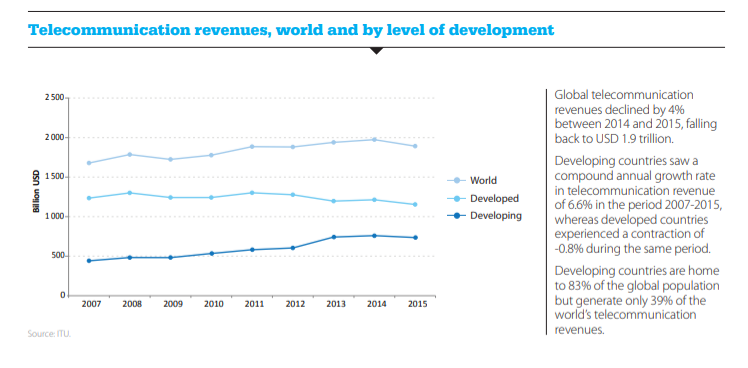

One rather impressionistic bit of evidence that prices are not excessive might be gleaned from industry profits. On a global basis, revenues dropped by about four percent between 2014 and 2015, for example.

Developed market revenues have been dropping since about 2012, according to ITU statistics.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, September 18, 2012

New Wave of Internet Arbitrage Coming?

The International Telecommunication Union (ITU) plans to hold a treaty conference, the World Conference on International Telecommunications, in December 2012, which will revise a 1988 treaty, the International Telecommunication Regulations (ITR). At stake are the ways communication network owners compensate each other for terminating international voice calls through the payment of settlements.

But there are wider implications. The ITU proposes to change the way the Internet is governed, in ways that will harm the Internet by raising the cost and complexity of exchanging traffic, Analysys Mason researchers argue. Basically, the ITU wants to create a new Internet traffic “settlements regime” modeled on voice precedents that will be difficult to administer and raise overhead costs.

But there could be other significant effects. First, operators might be induced to maintain their customers‘ websites abroad. One of the significant benefits of establishing an internet exchange point is to make it attractive for domestic websites to be hosted at home, in order to increase their performance and lower costs, Analysys Mason notes.

However, given that foreign websites will generate a source of incoming settlements, the incentive to keep them abroad would increase.

At the same time, foreign operators, in order to compensate for the settlements, would likely raise the price of hosting websites serving countries with high settlement rates, which might lead websites to develop less content targeted at a particular country in order to limit their costs.

While this could be seen to increase the incentives to locate content in the target country in order to avoid settlements, that is often not efficient, particularly for small or undeveloped markets from which access to a regional server may be sufficient, Analysys Mason argues.

In addition, it is likely that infrastructure investment decisions would be affected, as providers would be reluctant to invest in providing infrastructure to a particular country to which it is expensive to deliver traffic. In other words, there will be financial reasons not to build more undersea links to certain countries, for example.

Also, huge volumes of Internet traffic could be artificially generated in order to arbitrage a rate-regulated model, to generate inbound payments, alter traffic balances, or otherwise unfairly leverage any accounting rate regime that may be applied to the Internet.

Entities that believe they would be net recipients of settlements, based on current projections of traffic flows, might find themselves net payers as a result of the manipulation of traffic flows by other players.

In summary, aside from the intrinsic difficulties of successfully imposing regulations on international flows of Internet traffic, there could be unintended consequences that would harm the internet if such a system were imposed.

If history, human nature and self interest is any guide, some service providers to try and lower settlement payments, while others will attempt to grow their share of settlement payments.

Consider the flows of traffic. The notion of settlements is that a carrier that terminates traffic incurs costs to deliver that traffic. So a sending carrier pays the terminating carrier. In many cases, the traffic flows should largely balance each other, so the net payments are relatively small in magnitude.

But there are scenarios where traffic is unbalanced, and that causes problems. In the voice settlement regime, carriers that accept more traffic than they send wind up paying money. Carriers that send more traffic than they receive make money.

Some of you will remember, or even be able to point to, instances where revenue arbitrage was possible precisely because of such asymmetrical traffic flows. Server farms and “free conference calling services” in the United States provide examples.

In the proposed ITU framework, it is server farm traffic that could be troubling for some carriers.

Multimedia content, for example, might represent as much as 98 percent of Internet traffic. Right now, where those servers are located does not have implications for inter-carrier settlements.

For cost reasons, many of those servers are located in Africa. In 1999, 70 percent of international Internet bandwidth originating in Africa went to the United States. In 2011, less than five percent goes to the United States.

These days, content is stored at African server farms, for distribution largely to Africa, Analysys Mason notes. In some ways, that is helpful to African consumers, for quality and cost reasons. In other ways, high cross-border charges are unhelpful.

While it is true that IXPs are emerging to facilitate local exchange of traffic in Africa, the cost of cross-border connectivity between many African countries is still quite high, and this is hindering the emergence of regional IXPs to help exchange traffic and distribute content.

The bandwidth from Latin America presents the same broad picture. Between 1999 and 2011, the percentage of bandwidth going to the United States fell from just under 90 percent to 85 percent, replaced by more intra-regional traffic.

The main similarities between Africa and Latin America are that over 80 percent of their Internet bandwidth is connected to another region (Europe and the US respectively). At the same time, little bandwidth goes between countries within the region. Intra-Latin American traffic is 15 percent of total, while intra-African traffic is two percent.

The amount of cost-increasing overhead under any new settlement regime could be significant.

A recent study by the Packet-Clearing House analyzed 142,210 peering agreements representing 86 percent of global Internet carriers and 96 countries.

Only 698 of the peering agreements were based on written contracts, representing just 0.49 percent of all the contracts.

In other words, the vast majority of current international and domestic peering agreements are not just commercially negotiated, but are not even formalized in writing. If Internet settlements mirror voice practices, overall costs will rise, even if traffic flows can be accurately captured most of the time, and some say that will be very difficult.

Analysys Mason argues market-based mechanisms work, and are a better alternative to creating a new settlement regime modeled on voice principles.

But there are wider implications. The ITU proposes to change the way the Internet is governed, in ways that will harm the Internet by raising the cost and complexity of exchanging traffic, Analysys Mason researchers argue. Basically, the ITU wants to create a new Internet traffic “settlements regime” modeled on voice precedents that will be difficult to administer and raise overhead costs.

But there could be other significant effects. First, operators might be induced to maintain their customers‘ websites abroad. One of the significant benefits of establishing an internet exchange point is to make it attractive for domestic websites to be hosted at home, in order to increase their performance and lower costs, Analysys Mason notes.

However, given that foreign websites will generate a source of incoming settlements, the incentive to keep them abroad would increase.

At the same time, foreign operators, in order to compensate for the settlements, would likely raise the price of hosting websites serving countries with high settlement rates, which might lead websites to develop less content targeted at a particular country in order to limit their costs.

While this could be seen to increase the incentives to locate content in the target country in order to avoid settlements, that is often not efficient, particularly for small or undeveloped markets from which access to a regional server may be sufficient, Analysys Mason argues.

In addition, it is likely that infrastructure investment decisions would be affected, as providers would be reluctant to invest in providing infrastructure to a particular country to which it is expensive to deliver traffic. In other words, there will be financial reasons not to build more undersea links to certain countries, for example.

Also, huge volumes of Internet traffic could be artificially generated in order to arbitrage a rate-regulated model, to generate inbound payments, alter traffic balances, or otherwise unfairly leverage any accounting rate regime that may be applied to the Internet.

Entities that believe they would be net recipients of settlements, based on current projections of traffic flows, might find themselves net payers as a result of the manipulation of traffic flows by other players.

In summary, aside from the intrinsic difficulties of successfully imposing regulations on international flows of Internet traffic, there could be unintended consequences that would harm the internet if such a system were imposed.

If history, human nature and self interest is any guide, some service providers to try and lower settlement payments, while others will attempt to grow their share of settlement payments.

Consider the flows of traffic. The notion of settlements is that a carrier that terminates traffic incurs costs to deliver that traffic. So a sending carrier pays the terminating carrier. In many cases, the traffic flows should largely balance each other, so the net payments are relatively small in magnitude.

But there are scenarios where traffic is unbalanced, and that causes problems. In the voice settlement regime, carriers that accept more traffic than they send wind up paying money. Carriers that send more traffic than they receive make money.

Some of you will remember, or even be able to point to, instances where revenue arbitrage was possible precisely because of such asymmetrical traffic flows. Server farms and “free conference calling services” in the United States provide examples.

In the proposed ITU framework, it is server farm traffic that could be troubling for some carriers.

Multimedia content, for example, might represent as much as 98 percent of Internet traffic. Right now, where those servers are located does not have implications for inter-carrier settlements.

For cost reasons, many of those servers are located in Africa. In 1999, 70 percent of international Internet bandwidth originating in Africa went to the United States. In 2011, less than five percent goes to the United States.

These days, content is stored at African server farms, for distribution largely to Africa, Analysys Mason notes. In some ways, that is helpful to African consumers, for quality and cost reasons. In other ways, high cross-border charges are unhelpful.

While it is true that IXPs are emerging to facilitate local exchange of traffic in Africa, the cost of cross-border connectivity between many African countries is still quite high, and this is hindering the emergence of regional IXPs to help exchange traffic and distribute content.

The bandwidth from Latin America presents the same broad picture. Between 1999 and 2011, the percentage of bandwidth going to the United States fell from just under 90 percent to 85 percent, replaced by more intra-regional traffic.

The main similarities between Africa and Latin America are that over 80 percent of their Internet bandwidth is connected to another region (Europe and the US respectively). At the same time, little bandwidth goes between countries within the region. Intra-Latin American traffic is 15 percent of total, while intra-African traffic is two percent.

The amount of cost-increasing overhead under any new settlement regime could be significant.

A recent study by the Packet-Clearing House analyzed 142,210 peering agreements representing 86 percent of global Internet carriers and 96 countries.

Only 698 of the peering agreements were based on written contracts, representing just 0.49 percent of all the contracts.

In other words, the vast majority of current international and domestic peering agreements are not just commercially negotiated, but are not even formalized in writing. If Internet settlements mirror voice practices, overall costs will rise, even if traffic flows can be accurately captured most of the time, and some say that will be very difficult.

Analysys Mason argues market-based mechanisms work, and are a better alternative to creating a new settlement regime modeled on voice principles.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...