It has become the conventional wisdom that there is no "killer app" for fourth-generation mobile networks. Orange's LTE/EPC Program Director Rémi Thomas says "LTE is not driven by a killer application, but it will essentially be driven by capacity needs," said Thomas. No Killer App for LTE

It might be more accurate to say there is, at present, no stand-out killer app for 4G networks. Some think if such an app is possible, it will emerge, rather than being "planned for." Killer app is a myth

But it would be odd, perhaps almost unprecedented, for 4G mobile networks to succeed wildly, which is what virtually everybody expects, without the emergence of some new qualitatively different experience or value driver.

It might be more important to say that "nobody knows" what such qualitatively-new experiences will emerge. But some find say it is unlikely 4G will remain "3G but faster." Some might suspect that 4G will lead to new apps that we originally believed would happen on 3G networks.

About a decade ago, when the first commercial 3G networks were introduced, there was much talk about innovation and new applications the networks would enable, and the list looked remarkably similar to what people claim will happen with 4G. 3G history

E-commerce apps, for example, were thought to be an important 3G innovation. That is claimed for 4G as well, with more conviction, perhaps. “The availability of 3G services is going to have a profound effect on electronic commerce,” it was said.

That also is said of 4G. It was said that “3G works better” than 2G, and that was true. It also is said of 4G, and also is true.

3G wireless was sometimes characterized as a wireless version of the Internet, encompassing Web browsing, e-mail and media downloads. That sounds like 4G as well.

Over time, though, a distinctive lead application does tend to develop, though it might take some time. Voice and texting were the lead apps for 2G, while Internet access and email have emerged as the "killer app" for 3G, it can be argued.

Exactly how 4G products and services evolve is highly uncertain at this time and very similar to when wireless operators first deployed 3G networks, Fitch Ratings has argued.

For 3G networks, the industry did not offer a good view of this until smart phones, in particular the iPhone and other similarly oriented devices, drove significant consumer uptake for broadband data, as opposed to the earlier growth provided by 2G email services.

Longer term, Fitch expects the majority of operators should achieve data device penetration rates of at least 70 percent to 80 percent. If so, mobile broadband will collectively represent the killer app for 3G. But what about 4G? Is it just "3G with more speed," or something else?

Fitch expects that 4G services will likewise be defined by innovative devices, perhaps tablet oriented, with new content applications, including video that will drive significantly increased demand for data. If so, 4G might ultimately be different from 3G in providing a platform for different types of end user experiences.

There is a line of thinking that the value of 4G might initially accrue in large part from significantly-lower the cost per-bit costs to provide mobile broadband. Verizon Wireless, for example, believes the cost to deliver a megabyte of data on 4G with LTE will be half to a third of the costs of a 3G network.

But if the 4G experience is anything like what we've seen with 3G, it might take years for the answer to be found.

Showing posts with label 4G. Show all posts

Showing posts with label 4G. Show all posts

Wednesday, December 7, 2011

Is There a Killer App for LTE?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, November 8, 2011

Verizon to double data amounts for 4G smart phones

Customers buying smart phones running on the Verizon Wireless Long Term Evolution 4G network will get double the data buckets for as long as they keep their level of service.

Customers buying smart phones running on the Verizon Wireless Long Term Evolution 4G network will get double the data buckets for as long as they keep their level of service.

For example, someone who subscribes to the 2GB for $30 plan will receive 4GB instead. For $50 you can get 10GB instead of 5GB, and for $80 you can get 20GB instead of 10GB per month.

Existing customers (those who have upgraded their service or purchased a 4G smartphone within the last 14 days) will have to request the change. Verizon to double data amounts for 4G smart phones

Verizon Wireless apparently says the bigger data plans will stay in effect so long as users keep a smart phone plan.

The nice thing about a brand-new wireless network is that, at first, there aren't too many customers to clog up the pipes, allowing service providers to do these sorts of deals.

The nice thing about a brand-new wireless network is that, at first, there aren't too many customers to clog up the pipes, allowing service providers to do these sorts of deals.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, November 3, 2011

Verizon API Will "Turbo" Mobile Broadband

Verizon will publish an application programming interface that could allow mobile consumers to "turbocharge" the network bandwidth their smartphone apps use, presumably for a small additional fee.

Verizon will publish an application programming interface that could allow mobile consumers to "turbocharge" the network bandwidth their smartphone apps use, presumably for a small additional fee.

"I think one of the things that you could do is guaranteed quality of service," said Hugh Fletcher, associate director for technology in Verizon's Product Development and Technology team.

"One of the things that we are right now is very democratic in terms of allocating spectrum and bandwidth to users. And just because you request a high quality of service doesn't mean you're gonna get it. [The network] will try to give it to you, but if there's a lot of congestion, a lot of people using it, it won't kick people off," said Fletcher. Verizon API To Give Apps 'Turbo'

The network optimization API will likely expose attributes like jitter, latency, bandwidth, and priority to app developers, Fletcher said.

Despite expected complaints from some network neutrality advocates, there is a reason such an API might provide clear value to end users. Some of you might be using 3G or 4G networks, using different air interfaces, to use interactive cloud applications. If you do that often enough, on many networks, you will have discovered the experience problem caused by latency.

Where older GPRS or EDGE data networks featured round-trip latencies in the 600 millisecond to 700 msec. range, LTE networks feature round-trip latencies in the 50 msec. range.

One of the important elements of a cloud-delivered application experience is latency performance, even though we most often think of "bandwidth" as being the key "experience" parameter.

Some might say the key benefits will be for gaming apps, but many of us can assure you that other interactive apps, even those not intrinsically dependent on "real time" protocols, can suffer from mobile latency. Latency issues

Despite expected complaints from some network neutrality advocates, there is a reason such an API might provide clear value to end users. Some of you might be using 3G or 4G networks, using different air interfaces, to use interactive cloud applications. If you do that often enough, on many networks, you will have discovered the experience problem caused by latency.

Where older GPRS or EDGE data networks featured round-trip latencies in the 600 millisecond to 700 msec. range, LTE networks feature round-trip latencies in the 50 msec. range.

One of the important elements of a cloud-delivered application experience is latency performance, even though we most often think of "bandwidth" as being the key "experience" parameter.

Some might say the key benefits will be for gaming apps, but many of us can assure you that other interactive apps, even those not intrinsically dependent on "real time" protocols, can suffer from mobile latency. Latency issues

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, November 1, 2011

Clearwire to Stop Selling Sprint 3G

Clearwire has stopped offering postpaid plans to new customers and will no longer sell dual-mode WiMAX/3G devices that use Sprint's CDMA network. Sprint, for its part, says it will not sell Clearwire WiMAX phones after 2012. Clearwire dumps Sprint 3G

Clearwire has stopped offering postpaid plans to new customers and will no longer sell dual-mode WiMAX/3G devices that use Sprint's CDMA network. Sprint, for its part, says it will not sell Clearwire WiMAX phones after 2012. Clearwire dumps Sprint 3G The moves clearly point to a shift by both carriers to Long Term Evolution. Sprint's shift away from WiMAX, and Clearwire's shift away from 3G both mean each carrier is free to emphasize Long Term Evolution services expected to be offered on both networks as the "preferred" 4G network, going forward.

Sprint Nextel Corp. says it will stop selling phones and other devices compatible with Clearwire Corp.'s network at the end of 2012, as it switches customers to its own Long Term Evolution network.

It is possible to paint the picture as a sign of deteriorating relations between Sprint and Clearwire, but a shift to 4G and LTE is the real meaning of the changes. Sprint is carving out LTE capacity from its own 3G spectrum, while Clearwire needs to build an entirely new LTE network using spectrum it might otherwise devote to WiMAX.

Also, as Clearwire shifts away from a dual role as both a wholesaler of capacity and a retail brand, it has to be cognizant of what its wholesale customers want, and Sprint, Clearwire's top customer, clearly is signaling it wants LTE plus CDMA to be the preferred "dual mode" approach it prefers.

The irony is that Sprint owns a majority of Clearwire. Sprint to halt WiMAX sales

It is possible to paint the picture as a sign of deteriorating relations between Sprint and Clearwire, but a shift to 4G and LTE is the real meaning of the changes. Sprint is carving out LTE capacity from its own 3G spectrum, while Clearwire needs to build an entirely new LTE network using spectrum it might otherwise devote to WiMAX.

Also, as Clearwire shifts away from a dual role as both a wholesaler of capacity and a retail brand, it has to be cognizant of what its wholesale customers want, and Sprint, Clearwire's top customer, clearly is signaling it wants LTE plus CDMA to be the preferred "dual mode" approach it prefers.

The irony is that Sprint owns a majority of Clearwire. Sprint to halt WiMAX sales

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, October 24, 2011

Cable Deal for T-Mobile USA?

With the Justice Department having filed suit to block the proposed AT&T purchase of T-Mobile USA, what is T-Mobile's plan if the deal falls through? It doesn't appear that T-Mobile USA actually has had a "plan B." But many speculate that if the AT&T acquisition is blocked, it will also signal that Sprint will not be allowed to buy T-Mobile USA, either.

Bernstein Research senior analysts Robin Bienenstock and Craig Moffett say the most likely scenario is not a Sprint merger but a spectrum deal with cable operators Comcast and Time Warner, both of which own spectrum T-Mobile USA could use to launch LTE services. The cable operators could monetize their spectrum and provide backhaul services.

That will leave T-Mobile USA in a tough position, as it needs spectrum to launch Long Term Evolution, and will emerge from the merger process weakened in the retail market.

Bernstein Research senior analysts Robin Bienenstock and Craig Moffett say the most likely scenario is not a Sprint merger but a spectrum deal with cable operators Comcast and Time Warner, both of which own spectrum T-Mobile USA could use to launch LTE services. The cable operators could monetize their spectrum and provide backhaul services.

To the extent that cable operators sell a wholesale service, they might then use T-Mobile USA rather than Clearwire. That would be more bad news for Clearwire.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Is "4G Plus DirecTV" a Viable Alternative to FiOS?

Verizon Wireless seems to be cooking up an out of market “video plus broadband” plan, working with DirecTV. During its recent quarterly earnings report, Fran Shammo, Verizon Communications EVP said that the company was working on such an effort.

“You're going to see that come in the fourth quarter with the what we now call the Cantenna, which is not a commercial name obviously, but it's the antenna that we actually trialed with DIRECTV, which was extremely successful,” said Shammo.

Some will legitimately wonder whether that approach might even wind up being used in some Verizon markets where FiOS has not already started to be deployed. LTE plus DirecTV

There are some significant Verizon markets including cities like Boston, Buffalo, N.Y, Baltimore and Alexandria, Va. where FiOS construction has not started.

The obvious new question is the rational approach Verizon should take to upgrading its fixed-line network. There isn’t much doubt about optical access media being more resistant to some weather-related impairments than copper networks, nor is there much doubt that new optical facilities cost less to maintain than older copper networks.

But the business question is how much incremental investment ought to be made in the fixed network, if video and broadband services can be provided using the wireless network. One might rationally argue that the cost of maintaining the fourth generation wireless network is lower than the cost of maintaining the FiOS network.

Obviously, if that is true then the avoided capital investment in new optical facilities is significant as well. That isn’t to argue that fixed and wireless networks are in any way equivalent in terms of absolute bandwidth. But there is a financial question.

If the expected revenue and operating cost advantage of FiOS, compared to 4G, does not provide the optimal financial return, then a wireless solution might be the most-rational way to invest new capital.

The problem is that voice is a negligible contributor to incremental revenue on a FiOS network, while video, though an important contributor of revenue, is not such a great contributor to profits. That leaves broadband, and revenue upside is tough.

That is not to say fiber to home facilities are unimportant, merely to say that they might not be the best use of capital for a provider that also is investing heavily in mobile broadband.

In fact, there is an interesting bit of data in the latest report from Akamai on global Internet usage. The global average fixed-line connection speed was 2.6 Mbps, and the global average peak connection speed was 11.4 Mbps.

Looking at mobile broadband connections, average connection speeds on known mobile providers ranged from 5.3 Mbps down to 209 kbps, while “average” peak connection speeds ranged from 23.4 Mbps down to 1.2 Mbps.

The interesting observation is that wireless broadband has the higher peak speeds, about double that of fixed line connections, with a variable “average” speed that in some cases also is twice as high as fixed-line connections, though such sessions are highly variable. When mobile broadband is slow, it is an order of magnitude slower than fixed line connections. Global broadband speeds

“You're going to see that come in the fourth quarter with the what we now call the Cantenna, which is not a commercial name obviously, but it's the antenna that we actually trialed with DIRECTV, which was extremely successful,” said Shammo.

Some will legitimately wonder whether that approach might even wind up being used in some Verizon markets where FiOS has not already started to be deployed. LTE plus DirecTV

There are some significant Verizon markets including cities like Boston, Buffalo, N.Y, Baltimore and Alexandria, Va. where FiOS construction has not started.

The obvious new question is the rational approach Verizon should take to upgrading its fixed-line network. There isn’t much doubt about optical access media being more resistant to some weather-related impairments than copper networks, nor is there much doubt that new optical facilities cost less to maintain than older copper networks.

But the business question is how much incremental investment ought to be made in the fixed network, if video and broadband services can be provided using the wireless network. One might rationally argue that the cost of maintaining the fourth generation wireless network is lower than the cost of maintaining the FiOS network.

Obviously, if that is true then the avoided capital investment in new optical facilities is significant as well. That isn’t to argue that fixed and wireless networks are in any way equivalent in terms of absolute bandwidth. But there is a financial question.

If the expected revenue and operating cost advantage of FiOS, compared to 4G, does not provide the optimal financial return, then a wireless solution might be the most-rational way to invest new capital.

The problem is that voice is a negligible contributor to incremental revenue on a FiOS network, while video, though an important contributor of revenue, is not such a great contributor to profits. That leaves broadband, and revenue upside is tough.

That is not to say fiber to home facilities are unimportant, merely to say that they might not be the best use of capital for a provider that also is investing heavily in mobile broadband.

In fact, there is an interesting bit of data in the latest report from Akamai on global Internet usage. The global average fixed-line connection speed was 2.6 Mbps, and the global average peak connection speed was 11.4 Mbps.

Looking at mobile broadband connections, average connection speeds on known mobile providers ranged from 5.3 Mbps down to 209 kbps, while “average” peak connection speeds ranged from 23.4 Mbps down to 1.2 Mbps.

The interesting observation is that wireless broadband has the higher peak speeds, about double that of fixed line connections, with a variable “average” speed that in some cases also is twice as high as fixed-line connections, though such sessions are highly variable. When mobile broadband is slow, it is an order of magnitude slower than fixed line connections. Global broadband speeds

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, October 14, 2011

United States Leads LTE Market

|

| 4G Adoption Forecast |

But U.S. consumers have shown an ability to adopt such innovations in relatively short order once the value was perceived. Nobody argues anymore that U.S. consumers somehow lag in use of any of those services.

More recently, the U.S. market has emerged as the leader in mobile applications, smart phone development and now will take leadership in 4G networks as well.

Verizon, MetroPCS, and AT&T will account for the majority of 4G Long Term Evolution connections globally by year-end 2011. Pyramid Research expects that U.S. mobile service providers, with seven million LTE connections, will account for 47 percent of the world’s LTE subscriptions.

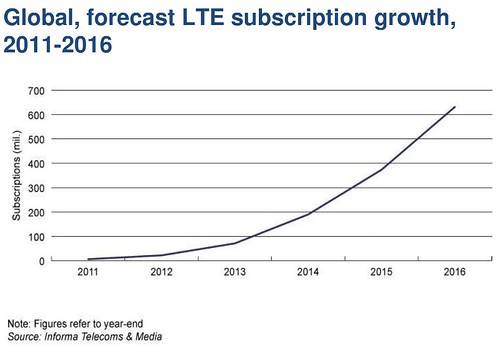

Pyramid expects 71 percent of 5.4 million global LTE handset sales will come from the United States in the near term. Separately, Informa Telecoms & Media projects something on the order of 600 million 4G subscriptions in service by about 2016.

The strong demand for mobile broadband in the U.S. market also will allow operators to quickly recoup spending on capital investments. Verizon and NTT Docomo, both the largest operators in their respective countries, each launched LTE in December 2010.

The strong demand for mobile broadband in the U.S. market also will allow operators to quickly recoup spending on capital investments. Verizon and NTT Docomo, both the largest operators in their respective countries, each launched LTE in December 2010.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, October 12, 2011

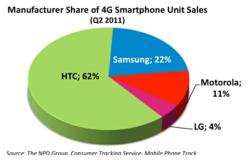

22% of U.S. Smart Phones Sold were 4G Capable

About 22 percent of smart phones purchased by U.S. consumers in the second quarter of 2011 were capable of running at 4G speeds.

About 22 percent of smart phones purchased by U.S. consumers in the second quarter of 2011 were capable of running at 4G speeds. A year ago, just three percent of U.S. smart phones sold could run on a 4G network, according to the NPD Group.

The top four smart phone 4G manufacturers, based on consumer sales in Q2 2011:

1.HTC: 62%

2.Samsung: 22%

3.Motorola: 11%

4.LG: 4%

What the study did not look at, but seems correct, is that "4G" is not yet a distinct "service." It is faster than 3G, which is good, but not yet in any way a truly different "service" than 3G. So far, 4G is a "better pipe," but just that: a better pipe, as a 10 Mbps connection is better than a 5 Mbps connection.

For 4G is anything more than "table stakes" for mobile service providers, the end use experience will have to change. So far, that hasn't happened.

1.HTC: 62%

2.Samsung: 22%

3.Motorola: 11%

4.LG: 4%

What the study did not look at, but seems correct, is that "4G" is not yet a distinct "service." It is faster than 3G, which is good, but not yet in any way a truly different "service" than 3G. So far, 4G is a "better pipe," but just that: a better pipe, as a 10 Mbps connection is better than a 5 Mbps connection.

For 4G is anything more than "table stakes" for mobile service providers, the end use experience will have to change. So far, that hasn't happened.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, September 18, 2011

New Verizon Policy on Heavy Users, Congested Towers

Verizon Wireless has instituted a new network management policy that some will call “throttling,” while others might say simply represents a more-nuanced way of managing network congestion.

The new plan affects what Verizon says is about five percent of Verizon’s user base, specifically those users of 3G services that use 2 Gbytes of more of data each month, from congested cell sites. The rules do not apply to users of the new 4G network, though. The easiest solution is simply to use 4G. It’s a better experience anyway. New Verizon usage scheme

One suspects that users are capable of making rational choices about their services, and also will rapidly adopt the “default to Wi-Fi strategy.” Most people already seem capable of quickly grasping the advantages.

Some 64 percent of smart phone consumers surveyed by Devicescape use Wi-Fi hotspots at least once a day. Most smart phone owners who use Wi-Fi also use it on the road. The study showed 90 percent of those users report accessing Wi-Fi both at home and on the road. Smart phone users use Wi-Fi often

Of those who use Wi-Fi outside their home or office, most (24 percent) connect at a cafe or coffee shop, 17.3 percent at a hotel, and 15 percent at a school campus. See Facing data caps, consumers keep turning to Wi-Fi.

Historically, mobiles haven’t been used excessively for data connections. Average mobile data consumption increased from about 90 MBytes per month during the first quarter of 2009 to 298 MBytes per month during the first quarter of 2010, according to Nielsen.

This represents a year-over-year increase of approximately 230 percent, though. While this increase is substantial, in the first quarter of 2009 more than a third of smart phone subscribers used less than 1 MByte of data per month and usage has dropped to a quarter in the first quarter of 2010.

About 20 million current smart phone users are hardly using any data.

But there is a reason frameworks for managing bandwidth use are important. As mobile data consumption continues to grow, the usage pattern is starting to resemble fixed-line patterns, and that is a problem for all mobile service providers, as there is not now, and never will be any way for mobile providers to match the bandwidth, or cost of bandwidth, that a fixed network provider can offer.

There is a telling statistic in Cisco's Visual Networking Index, namely that as mobile broadband users have rapidly grown, their usage pattern rapidly has assumed the familiar pattern seen in the fixed-line part of the business.

Consider heavy usage patterns. The top one percent of mobile data subscribers generate over 20 percent of mobile data traffic, down from 30 percent just a year ago. That 29-point swing in just 12 months suggests that as more "typical" users adopt mobile broadband, they bring behaviors much different from those of early mobile broadband adopters, namely less-intensive consumption.

Cisco also reports that mobile data traffic over the last year also now matches the 1:20 ratio that has been true of fixed networks for several years (one percent of users generate or consume 20 percent of total transferred bytes). Visual networking index

Similarly, the top 10 percent of mobile data subscribers now generate approximately 60 percent of mobile data traffic, down from 70 percent at the beginning of the year.

All of those instances of "reversion toward the mean" are driven by the broader adoption by "typical" users of smart phone service. That noted, average smart phone usage doubled in 2010. The average amount of traffic per smart phone in 2010 was 79 Mbytes per month, up from 35 Mbytes per month in 2009.

The new plan affects what Verizon says is about five percent of Verizon’s user base, specifically those users of 3G services that use 2 Gbytes of more of data each month, from congested cell sites. The rules do not apply to users of the new 4G network, though. The easiest solution is simply to use 4G. It’s a better experience anyway. New Verizon usage scheme

One suspects that users are capable of making rational choices about their services, and also will rapidly adopt the “default to Wi-Fi strategy.” Most people already seem capable of quickly grasping the advantages.

Some 64 percent of smart phone consumers surveyed by Devicescape use Wi-Fi hotspots at least once a day. Most smart phone owners who use Wi-Fi also use it on the road. The study showed 90 percent of those users report accessing Wi-Fi both at home and on the road. Smart phone users use Wi-Fi often

Of those who use Wi-Fi outside their home or office, most (24 percent) connect at a cafe or coffee shop, 17.3 percent at a hotel, and 15 percent at a school campus. See Facing data caps, consumers keep turning to Wi-Fi.

Historically, mobiles haven’t been used excessively for data connections. Average mobile data consumption increased from about 90 MBytes per month during the first quarter of 2009 to 298 MBytes per month during the first quarter of 2010, according to Nielsen.

This represents a year-over-year increase of approximately 230 percent, though. While this increase is substantial, in the first quarter of 2009 more than a third of smart phone subscribers used less than 1 MByte of data per month and usage has dropped to a quarter in the first quarter of 2010.

About 20 million current smart phone users are hardly using any data.

But there is a reason frameworks for managing bandwidth use are important. As mobile data consumption continues to grow, the usage pattern is starting to resemble fixed-line patterns, and that is a problem for all mobile service providers, as there is not now, and never will be any way for mobile providers to match the bandwidth, or cost of bandwidth, that a fixed network provider can offer.

There is a telling statistic in Cisco's Visual Networking Index, namely that as mobile broadband users have rapidly grown, their usage pattern rapidly has assumed the familiar pattern seen in the fixed-line part of the business.

Consider heavy usage patterns. The top one percent of mobile data subscribers generate over 20 percent of mobile data traffic, down from 30 percent just a year ago. That 29-point swing in just 12 months suggests that as more "typical" users adopt mobile broadband, they bring behaviors much different from those of early mobile broadband adopters, namely less-intensive consumption.

Cisco also reports that mobile data traffic over the last year also now matches the 1:20 ratio that has been true of fixed networks for several years (one percent of users generate or consume 20 percent of total transferred bytes). Visual networking index

Similarly, the top 10 percent of mobile data subscribers now generate approximately 60 percent of mobile data traffic, down from 70 percent at the beginning of the year.

All of those instances of "reversion toward the mean" are driven by the broader adoption by "typical" users of smart phone service. That noted, average smart phone usage doubled in 2010. The average amount of traffic per smart phone in 2010 was 79 Mbytes per month, up from 35 Mbytes per month in 2009.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, May 9, 2011

Better Broadband a 2-Edge Sword for Mobile Service Providers

You won't find too many people arguing that Long Term Evolution, WiMAX or 4G in general is a bad thing, long term. You can find lots of people who might say the timing of the investment is an issue, that the danger of overpaying to acquire spectrum is an issue, or that protocol decisions carry some risk.

You won't find too many people arguing that Long Term Evolution, WiMAX or 4G in general is a bad thing, long term. You can find lots of people who might say the timing of the investment is an issue, that the danger of overpaying to acquire spectrum is an issue, or that protocol decisions carry some risk.One hears less talk about the impact on voice services as lower-latency mobile broadband services are introduced. One advantage LTE offers application providers and access providers is much better latency performance, which means better real-time services performance. That means better voice and video.

But that lower latency is better for all providers of real-time services, not just the mobile broadband provider.

"Because LTE is all-IP and offers lower latency, it puts mobile calling services from OTT providers like Skype on more equal footing with existing carrier wireless voice services," says Tole Hart, Yankee Group senior analyst.

In other words, though LTE is strategic for mobile service providers, it also means a better platform for over-the-top application providers who have services requiring good latency performance.

Yankee Group forecasts smart phone penetration reaching 50 percent by the end of 2011 and 70 percent by 2013, meaning there will be more customers using their smart phones to download alternative calling apps from application providers like Skype, Vonage and Google Voice, and possibly from social communities like Facebook in the future.

The standard "advice" for mobile service providers is to enhance the value of their captive voice services. It's good advice, though strategically problematic, since the application providers will continue to enhance the value of their own services as well.

Obviously, at stake for carriers is a portion of the approximately $730.4 billion in global mobile voice service revenue. But there also will be danger from application providers who bundle text messaging with their voice services, as well.

Text messaging generates about $74.7 billion worth of revenue, and very-high profit margins.

Text messaging generates about $74.7 billion worth of revenue, and very-high profit margins.

Mobile service providers have important advantages in terms of creating bundles of services that will tend to keep customers "glued" to a basket of features including voice, text messaging and broadband access. That would be a simple adoption of the fixed-line "triple play" strategy, where the incremental cost of any one service is relatively low, in a package of three or four services.

Of course, in some markets mobile service providers might also be able to apply native quality of service mechanisms that provide meaningful experience advantages for end users, and are not available to other application providers. In other cases mobile service providers might want to sell those capabilities to third-party voice providers as a revenue-generating product.

The point is that there is no simple, fool-proof way to "firewall" a mobile voice service from more-effective application provider competition once an LTE network is in place. Bundles and quality assurance are likely to be important weapons, though.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, May 2, 2011

Is Telstra Getting Out of Fixed Line Consumer Voice?

In what might strike you as an odd statement, Telstra executives say that VoIP is not sufficiently reliable to sell to consumers.

While launching a new IP telephony services aimed at small business customers, Telstra CEO David Thodey said the company was only continuing to review consumer VoIP services.

“As we think the product is mature enough, and has enough technical backup, we’ll bring that product to market,”Thodey said. However, Thodey didn’t appear to believe a Telstra VoIP offering would appear soon, according to Australian content provider Delimiter.

“We don’t think the quality and reliability is there," Thodey said. "We could bring it to the market tomorrow, but we don’t want to."

That explanation might strike some as quite odd, given the success carriers are having with consumer VoIP.

In fact, some of us might speculate that something else is afoot, namely an unwillingness to invest in consumer VoIP because Telstra might not want to sell consumer VoIP when it starts to buy wholesale access services from the National Broadband Network.

When that happens, Telstra, like other retail service providers, will have a choice of customers to serve. Given Telstra's belief in 4G Long Term Evolution, Telstra might be planning to rely on wireless for consumer voice, staying out of the consumer fixed-line voice service.

That might strike you as odd, but keep in mind that Telstra also operates separate cable TV facilities, running on separate networks. While you might think Telstra is giving up a "triple play" opportunity, it isn't. Telstra can deliver broadband access using the NBN, video entertainment on its existing cable TV networks and voice and mobile broadband on its planned 4G network.

In principle, Telstar could deliver voice using its cable networks as well, but Telstra might simply have concluded that mobile is the best way to sell voice to consumers.

http://links.eqentia.com/520b2ad1536d771f/?dst=http://delimiter.com.au/2011/05/02/consumer-voip-not-reliable-says-telstra/&utm_campaign=visibli&utm_source=cisco&utm_medium=twitter

While launching a new IP telephony services aimed at small business customers, Telstra CEO David Thodey said the company was only continuing to review consumer VoIP services.

“As we think the product is mature enough, and has enough technical backup, we’ll bring that product to market,”Thodey said. However, Thodey didn’t appear to believe a Telstra VoIP offering would appear soon, according to Australian content provider Delimiter.

“We don’t think the quality and reliability is there," Thodey said. "We could bring it to the market tomorrow, but we don’t want to."

That explanation might strike some as quite odd, given the success carriers are having with consumer VoIP.

In fact, some of us might speculate that something else is afoot, namely an unwillingness to invest in consumer VoIP because Telstra might not want to sell consumer VoIP when it starts to buy wholesale access services from the National Broadband Network.

When that happens, Telstra, like other retail service providers, will have a choice of customers to serve. Given Telstra's belief in 4G Long Term Evolution, Telstra might be planning to rely on wireless for consumer voice, staying out of the consumer fixed-line voice service.

That might strike you as odd, but keep in mind that Telstra also operates separate cable TV facilities, running on separate networks. While you might think Telstra is giving up a "triple play" opportunity, it isn't. Telstra can deliver broadband access using the NBN, video entertainment on its existing cable TV networks and voice and mobile broadband on its planned 4G network.

In principle, Telstar could deliver voice using its cable networks as well, but Telstra might simply have concluded that mobile is the best way to sell voice to consumers.

http://links.eqentia.com/520b2ad1536d771f/?dst=http://delimiter.com.au/2011/05/02/consumer-voip-not-reliable-says-telstra/&utm_campaign=visibli&utm_source=cisco&utm_medium=twitter

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, April 25, 2011

Businesses Up Tablet, Notebook, E-Reader Spending 30%

Business spending on 3G and 4G devices such as tablets, notebooks, and e-readers was up nearly 30 percent in 2010, compared to 2009.

“A key take away from the research is that the non-handset spending increase trend seems to be universal across all sizes of business,” says Greg Potter, research analyst. “There are some slight variations in some of the vertical segments but, they too, share a robust 2010 and have a very healthy five-year forecast.”

Enterprise spending makes up over 62 percent of business spending on non-handset data services, spending over $1.9 billion in 2010.

Enterprise (1,000 to 4,999 employees) will increase spending in 2011 by 19.5 percent in the professional services vertical. Small office and home office spending will surpass $275 billion by 2014, In-Stat projects.

The healthcare and social services vertical represents the largest share of spending, over $400 million in 2010.

“A key take away from the research is that the non-handset spending increase trend seems to be universal across all sizes of business,” says Greg Potter, research analyst. “There are some slight variations in some of the vertical segments but, they too, share a robust 2010 and have a very healthy five-year forecast.”

Enterprise spending makes up over 62 percent of business spending on non-handset data services, spending over $1.9 billion in 2010.

Enterprise (1,000 to 4,999 employees) will increase spending in 2011 by 19.5 percent in the professional services vertical. Small office and home office spending will surpass $275 billion by 2014, In-Stat projects.

The healthcare and social services vertical represents the largest share of spending, over $400 million in 2010.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, April 15, 2011

T-Mobile Adds 10 New 4G Markets

Ten more markets have T-Mobile's 4G (HSPA+)network, bringing the 4G network up to 167 markets and more than 200 million people in the United States.

The new 4G markets include:

Ames, Iowa

Anderson, Indiana

Battle Creek, Michigan

Benton Harbor, Michigan

Jackson, Michigan

Fort Collins-Loveland, Colorado

Lawrence, Kansas

Manhattan, Kansas

Springfield, Illinois

Wichita Falls, Texas.

T-Mobile is also working to double the speeds of its 4G service to 42 Mbps in 25 of its 4G markets, covering more than 140 million people, this year.

New York City, Las Vegas and Orlando are already online with 42 Mbps service. Chicago, Long Island and parts of New Jersey are slated to follow soon.

The new 4G markets include:

Ames, Iowa

Anderson, Indiana

Battle Creek, Michigan

Benton Harbor, Michigan

Jackson, Michigan

Fort Collins-Loveland, Colorado

Lawrence, Kansas

Manhattan, Kansas

Springfield, Illinois

Wichita Falls, Texas.

T-Mobile is also working to double the speeds of its 4G service to 42 Mbps in 25 of its 4G markets, covering more than 140 million people, this year.

New York City, Las Vegas and Orlando are already online with 42 Mbps service. Chicago, Long Island and parts of New Jersey are slated to follow soon.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, January 22, 2011

4G for Business: What's the Value Driver?

(click on image for a larger view)

"Unlike 3G, 4G networks are end-to-end IP, designed from the start to support converged application traffic and provide improved latency," Yankee Group researchers note. Examples of new applications sometimes center on collaboration apps, especially forms of telepresence and videoconferencing.

Others suggest 4G can be used as a better replacement for existing 3G applications and use cases, as a backup or replacement for fixed-line broadband, backhaul or redundant capacity service for times of peak load.

Call me a skeptic at this point, but similar claims about "enabling new applications" were touted when 3G networks were deployed as well, and it took quite some time for important new apps to develop.

New 4G networks are a vast improvement over 3G in many ways, but the mere existence of the network probably will not lead to dramatically-new apps, right away. If that does happen, some have suggested, it will be "personal Wi-Fi hotspot" or video apps that likely will drive the lead apps.

Initially, though, 4G is likely to be viewed as "better wireless broadband," to support existing apps. I'd prefer to be proven wrong, and soon. But history suggests it will take some time for really new apps to develop, in the business or consumer spaces.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, January 7, 2011

Sprint as Wal-Mart?

“Sprint is at a crossroads,” said Craig Moffett, a New York-based analyst at Sanford C. Bernstein. “Their time-to- market advantage is now largely gone for 4G.”

That's true enough. What isn't so clear is how Sprint's positioning will evolve, now that the 4G platform does not offer such uniqueness.

Some might argue that Sprint will have emphasize its lower cost plans for unlimited wireless data use. "Unlimited," assuming the other carriers do not offer it, will offer some uniqueness.

Some might argue that Sprint will have emphasize its lower cost plans for unlimited wireless data use. "Unlimited," assuming the other carriers do not offer it, will offer some uniqueness.

I suspect Sprint will do more than that. Whether Sprint would agree with the Wal-Mart analogy is not clear. That Sprint would base its strategy on that seems unlikely. We'll see.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, January 6, 2011

Verizon CEO Touts 4G

It's fast. It might be pricey, not in terms of formal price ($50a month for PC dongle service, with a 5 Gbyte cap, $80 for a 10-Gbyte cap), but if it encourages people to watch lots of video on their PCs, using the air cards, that they might not have in the past, it could get expensive.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, December 20, 2010

AT&T Acquires 700-MHz spectrum from Qualcomm

AT&T is buying spectrum licenses in the 700 MHz frequency band from Qualcomm for $1.925 billion. The spectrum will be used as part of AT&T's Long Term Evolution 4G mobile broadband network.

Qualcomm had been using the spectrum to support its FLO TV business, but Qualcomm is shutting the service in March 2011.

The spectrum covers more than 300 million people total nationwide and includes 12 MHz of 700 MHz D and E block spectrum covers more than 70 million people in five of the top 15 U.S. metropolitan areas, including New York, Boston, Philadelphia, Los Angeles and San Francisco.

The network also includes 6 MHz of 700 MHz "D block" spectrum covers more than 230 million people across the rest of the United States.

Frequencies in the 700 MHz and 800 MHz bands are highly favored for mobile services because the signals feature both more range and greater ability to penetrate buildings. As indoor coverage is a continual issue for mobile services, the new frequencies will help AT&T deal with indoor coverage for its LTE network.

read more here

Qualcomm had been using the spectrum to support its FLO TV business, but Qualcomm is shutting the service in March 2011.

The spectrum covers more than 300 million people total nationwide and includes 12 MHz of 700 MHz D and E block spectrum covers more than 70 million people in five of the top 15 U.S. metropolitan areas, including New York, Boston, Philadelphia, Los Angeles and San Francisco.

The network also includes 6 MHz of 700 MHz "D block" spectrum covers more than 230 million people across the rest of the United States.

Frequencies in the 700 MHz and 800 MHz bands are highly favored for mobile services because the signals feature both more range and greater ability to penetrate buildings. As indoor coverage is a continual issue for mobile services, the new frequencies will help AT&T deal with indoor coverage for its LTE network.

read more here

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, December 19, 2010

ITU Says Some 3G Networks are 4G, Pre-4G is 4G, and 4G is 4G

The International Telecommunications Union recently defined “LTE-Advanced” and “WirelessMAN-Advanced” as the only "official definitiions of "fourth generation" networks, automatically making networks operated by Sprint, Clearwire, Verizon, MetroPCS and all other operators of WiMAX and Long Term Evolution networks something other than standards-based "4G" networks.

Now the ITU has muddied the waters even more, saying that some "3G" networks are "4G," while the formal "pre-4G" networks in existence, or about to be built, also are "4G."

"As the most advanced technologies currently defined for global wireless mobile broadband communications, IMT-Advanced is considered as “4G”, although it is recognized that this term, while undefined, may also be applied to the forerunners of these technologies, LTE and WiMax, and to other evolved 3G technologies providing a substantial level of improvement in performance and capabilities with respect to the initial third generation systems now deployed," the ITU says in a new statement.

Huh? Some of us have had no issue with T-Mobile USA saying its new HSPA+ network offers "speeds equivalent to 4G," because the WiMAX and HSPA+ networks do offer comparable access speeds. But it does create a definitional muddle. It's one thing for marketplace contestants to position their networks in one way or another.

It might be quite another for a "standards" body to argue that 3G is 4G, existing 4G is 4G, and other possible networks might also be 4G.

What's the point of a standard when it isn't a standard any longer? In this case, it might mean that the "non-standard" standards will grow organically to the point that the newly-minted "4G" standard simply ceases to be relevant, much as adherence to the supposedly-"legacy" TCP/IP completely killed the shift to new protocols for layers one through four of the data communications protocols.

One might say the ITU flip flop is merely embarassing, and yet another example of standards bodies attempting to define "next generation" networks. It might result in something far more substantial than that. One might suggest that the whole effort now is questionable, in terms of helping shape the development of 4G.

Once critical mass developments around the real-world 4G and advanced 3G networks, services, revenue elements and devices, evolution will happen based on those factors. That doesn't mean operators will abandon the effort to keep developing more-capable networks. But as we have seen with TCP/IP and other data "standards," the market often decides what a standard is.

So far, the markets, and end users, have decided the path for next-generation networks, in large part. That could well happen here as well. No matter what the ITU thinks, if voluntary groups such as the GSM decide to evolve LTE in some other direction, the existence of a formal standard will not deter them.

That is not to fault the well-intentioned hard work of the technologists working on the standard. The point is simply that the global telecommunications industry has yet to prove it can devise a "next-generation" network standard that real-world operators actually embrace obviously, and with great commercial success. Instead, the pattern so far has been that network operators and end users sort of grope towards better solutions as best they can.

But it is equally true that, up to this point, real-world commercial success has not been driven so much by the standards as by solutions that users believe are workable and useful.

For a discussion f the ITU standards, read this: http://www.itu.int/itunews/manager/display.asp?lang=en&year=2008&issue=10&ipage=39&ext=html and this http://www.networkworld.com/news/2010/121710-itu-softens-on-the-definition.html.

For a discussion of the change, arguing that the ITU now has erred twice on the same subject, see http://www.abiresearch.com/research_blog/1520.

Now the ITU has muddied the waters even more, saying that some "3G" networks are "4G," while the formal "pre-4G" networks in existence, or about to be built, also are "4G."

"As the most advanced technologies currently defined for global wireless mobile broadband communications, IMT-Advanced is considered as “4G”, although it is recognized that this term, while undefined, may also be applied to the forerunners of these technologies, LTE and WiMax, and to other evolved 3G technologies providing a substantial level of improvement in performance and capabilities with respect to the initial third generation systems now deployed," the ITU says in a new statement.

Huh? Some of us have had no issue with T-Mobile USA saying its new HSPA+ network offers "speeds equivalent to 4G," because the WiMAX and HSPA+ networks do offer comparable access speeds. But it does create a definitional muddle. It's one thing for marketplace contestants to position their networks in one way or another.

It might be quite another for a "standards" body to argue that 3G is 4G, existing 4G is 4G, and other possible networks might also be 4G.

What's the point of a standard when it isn't a standard any longer? In this case, it might mean that the "non-standard" standards will grow organically to the point that the newly-minted "4G" standard simply ceases to be relevant, much as adherence to the supposedly-"legacy" TCP/IP completely killed the shift to new protocols for layers one through four of the data communications protocols.

One might say the ITU flip flop is merely embarassing, and yet another example of standards bodies attempting to define "next generation" networks. It might result in something far more substantial than that. One might suggest that the whole effort now is questionable, in terms of helping shape the development of 4G.

Once critical mass developments around the real-world 4G and advanced 3G networks, services, revenue elements and devices, evolution will happen based on those factors. That doesn't mean operators will abandon the effort to keep developing more-capable networks. But as we have seen with TCP/IP and other data "standards," the market often decides what a standard is.

So far, the markets, and end users, have decided the path for next-generation networks, in large part. That could well happen here as well. No matter what the ITU thinks, if voluntary groups such as the GSM decide to evolve LTE in some other direction, the existence of a formal standard will not deter them.

That is not to fault the well-intentioned hard work of the technologists working on the standard. The point is simply that the global telecommunications industry has yet to prove it can devise a "next-generation" network standard that real-world operators actually embrace obviously, and with great commercial success. Instead, the pattern so far has been that network operators and end users sort of grope towards better solutions as best they can.

But it is equally true that, up to this point, real-world commercial success has not been driven so much by the standards as by solutions that users believe are workable and useful.

For a discussion f the ITU standards, read this: http://www.itu.int/itunews/manager/display.asp?lang=en&year=2008&issue=10&ipage=39&ext=html and this http://www.networkworld.com/news/2010/121710-itu-softens-on-the-definition.html.

For a discussion of the change, arguing that the ITU now has erred twice on the same subject, see http://www.abiresearch.com/research_blog/1520.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

It's a Good Thing App Developers Aren't at the Mercy of the ITU

If you want an excellent example of why it is a very good thing that software development now is viewed as occurring in "layers," where underlying communications protocols are abstracted, consider the situation facing mobile software developers.

Devices, tools, vendors, network contracts, business requirements, customer attitudes and competitors will change rapidly, probably invalidating some aspect of a strategy every couple of months.

For that reason, it is a very good thing that among the complications an application developer does not have to worry about is uncertainty about communications protocols in layers one through four of the "stack."

If there were tight linkage between layer-seven apps and layers one to four, developers would be in a pickle, now that the International Telecommunications Union has first created WiMAX and Long Term Evolution standards no real-world network uses, and further has complicated matters by saying that existing advanced 3G and pre-standard 4G networks are, in fact, 4G networks.

It's one thing to create standards that allow global networks to communicate. It's a good thing to have an evolution plan for networks that support greater functionality. It isn't so clear how useful it is to create a well-intentioned standard that first defines all existing networks of that type out of existence, before backtracking and declaring all of them to be "standards-compliant," and then to stretch the definition to include some advanced 3G networks as well.

App developers would face much greater uncertainty were they forced to create tools and products that had to track those sorts of changes.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, December 13, 2010

4G Has Been a Technical Issue; Now it Becomes a Business Issue

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...