“Customer journey disruptions brought about by the pandemic have prompted CMOs across industries to question long-held beliefs on the relative value of their channel investments,” say Gartner analysts. The biggest trend has been that--unable to rely on in-person channels--spending shifted to digital channels.

Some 72 percent of the marketing budget of surveyed enterprises is “pure digital,” says Gartner.

What remains unclear is whether marketing tactics and practices will remain permanently shifted in that way.

Some may well conclude that their sales results have not suffered. Simply put, most enterprises have somehow managed to keep sales and marketing going, if in different ways, and some have even reported revenue gains, even when unable to visit customers directly, or have customers visit them.

So the big question is whether there have been changes in belief and practices that are permanent, and not simply transitory.

At a high level, the issue can be neatly summarized: enterprises have had to find some way to keep revenues flowing despite the substantial inability to have in-person contact with business partners or customers.

The longer term issue is whether executives will conclude they do not need to spend money, time and effort in the old ways, at the same levels. That, in turn, will have repercussions for many in marketing and sales ecosystems.

“CFOs have become comfortable with the lower cost base that spending cuts in marketing, alongside savings on real estate and travel costs, have yielded,” Gartner says in a new report. “CMOs proved that they could do more with less, curbing spending on events, agencies and ad budgets in the face of a crisis.”

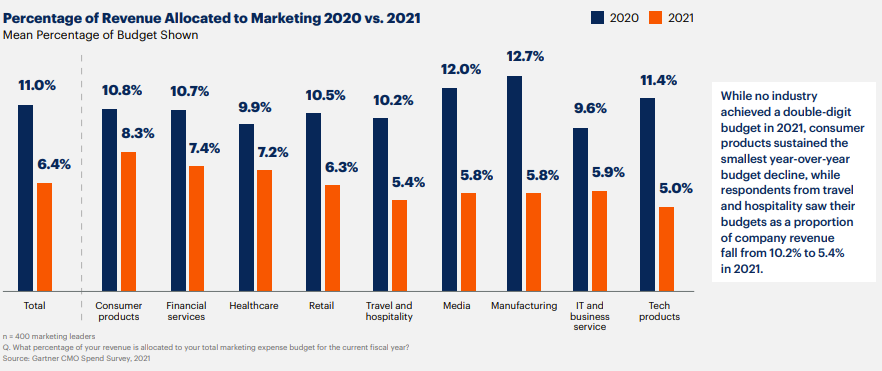

Among the areas most affected are items such as business “travel and hospitality,” which fell nearly 50 percent from 2020 to 2021. Investments in digital processes to support business operations are taking priority over marketing, Gartner says.

“CEOs state the top focus points for their Chief Digital Officers (CDOs) in 2021 include customer experience and e-commerce.” Marketing execs have reprioritized the spending commitments across their channels and programs to favor pure-play digital channels, accounting for 72.2 percent of the total marketing budget.

Typically, budget priorities reflect business priorities. So less spending is typically interpreted as “lower value” or priority. That might not necessarily be true for marketing budgets.

Marketing budgets have always been the first of the enterprise budgets to be cut in any recession and the last to be restored once growth returns, Gartner notes, and rightly so.

And marketing budgets are falling to their lowest levels in recent history, say analysts at Gartner.

So one might conclude that marketing--perhaps always to some extent a “more is better” category--is less important at the moment. That is almost certainly untrue. Unable to conduct face-to-face operations, marketing arguably has been more important.

But perhaps higher value is perceived even when spending levels are lower. In other words, the ability to “do more with less” might be the conclusion many have reached after their experience with virtual sales and marketing imposed on them.

“Social distancing rules transformed buying journeys for B2B and B2C customers alike throughout 2020,” Gartner notes. Also, “the majority of customers who used a digital channel for the first time in the first wave of the COVID-19 crisis state that they will continue to use them when the crisis passes.”

That suggests an “inevitable shift to online channels.”

The still-unknown issue is how much permanent change could occur in enterprise marketing practices. As always, there will be repercussions in the rest of the business ecosystem.